Received your bonus or commission but wondering about the large deductions that are incurred? Find out how to calculate your Malaysian Bonus & Tax calculations.

Updated: Jul 26, 2018

History & Introduction

In 2009, Malaysia’s income tax moved to a Monthly Tax Deduction (MTD) or Potongan Jadual Bercukai (PCB). If you are earning on average less then 2,500 a month, you will not need to file taxes. Also as per announced in Budget 2014, you can opt not to file taxes if you are already paying MTD/PCB. However, you most likely would want to claim as there are deductions & you can get tax cash refunds.

How PCB works is that your estimated monthly tax payable amount is deducted from your salary. Your employer would pay this amount to Lembaga Hasil Dalam Negeri (LHDN) by the 10th of the month. When you file your taxes annually, you would fill up tax-related info including your accumulated PCB for the year. If you have paid more then required, you get a refund. If you have paid less, you will need to pay the difference.

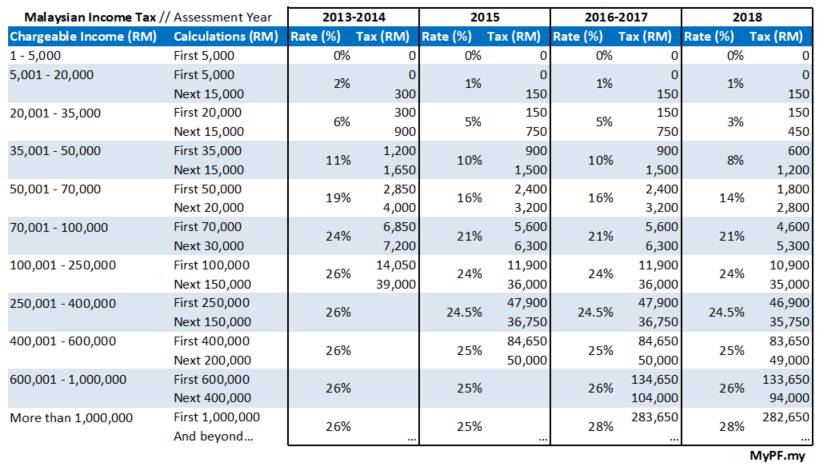

Taxes in Malaysia are progressive. A progressive tax is a tax where the tax rate increases as the taxable base amount increases. The term “progressive” refers to the way the tax rate progresses from low to high, with the result that the average tax rate is less than the highest marginal tax rate.

The taxable base amount is based on chargeable income. Salary & other remuneration less tax exemptions & tax relief.

Remuneration subject to PCB:

- Salary/Wages

- Overtime Pay

- Commission

- Tips

- Allowance

- Bonus/Incentive

- Director fees

- Perquisite (perks)

- Employee’s Share Option Scheme (ESOS)

- Tax borne by the Employer

- Gratuity

- Compensation for loss of employment

- Other remuneration related to employment

PCB allowable deductions:

- Deduction for individual – 9,000

- Deduction for husband or wife –

3,000 in Y20144,000 (if spouse not working) - Deduction for child –

1,0002,000 per child (claimable only once per child if both parents working)in Y2014

E.g. Both husband & wife working with 3 children. Husband 2 children deduction & wife 1 children deduction. - Contribution to EPF or other approved scheme – 6,000

- Deduction for zakat (Muslims only)

Bonus – Estimate after Taxes

Moving on, how does the calculation for bonuses work?

A rough estimate is that about 16% of your bonus would go into paying for taxes & 11% for EPF deductions.

Thus you would only take home about 73% of your bonus.

E.g. Bonus 10,000. Actual take home: 7,300

Bonus – Calculation after Taxes

For a more accurate calculation, there are 2 ways that PCB is calculated. Companies may use either method. And you can calculate it yourself as well to check that it tallies.

Method

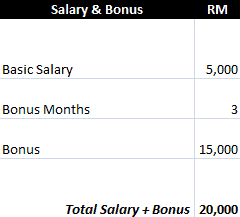

1. List down your salary & bonus/other remuneration

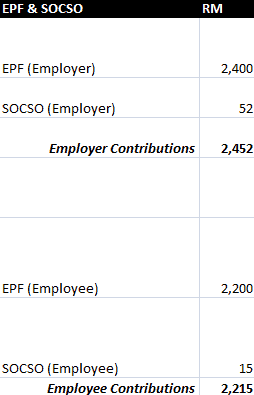

2. Calculate your EPF, SOCSO & EIS deductions

Note: for EPF include salary + bonus, SOCSO is a fixed monthly amount

EPF (default) Employer: 12% | Employee: 11%

SOCSO (max at above RM3900 monthly) Employer: 69.05 | Employee: 19.75

Employment Insurance Scheme (EIS): Employer: 0.2% | Employee: 0.2% (max RM20 or RM4,000 salary per month)

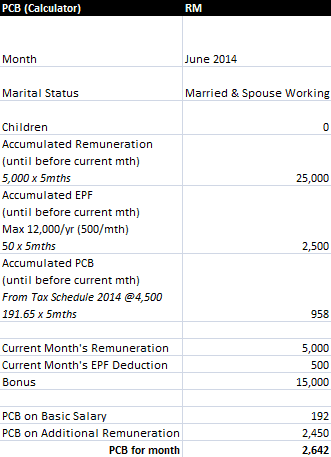

3A. Calculate using PCB Calculator

- Month: Current month | Marriage Status: Single / Married (spouse working / not working) | No of Children

- Accumulated Remuneration (until before current month): Monthly salary * Total months from Jan until last month

- Accumulated EPF (until before current month): Monthly EPF (Employee) deduction * Total months from Jan until last month

Note: If monthly EPF (employee) deduction is above 500, use 500 - Accumulated PCB (until before current month): Monthly PCB deduction * Total months from Jan until last month

Note: You can see your monthly PCB deduction in your payslip - Fill in your Current Month’s Remuneration | Current Month’s EPF Deduction | Bonus Amount

- Click Calculate & you will get your PCB on Basic Salary & PCB on Additional Remuneration

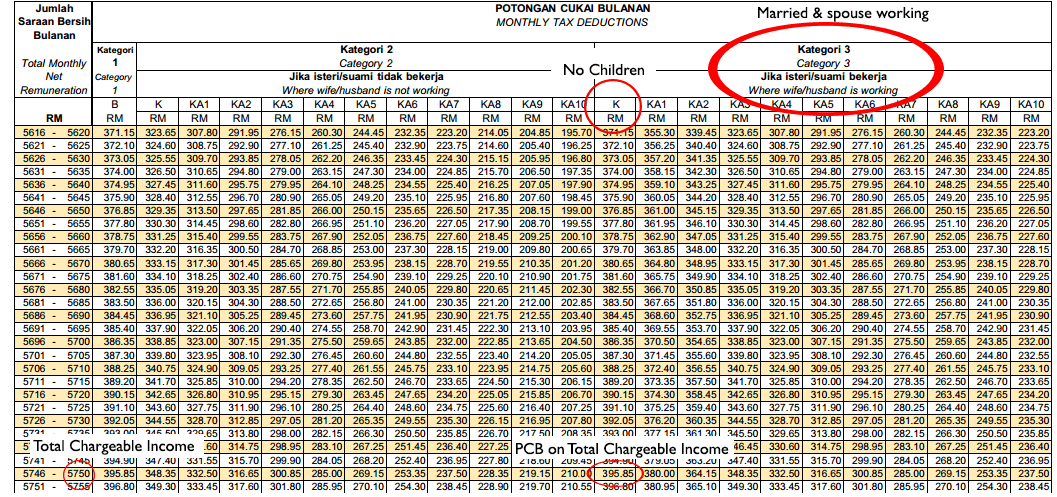

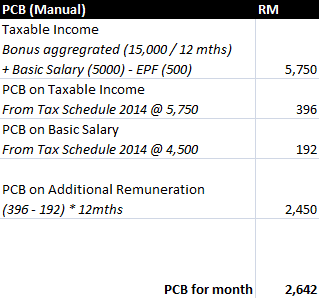

3B. Calculate manually using PCB Schedule

- Calculate your monthly taxable income

Calculate bonus divided up equally into 12month: Total Bonus / 12

+ Add current month basic salary

– Deduct current month EPF (employee) (Note: Max 500)

= Get Total Chargeable Income - Check the PCB Schedule for your PCB on Total Chargeable Income

- Check the PCB Schedule for your PCB on Basic Salary

- Calculate PCB on Additional Remuneration

( PCB on Total Chargeable Income – PCB on Basic Salary ) X 12months - PCB for Month = PCB on Basic Salary + PCB on Additional Remuneration

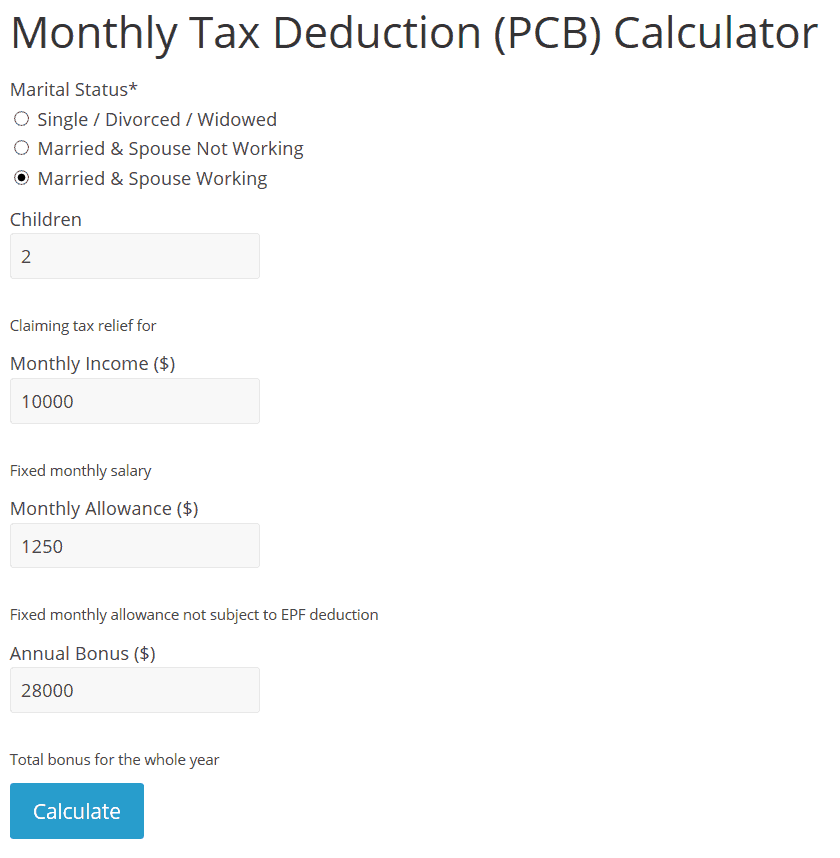

3C. Calculate using the MyPF Monthly Tax Deduction (PCB) Calculator

Calculator screenshot

- Key in marital status and children (if any)

- Key in monthly income, fixed allowances, and annual bonus.

- Calculate results.

- Monthly Tax Deduction (PCB) Calculator

FAQ

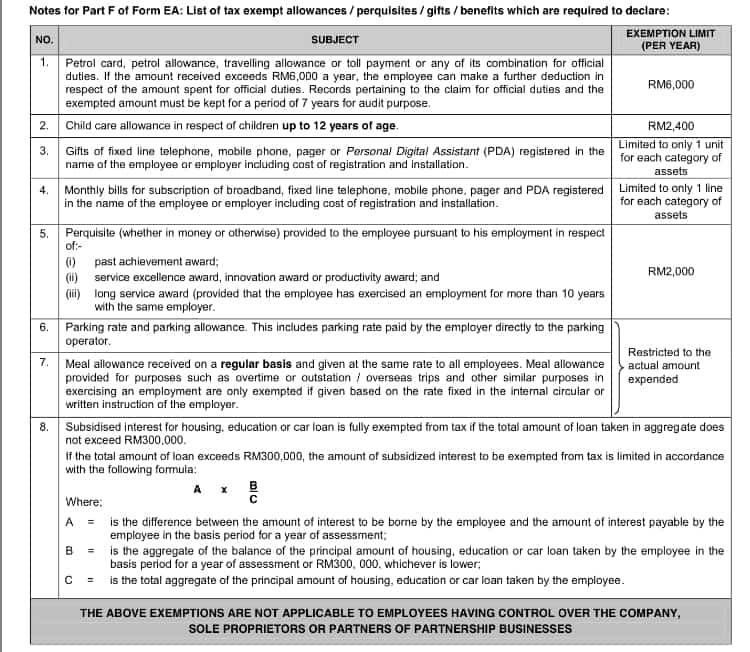

Q: I am getting employee benefits from my company. Is it taxable?

A: Employee benefits (aka perquisites) are considered income and taxable. There are some exemptions as below claimable.

Share and discuss on Malaysian Bonus & Tax Calculations

Does this accurately help you to estimate your PCB & take home pay during your bonus month(s)?

Is there any information that needs further clarification?

{kind=link}

{kind=link}

{kind=link}

Very very informative! I wish had seen this last year itself. Excellent Steve! :)

PCB for Month = PCB on Basic Salary + PCB on Additional Remuneration

1.Does the above include the deduction of tax for that current month salary ?

2. Or deduction for bonus only?

Regards,

jane

Hi.. this is very informative and clear. Question, what if the employee receiving bonus is relatively new – say only 5 months into the job? Should I multiply X6 when calculating PCB on Additional Remuneration?

Thank you.

Yau

Hi,

If i receive 7000MYR for month what are can be included in the allowances per month to avoid tax since i am a resident and indian national

Can you please share the

like this

Basic pay : 6000

Parking : 500

Petrol : 500

Can you help on this

Hi Stev,

If the new hiring company was buying the bond of existing company which I’m still work at. How the tax will be charge.

Let’s said the amount is RM35,000 ? Can the tax be relief ?

Hi, I have an Question, if only get pay for Bonus, which mean the Bonus Amount – EPF 11% – Income Tax (According to the Tax Table Schedule) = balance of the amount to be paid to the Staff, am I right? Bonus no need to deduct for Socso, correct me or not?

SOCSO Guidelines:

“Wages” for contribution purposes refers to all remunerations payable in money by an employer to an employee. Among the remunerations are as follows :

Payments that are not defined as wages are:

Under PCB Allowed Deductions, you mention that:

‘Contribution to EPF or other approved scheme – 12000 (500/mth)’. Is this 6000 per year or 1000 per month?

Great article. Thanks!

Hi,

If Phone Allowance subject to monthly PCB Contribution?

Thanks

Hi, If basic salary and bonus to be paid separately by employer. Is the PCB calculation for bonus is the same as above formula?

Hi! I’m Ryan here. I would like to know is medical leave & annual leave will consider in bonus payout.

E g : Salary + allowance – epf – PCB – medical leave – annual leave =

Many thxs

Hi! If I receive my bonus in Jan 2018, so how do I calculate my tax amount?

Hi,

Suppose if I get a Salary of RM 7,000 anually and I have Annual Leave Encashment of RM 4,000 for last 12 Months which is to be re-imbursed in February. What should be my total tax Deduction? Please advise.

1) Will it be for RM 11,000 (RM 7,000 + RM 4,000) as a whole

2) or Will it be RM 7,000 Tax + RM, 4,000 tax

Hi,

I would like to know the calculation on monthly PCB deduct on my payslip, as i do the calculation and refer to the PCB schedule above, result is different.

example: basic salary RM4k, Allowance RM1k, performance bonus monthly RM1k, how is the PBC calculate ?

Hi, I’m Ken here. a car salesman with earning Basic + Commission. I would like to ask a question that help all of the salesman. Let’s say my commission for 1 car is RM2,000, I promise to give a full tank petrol, car tinted film, smart tag for my customer that cost me around RM1,200 on my own. so how to i declare the income tax which I’m not earning RM2,000 per car? because at the end of year mayb my annual total basic + commission is RM80,000 on EA form. But actually after deduct the free gift, my Annual income is just RM50,000.

Hello, I am Jean. My company supports me on schooling costs. They pay directly, and school cost does not appear anywhere in my payslips. Is this a benefit taxable at my level, or is this similar to other types of company supports (e.g. temp accommodation during relocation), so not taxable benefit for me?

Hi, if my bonus out on Feb 2018 for previous year 2017 remuneration. Separate payslip with Feb 2018. My 2017 EA form doesn’t cover this bonus. So should I fill it in 2017 or 2018 (next year) income tax?

I am getting outstation allowance from my company. Is it taxable & also needs to declare in Form EA ? Please advice . Thanks.

What is the advantages/disadvantages (in terms of PCB and EPF deduction) of having bonus being paid together with salary versus bonus being paid separately?

Hi, I am Precilla here, I have a doubts for the Bonus payout example for Remuneration of YA 2018, we had pay the balance of Bonus during Feb’2019. Of course the EA form will not show the amount which is paid in Feb 2019.

they will be 2 scenario.

Scenario No.1

Bonus been accrued in the book during Dec 2018. Then payout during Feb’19

Scenario No.2

Bonus DO NOT accrued in to book and the bonus payout for the remuneration of YA 2018 during Feb’19

My question is for personal tax, do I need to declare my income for YA 2018 or 2019?

Foreign worker (PLKS permit) arriving on 31st August 2019, start work on 1st September 2019 and 1st month salary RM 1,500.00..

How to calculate his 1st month pcb?

Link: https://mypf.my/mtd-pcb-calculator/

Hi Will like to know the due to the current unstable economy if terminated by the company and given of lump sum pre-tax payment of RM108,000. May i know is it taxable? If yes, may I know the amount and can seek for EIS claim?

http://www.perkeso.gov.my

PCB borne by employer is taxable in basis year or following year ? any public ruling related..

http://www.hasil.gov.my/bt_goindex.php?bt_kump=5&bt_skum=3&bt_posi=1&bt_unit=5100&bt_sequ=6

If company granted options to employee and allow to encash. The tax should under which category?

Hi,

How do i get the deduction for this wife not working RM4,000? My wife is not working since 2019

PCB allowable deductions:

Deduction for husband or wife – 3,000 in Y2014 4,000 (if spouse not working)

Hi, if my bonus RM 60,000 accrued in Year 2017 company Account and received half RM 30,000 in year 2020, so pcb should declare in my year 2020 income? Only declare half or full?