What are the differences between Mortgage Reducing Term Assurance (MRTA), Overdraft Term Level Assurance (ODLTA) and Mortgage Level Term Assurance (MLTA) insurance? Which is better for my needs? Does it make a difference if the property is for my own stay or for investment purposes?

Updated: Oct 21, 2018

As part of property ownership, you need to consider asset risks planning if you buy your property with financing should anything unfortunate happen.

We discuss a few options for protecting your property assets, and provide guidelines on pros, cons, tips, costs, and how much coverage is needed.

Why the need for property asset risk planning?

Being a wise property owner, you will want to manage asset risk planning to make sure unfortunate events i.e. becomes incapacitated or passing away have minimal impact on you and your loved ones.

Property Asset Risks

- Losing the home you and your family live in.

- Losing your property to the bank or forced to auction off your property.

- Forced to sell your property at a loss.

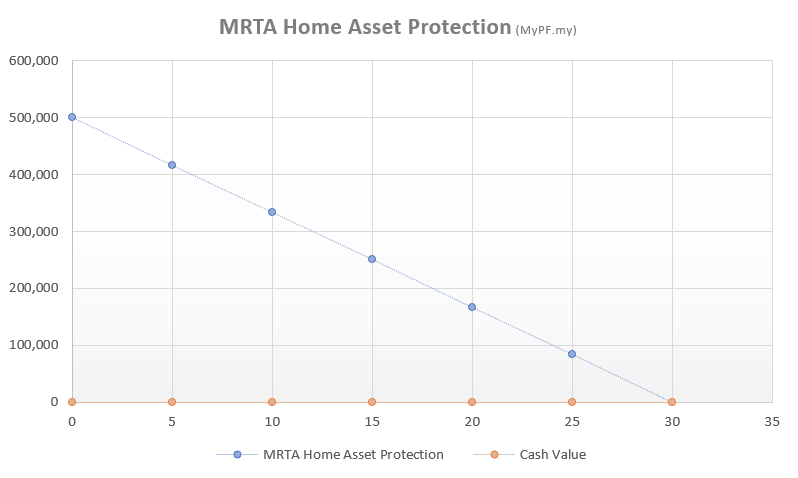

MRTA: Mortgage Reducing Term Assurance

Protection: MRTA gives you protection which reduces over time until it reaches zero. In the past MRTA was often compulsory. Today, you have more flexibility (although some banks are resorting to offer better rates if you take a MRTA and loan with the bank).

Duration: 5 years – 35 years (up to maximum home loan duration)

Cash Value: No (If you make an upfront lump sum payment, you made get back a refund for future premiums if you cancel your MRTA early)

Costs: Approximately RM3,500 for every RM100,000 of protection required (one time)

- E.g. RM500,000 protection: 17,500 (lump sum)

Pros

- MRTA is lower cost in terms of total premium, especially if you short cover instead of your full duration of your home loan.

- MRTA can be bundled together with your home loan reducing cash outlay.

Cons

- MRTA in Malaysia does not have critical illnesses coverage (only death and Total Permanent Disability).

- Protection coverage may be insufficient as your protection either ends earlier OR your owing amount is higher than the protection you have, especially loan rates increases.

- No cash value. Even if you cancel the MRTA policy early, you may get back only a certain % of the premium paid (or zero when nearing the last years of the MRTA policy).

- May be an expensive cost for the MRTA if factored into your home loan would approximately double.

- E.g. RM500,000 protection: 35,000 (factored into home loan) / Additional RM175 per month for home loan payments.

- MRTA can be moved to another property when you sell and buy a new property, with some difficulty and paper-work and only for conventional non-Takaful MRTA policies.

- Insurability is not guaranteed. You need to prove you are healthy every time you want to purchase a new MRTA.

Tips

- Consider other options besides MRTA, focusing on value and not just the total premium costs. Other options such as a MLTA often prove to be better alternative.

- If possible, pay off the MRTA separately (not bundled into home laon) as otherwise you will be charged a high amount of interest.

- If you are “forced” to take a MRTA by the bank, take the minimal coverage for the minimum period of years (typically 5 years). Then follow up with your own property asset risk planning.

MLTA: Mortgage Level Term Assurance

Protection: MLTA offers level (or slightly increasing) protection.

Duration: As long as you need the coverage. (At the minimum, coverage for 30 years available).

Cash Value: Yes (increasing over time but may dip in old age as protection costs increase).

Costs: Approximately RM400 for every RM100,000 of protection required (per year). Min RM1,200 per year.

- E.g. RM500,000 protection: 2,000 per year (166 per month)

Pros

- MLTA gives you the same or increasing protection over time.

- Upon claim, payout goes to you/nominee(s) which you can use at your own choosing including paying part/all of your home loan.

- Cash value accumulation which you can withdraw at any time (or upon ending your MLTA).

- MLTA is on your life and not tied to a particular property. If you decide to sell your property and purchase a new property you can use your same existing MLTA as risk protection for your new property.

- Flexibility with protection value which can be adjusted up or down at any time you desire.

- Option to add on a premium waiver whereby if Total Permanent Disability (TPD) or Critical Illness (CI) occurs, all future premiums are waived.

Cons

- MLTA is more expensive than MRTA in terms of total premium costs.

Tips

- Work with a good advisor familiar with MLTA products to structure your asset protection to give you the best combination of value, protection, and cash value.

- Inform your nominees (or trustee) on the insurance and instructions on dealing with the property and funds in case of passing/TPD.

ODLTA (aka ODLA): Overdraft Level Term Assurance

Protection: ODLTA provides level protection which remains the same throughout. It is more often used among short term investors to cover a short period (e.g. 5 – 10 years)

Duration: 5 years – 35 years (up to maximum home loan duration)

Cash Value: No (If you make an upfront lump sum payment, you made get back a refund for future premiums if you cancel your ODLTA early)

Costs: Approximately RM6,500 for every RM100,000 of protection required

- E.g. RM500,000 protection: 32,500 (lump sum)

Pros

- Coverage remains constant throughout the period.

- Any additional coverage after paying off for the property would go to your next of kin.

- Can be financed into your home loan.

Cons

- More expensive than MRTA by 20-30%.

- Other cons similar to above MRTA.

MRTA or MLTA?

A MLTA is a better option in terms of value and flexibility. However, your cashflow needs to be sufficient to handle the higher ongoing premiums.

A MRTA is a lower cost option, and you can bundle it with your home loan if necessary. You may also need to take up a MRTA in order to enjoy better home loan rates from your bank/financial institution.

Share and discuss on MRTA and MLTA

FAQ

- Q: How much protection do I need… ?

How much home risk protection you require would depend on each individual’s needs and personal finances circumstances. However, the following guidelines may help you in your decision making process with the following questions. - Q: … for own stay (primary residence) for medium-long term?

For your primary residence, you will want to cover close to 100% of your entire home loan amount. This will ensure that if anything untoward happens to you, that the entire home loan will be paid off and your family has a place to stay in (with extra if it’s a MLTA).

E.g. Property purchase price RM500k with 90% financing. Home loan at RM450k.

Cover sum assured RM400k – 450k. - Q: … for rental/investment purposes?

For investment properties, you would need a lesser amount of coverage. The coverage is important to ensure that if anything unexpected happens, you (or your family/investment partners) have enough time to handle necessary arrangements without having to worry about monthly loan repayments, inability to find tenants, or negative yield. For example, your family/partners may need to sell the property but need to await for the property market to recover.- Reselling (flip): suggest to cover 3 to 5 years equivalent home loan repayments.

- Rental: suggest to cover minimum 1 year equivalent home loan repayments, even if you are confident of good occupancy.

- Q: I have cash savings/investments and life insurance. Do I still need MRTA/MLTA?

No, if you are ok with using the cash savings/selling investments to cover your outstanding loan if anything untoward happens. Most of us do take loans when buying properties as it is an appreciating asset. Leverage allows you to improve your property investment returns and provides better cash flow. It is a relatively small expense for protecting your property assets adequately.

For life insurance, you will want to ensure that you are adequately protected. You should not have too much life insurance coverage unless you were overprotected and buying too much insurance previously before you purchased a property. Talk to an advisor to review and improve your risk management (and likely save money). - Q: Should I take a premium waiver rider?

It is optional. You can compare the cost difference with/without a waiver upon occurrence of disability and/or critical illness and decide.

How to calculate MRTA and MLTA premium?

Hi there ….

I bought a house and I m preparing to take MRTA as the loan I got is RM 530K with 2 names and the mortgage consultant have suggested MLTA but i’am not interested on it as I can afford monthly commitments.

1.Q:May I know how much the sum should I cover

2.Q:Is there any alternative way for the MRTA payment mode rather then lump sum Ex:Monthly,quarterly

Hope to hear ur feedback

Thank You

Contact us to get comparative quotes.

Hi , My housing loan is approx. RM160000. We bought the bouse 18 years ago. Its joint account with my husband and me. How much MLTA we should take.

hi can we pay MRTA annually? or only lumpsum and bundle with loan is allowed?

Hi,, I’m currently applying for home refinancing,, loan amount is RM510k for 33 years,, the bank I’m applying with requires me to purchase their mrta to get cheaper rates,, I just want to cross-check,, the premium quoted for RM510k coverage for 33 years is RM49,075 one-time payment,, is this premium reasonable or expensive?,, any advise is greatly appreciated,, tq

Hi, i bought an auction property last year, and commited to mortgage loan of RM500k. I was misled by my insurance agents who insisted me to take up MLTA, with premium coverage of RM750k, more than what i loaned for. The agent’s argument is that I should put in more as Im still young, as i have no relevant experience and due to time constraints of applying loans i trusted the agent. However, after some researching i regreted the decision. Is it possible to reduce the amount cover now say rm500k after signing off the initial premium? Thank you.

I bought similar plan as well for future use as MLTA, I was quoted by my agent for higher coverage because Im not sure about the price of the house I’ll be getting. But I remember usually for such plan even if we didn’t use it for the exact amount of coverage for the house , the money put in can be used for investment and it has cash value in a long run, cause I just have to commit for 5 years, not sure about yours

Hello, We have an outstanding loan amount of RM70000,

I am 62 years old and my wife is 58,My wife’s name is on loan repayment, Should we take MRTA,

What advice can you give us

https://mypf.my/contact

Hi, is mrta amount also depends on the age of loan applicant?

Hi, what would you recommend in long run if buying the house for own stay and long run benefit. Which insurance plan should go for? MRTA or MLTA? My bank quote me with lower rate if I bundle it with MRTA. And the housing loan department from the bank do not sell MLTA. MLTA is from another department from within the bank.

https://mypf.my/contact

Hi, I got a loan offer from bank approved which is 980k (90%). The offer includes MRTA payment 9k+ which is sum insured for 200k for 35 years. I feel this sum insured value is too low as it only covers about 20%. I’m still waiting to get my official offer letter. Can we actually request for more higher MRTA insured value from bank?

Also CI payment about 1700+ for sum insured value 50k for 15 years. Felt not relevant with the principle loan amount!! As the insured value is too low.

hi

i’m an ‘OKU’ physically disabled person. i’m in search a hse Nearby lrt/mrt this due -i cant drive. i’m using my staff entitlement loan but my only worries on morgage insurance MRTA… as i experienced on several insurance company who reject my medical card application but in 2010 one of the rejected company who alt offered “life insurance” with sum insured< 60k only, whn think of my parents so i just except it without med.card.

1) is there any mrta provider who easy can consider my application – people who born like me? although with loading but with affordable amount????

2) i have argued wt my approved hse loan bank who forced me to took bank appointed insurance, recently as i informed, insurance can consider but there will be loading up to min 40k++ & i have appeald but the insurance company disagreed. bnk had adviced me to dump into loan & this will increased my monthly payment- bnk just ignored my voice up on my other commitment issue's (mau ambil- tak mau cari lain bnk). whn i proposed to apply wt other insurance company and bnk sd better accept it bcoz if i tried to approach oth insurance there no promises will accept me.

pls i need solution on this matter in urgent or should i complaint wt BNM????

hi,

i got interest-free staff loan from the company, to acquire a house which is constructed by the company (i work in a developer company)

What type of insurance should I choose in order to protect the benefit of my dependents in case any untoward event on me, so that by that time, they can have the insurance compensation to payoff the staff loan to my company? MLTA or term life insurance? Which of these impose higher premium? Thank you

https://mypf.my/contact

Hi, want to ask, why bank offer me MRTA for 15 years, 20 years, 35 years, but for my boyfriend another bank offer him MRTA for 15 years, 25 years and 35 years?

The years of entitlement is not fixed? or its based on ages?

Hi , If settle the home loan payment within 5 years instead of original 20 yrs . How much fund i can get back from MRRT coverage ?

Example my loan amount is 300K

Is it mandatory to purchase mortgage insurance when buying a property?

hi, i just get my loan approval from bank 500k and bank suggest us to take MRTA 10y for the lower interest rate. but the mortgage consultant ask us to buy MLTA.

1. can we purchase MLTA lower then loan amount? bcos MRTA is join name .

Ia thr any options for example my house loan is for 30 years and i took mrtt for 20 years. Can i take another insurance after 20 years of mrtt. If can what type of insurance i can choose. Pls advise

hai for mlta premium every month want to pay or lum sum want to pay

me n my husband both at 35 – able to secure 200k house loan – small investment – we are planning to go for mrta.. how much should it cost us as bank r giving us both total upto 28K – but wat i read online is different – its way too expensive. what should we do?