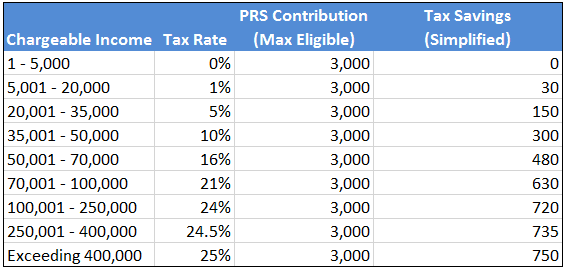

I am currently at the 21% tax bracket & would like to maximize my tax incentive (relief) of Private Retirement Scheme (PRS) contribution of RM3000. Let me know what you suggest.

Based on simple tax calculation, you would enjoy tax relief based on your tax bracket (below as of Y2016)

Option: PRS Unit Trust Fund

Checking on a UT ranking site like LipperLeaders would show you various PRS fund options in Malaysia.

(Source: LipperLeaders.com)

As of time of writing, recommended would be one of the following with near 5 ratings in all categories. The links below open through Fundsupermart which is an online discount UT brokerage.

- RHB Retirement Series – Growth Fund

- RHB Retirement Series – Conservative Fund

- CIMB-Principal PRS Plus Asia Pacific Ex Japan Equity

Option: Private Retirement Pension Scheme

Another option to consider besides a PRS fund is a private retirement pension scheme. This works similarly to pension schemes. However, the initial funding for the pension scheme (e.g. RM3000 investment annually) would come from the individual himself/herself.

The pension scheme then would pay out a pension when the person reaches age 60 (or to next of kin if the person passes away at an earlier age). To qualify you will need to be below 50 or 55 depending on the private retirement pension scheme.

- Pros: Returns are secure & contractually guaranteed with IRR between 4-4.8%

- Cons: There is a minimum commitment of typically 10 years of investment

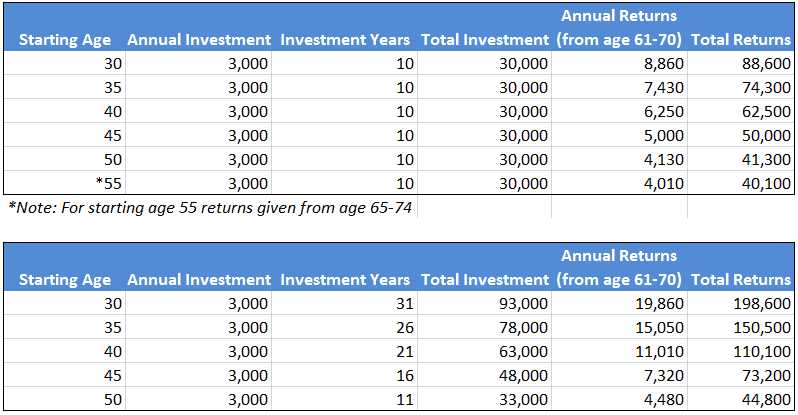

Examples:

Starting from age 30, you place in RM3,000 per annum

- If you invest for 10 years & then stop investing. you receive RM8,860 per annum for 10 years from age 61-70 (Total returns RM88,600)

- If you invest every year from age 30 until age 60. you receive RM19,860 per annum for 10 years from age 61-70 (Total returns RM198,600)

Interested in maximizing your PRS tax relief OR simply to improve your Personal Finances?

Contact us!

{kind=link}

{kind=link}

{kind=link}

Leave A Comment