Useful reference information on Malaysian Income Tax 2017 for year of assessment 2016 for resident individuals. E&OE.

Contents

Key Malaysian Income Tax Info

Do I need to file my income tax?

Yes, you would need to file your income tax for this past year if:

– You spent at least 182 days in the past calendar year in Malaysia, OR

– You spent at least 90 days in Malaysia in each of at least 3 out of 4 preceeding years.

AND

– Your income after EPF deductions is above RM34,000, OR

– You have filed your income taxes in any years prior.

What is considered “income”?

All income received in 2016 from taxable sources including employment, tuition classes, businesses, commissions, direct sales, rent, royalties and other income as stated under section 4 and section 4A of the Income Tax Act 1967 must be declared.

All supporting documents pertaining to tax relief and expenses must be kept for seven years for audit or investigation purpose.

When do I need to fill my taxes by?

Submission of Income Tax Return Form (ITRF) for Year of Assessment 2016 via e-Filing can be furnished commencing from March 1, 2017.

Individuals without business source: March 1 – April 30 every year

- BE Form, for individuals without business source

- M Form, for a non-resident individual without business source

Individuals with business source: June 1 – June 30 every year

- B Form, for individuals with business source

- M Form, for a non-resident individual with business source

- P Form, for partnership

Tax Payment Methods

- Credit Card (Visa, Master, AmEx)

- Internet Banking (CIMB, Citibank, Hong Leong Bank, Maybank, Public Bank, RHB Bank)

- Bank Counter (Affin Bank, Bank Rakyat, Bank Simpanan Nasional, CIMB Bank, Maybank, Public Bank, RHB Bank)

- ATM (CIMB, Maybank, Public Bank)

- POS Malaysia (Cash only)

- Telegraphic Transfer (TT) / Transfer Interbank Giro (IBG) / Electronic Fund Transfer (EFT)

Tax Refund

Tax Refund (if any) will be credited into the account automatically to the taxpayer within 30 working days after the submission of Income Tax Return Forms (ITRF).

Tax Penalties

Failure to file income taxes

No prosecution: 300% tax payable

On conviction: RM200 – RM200,000 / imprisonment

Incorrect tax returns by understating income

No prosecution: 100% tax undercharged

On conviction: RM1,000 – RM10,000 & 200% tax undercharged

Incorrect tax returns by understating tax liability

10% on difference between tax underestimated & 30% of actual tax payble

Late payment

10% tax payable & additional 5% on outstanding if not paid in 60 days

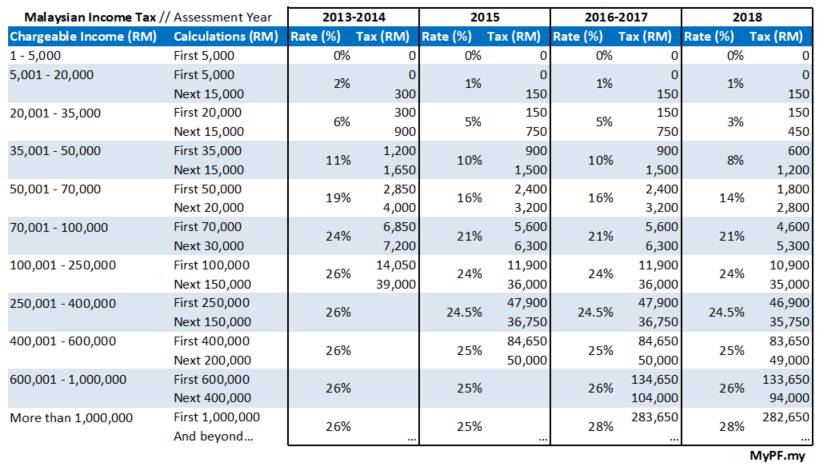

Income Tax Brackets

Key Change from 2015

Progressive chargeable taxes above RM600,000 at 26% (previously 25%) and above RM1,000,000 at 28% (previously 25%)

Income Tax Rebates

- Self: RM400 (chargaeble income below RM35,000)

- Spouse: RM400 (chargaeble income below RM35,000 and spouse no income)

- Zakat/fitrah (Muslims only): up to maximum tax charged

Income Tax Exemptions

- Individual and dependent: RM9,000

- Disabled individual: RM6,000 (additional)

- Wife/husband/payment of alimony: RM4,000

- Disabled wife/husband: RM3,500

- Cost of basic supporting equipment for disabled individual (self/spouse/child/parent): RM6,000

- Medical expenses on serious diseases: RM6,000 (including up to RM500 for complete medical exam self/spouse/child)

- Education fees (self): RM7,000

- Purchase of books/journals/magazines (including electronic copy; excluding newspapers): RM1,000

- Purchase of PC once every 3 years (excluding tablet/hybrid/phone): RM3,000

- Deposit in SSPN for children: RM6,000

- Purchase of sports equipment (excluding clothing, shoes): RM300

- Housing loan interest (SPA from Mar 3, 2009 – Dec 31, 2010): RM10,000

- Deduction for children:

- Under 18: RM2,000

- Above 18 & schooling: RM2,000

- Above 18 & Higher Education schooling: RM8,000

- Disabled child: RM6,000

- Disabled child & Higher Education schooling: RM14,000

- EPF and life insurance (self/spouse): RM6,000

- PRS and annuity: RM3,000

- Education and medical insurance (self/spouse/child): RM3,000

- SOCSO: RM250

- Deduction for parent (father/mother): RM1,500 each

- OR Medical treatment/special needs/care expenses for parents: RM5,000

- Note: amount is shared among all children in any proportion desired up to the exemption limit

More Info

- 2016/2017 Malaysian Tax Booklet (pwc)

- LHDN official website / eFiling (hasil.gov.my)

- What may alert LHDN to investigate you for tax evasion! (malaysiandigest.com)

- Malaysian Income Tax 2018

FAQ

- Q: What tax deductions are applicable for medical treatment/special needs/care expenses for parents (RM5,000)?

Tax deductions for medical and healthcare expenditures for the parents only is eligible for claim regardless of the parents’ total income. The expenditures comprise:- Medical treatment expenditures who are diagnosed with diseases/physical/mental disabilities, and healthcare services supported by receipts issued by medical practitioners registered under Malaysian Medical Council (MMC), pharmacies or licensed drug stores; or

- Special needs expenditures such as nutritional food and disposable diapers prescribed and endorsed by medical practitioners registered under the MMC and supported by receipt.

- Q: For rental income, can I deduct expenses?

Yes for expenses incurred after property rented out are deductible from the rental income. Examples are assessment and quit rent, loan and fire insurance premium, expenses on rent collection, expenses on rent renewal, expenses on repair and service charges.

No for initial expenses before property rented out. Examples are costs of obtaining the first tenant for the property (advertisement, introducer’s commission, legal fees for preparation of tenancy agreement), other expenses incurred prior to the property being rented out, renovation and improvement costs.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment