Seeking Income in Times of “Uncertainties” (Fixed Income; Bond Market)

By Kho Hock Khoon, Senior VP Fixed Income, AmInvest

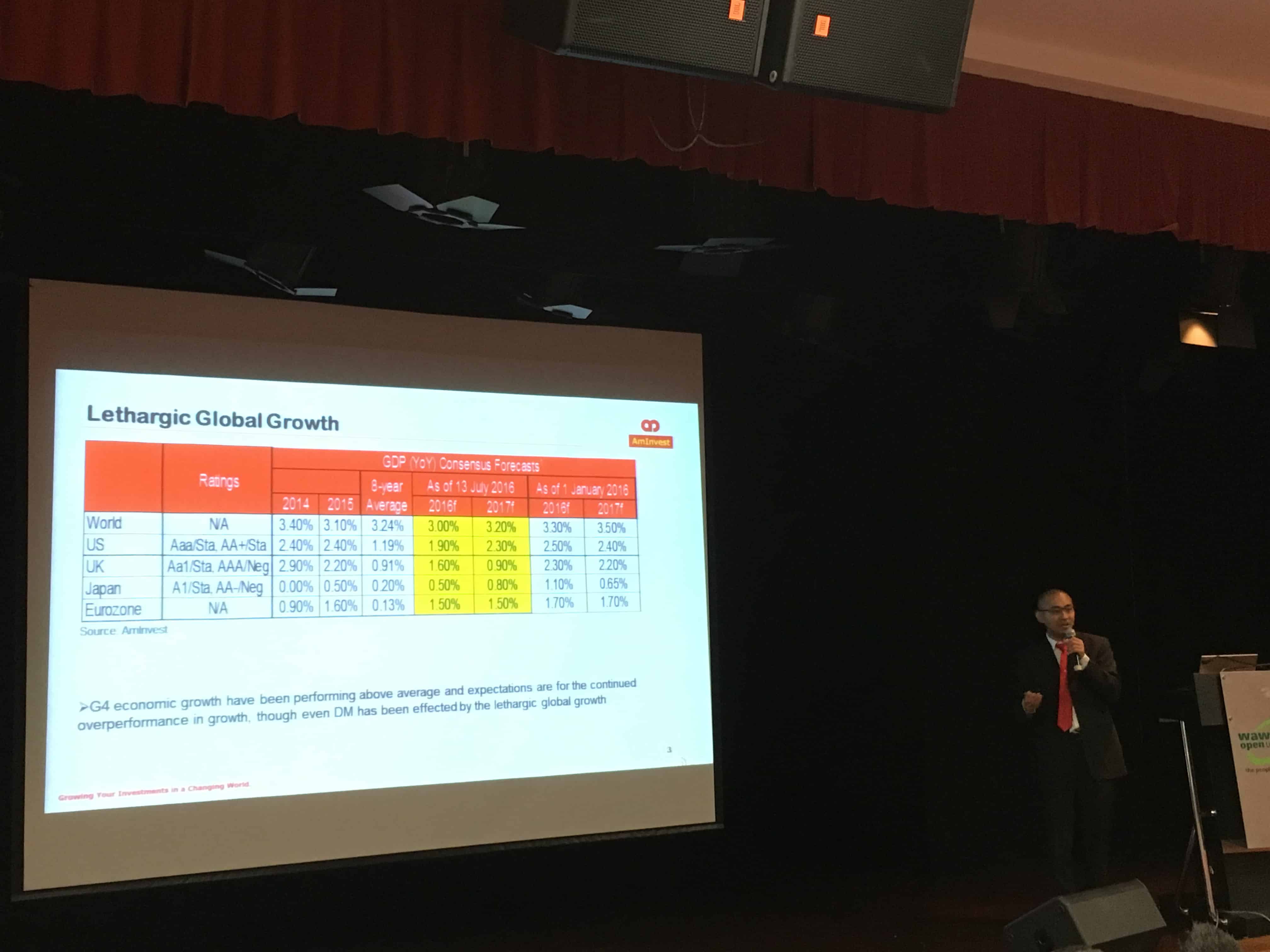

Key Highlights of Global Market

• Global growth modest

• Disinflation continues (est 3.2%)

• O&G prices proves disinflation

• US jobs data: employment trend healthy but job creation soft/mixed recently (Feds hiked int rate late 2015 w good employment data)

• US private sector sentiment tapered off (below avg)

• US wages tapered off (below avg)

• US 10-yr treasury yield fallen over 3016 as expectations of further hikes reduce

• US rate hike probability 41% (2016 Dec) / 43% (2017 Feb) / 49% (2017 Mar) (source: AmInvest)

• Hiking Policy Rate: US, Chile, Mexico

• Easing Policy Rate: Malaysia, Russia, Philippines, South Korea, EU, Japan, Aus, India, NZ, etc

Brexit (2016 Jun) Impact on Malaysia

• Remains unfolding & early days to access

• Malaysia: ltd trading partner (1%) but larger impact from EU (10%)

Malaysia & GDP

• GDP Growth Q1: 4.2%

• All softened (public spending, etc)

• Q2 forecast 4.0-4.5%

• Inflation: 1.6% (low; not a concern)

• Exports: -0.9%

• Imports: +0.3%

• Capital Goods Import: -0.02%

• Unemployment Rate: 3.1% (expect to rise)

• Consumer Index: all time low (GST; MYR drop)

• Big ticket items sales (eg cars): negative growth

Palm Oil; O&G

• Palm Oil: CPO pricing negative

• O&G: oil prices rebounded (saving grace; lag 3-6mths)

• OPEC & US oil production: US Cut production & drilling rigs -50%; non-OPEC maintain/slight reduction; expect oil prices increase

Ringgit & Reserves

• Malaysia Foreign Reserves: +2b (2016; stabilised; MYR not as gloomy as sentiment holds)

• Onshore & Offshore Ringgit: no foreign sell-off; spreads are normal

Banking Loan Growth

• 2016 May: +6.2% (slowest in 3yrs; cautious in banking)

• Gross NPL ratio: 1.65% (banks even more cautious)

Property

• BNM controls slowed price rise in property market

• Less new launches

• Property inventory held by developers reducing

Government Securities

• Foreign Holding of MGS: 49.8%

• Foreign Holdings: only 32.4% if include Islamic securities

• 2015: foreigners net buyers

• 2016: 6 consecutive mths foreigners net buyers

• 2016 Jun: 5b in bonds

• 10-yr Yield looks attractive vs other regional countries (Aus, S Korea, Thai, China)

• Strong rally following Brexit

• Expect rally in MGS

• PDS-AAA (corporate bonds) 3/5-yr credit spreads attractive

• MGS benchmark returns (YTD returns 3.86%)

Strategy

1. Market sentiment in the near term will likely be dictated by the developments arising from Brexit as well as its implications on the US Fed fund rate hikes

2. With BNM’s expectations of a moderate inflation outlook & slower economic growth forecast for 2016, the OPR is likely to stay at its present level of 3.25% this year. However, we do not discount the possibility of a rate cut this year should downside risk to growth materialises & significanly slows down domestic economic activities.

3. Given the uncertain outlook from a diverging global economy as well as The uncertain economic implication arising from Brexit, we remain cautious & advocate reinvesting & participating in new issuances to capitalise on more attractive yields.

Bond as asset class has lower volatility

What is your risk profile?

Money market to pure bonds?

Investment term? (Min 1-yr)

Q&A

Q: Bonds BBB promoted back to investment grade?

No local corporate issues depreciated to BBB & very small % (<1%) of universe. Generally safe. Advise to read prospectus. Local fund usually higher grades. However offshore may be different possibly including BBB.

Q: Suggestion to take car sales out of equation

Yes prefer Ubee over taxi. But car ownership is different as is own car & private transport. Not in near future.

Q: What if 2 different bond ratings?

Fund houses will use lower rating

Q: Bond funds returns same as a bond?

Generally if you buy a bond at 4.5%, generally expect bond fund returns at 4.5% (possibly higher).

(E&OE. For info sharing purposes only not affiliated with FSM or AmInvest)

{kind=link}

{kind=link}

{kind=link}

Leave A Comment