Should I invest in SSPN Prime (previously known as SSPN-i and before that SSPN1M) for my child’s higher education? What are the returns, pros, and cons?

Updated: Jul 1, 2023

Contents

What is Skim Simpanan Pendidikan Nasional (SSPN)?

SSPN (National Education Savings Scheme) is a savings scheme for higher education launched in 2004.

SSPN was introduced by the Goverment through Perbadanan Tabung Pendidikan Tinggi Nasional (PTPTN) aka National Higher Education Fund Corporation.

Depositors agree for PTPTN to manage and invest their deposits under the Islamic concept of “Wakalah Bil Istithmar”.

SSPN offers returns of ~4% and annual tax relief of up to RM8,000.

From 2012, having a SSPN account is a pre-requisite for taking a PTPTN loan.

From 2018, SSPN is renamed as SSPN1M (SSPN 1 Malaysia).

From 2019, SSPN is renamed back to SSPN-i.

From 2021, SSPN-i is renamed to SSPN Prime.

SSPN Eligibility Criteria

- Malaysian Citizen

- Depositor: Age 18-64

- Child Beneficiary: Age below 29

- Min account opening: RM20

Account Opening

- Online or via MyPTPTN app

- PTPTN counter/ agent

- Banks: Maybank, Bank Islam, Agrobank, Bank Rakyat, or RHB Bank

Note: There are no restrictions on accounts you can open.

SSPN Benefits

- Child qualifies for PTPTN loan application for higher education.

- Parent/guardian tax relief of up to RM8,000 (previously RM6,000) per annum ONLY for parent/guardian of qualified child beneficiary.

Note: If both parents filing joint tax relief, total is for combined limit only. - Free takaful insurance with minimum deposit RM1,000.

- Consideration for matching grant of up to RM10,000 for eligible families with monthly base pay below RM4,000.

- Savings guaranteed by the Malaysian government.

- Competitive dividends which are tax-exempt.

- Flexibility to save in any PTPTN branch, 3000 agent locations, and via online banking.

SSPN Prime Returns

SSPN Prime Historical Returns

| Year | Dividend % |

|---|---|

| 2004 | 3.00 |

| 2005 | 4.00 |

| 2006 | 4.00 |

| 2007 | 4.00 |

| 2008 | 4.00 |

| 2009 | 2.50 |

| 2010 | 3.25 |

| 2011 | 3.75 |

| 2012 | 4.25 |

| 2013 | 4.25 |

| 2014 | 4.25 |

| 2015 | 4.00 |

| 2016 | 4.00 |

| 2017 | 4.00 |

| 2018 | 4.00 |

| 2019 | 4.00 |

| 2020 | 4.00 |

| 2021 | 3.00 |

Average: 3.84%

Median: 4.00%

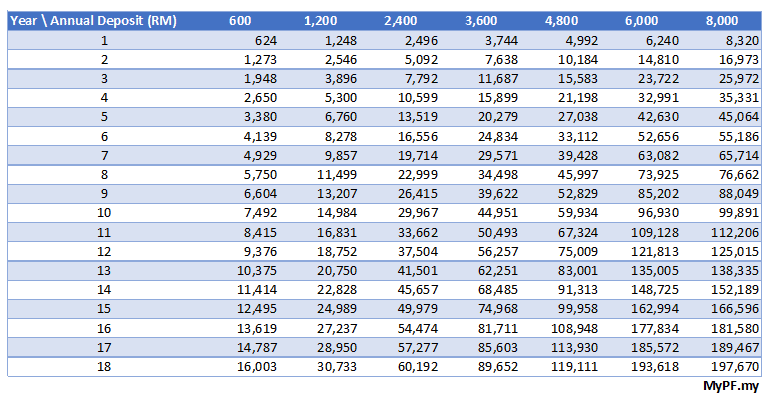

SSPN-i Estimated Returns

SSPN estimated returns based on 4.0% p.a. compounding

SSPN Prime Bonus/Loyalty Incentive

- 2018: Matching RM500 savings for RM500 invested in for children aged 7-12

- 2019: Bonus 0.50% during campaign Jan 1 – Apr 30, 2019

- 2020: Bonus 1.00% during campaign Feb 5 – Apr 30, 2020

Criteria

- SSPN-i account opened for at least 3 previous calendar years.

- No withdrawals made during campaign period.

- Minimum RM1,000 in account.

- Minimum RM500 additional investment made.

- Maximum RM8,000 incentive given per account.

SSPN Tax Relief

Tax relief of up to RM8,000 (increased from RM6,000 for SSPN-i) per annum for parent/guardian saving SSPN-i for their child.

For parents with separate tax filing and separate SSPN-i account for child, each parent qualifies for tax relief up to RM8,000 each per annum.

SSPN child account must be opened before age 18 to qualify for the tax relief (with annual contribution) until child turns 29.

Note: Self contribution accounts not qualified for tax relief

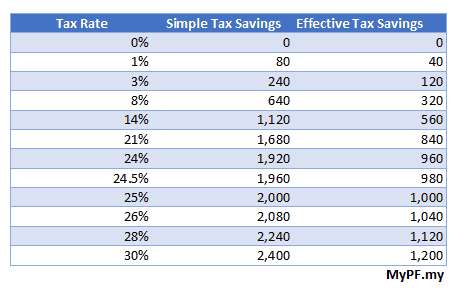

Tax Relief Example

Tax Savings example above based on RM8,000 p.a. SSPN deposit. Effective tax savings is an estimate based on ~50% simple tax savings as Malaysia is on a progressive tax bracket. Run an online tax calculator or check with a tax consultant for more accurate tax savings.

How to get SSPN Prime Tax Statement for LHDN

- Login to PTPTN services menu

- Select Penyata Hasil

- Download/save statement

SSPN Takaful Insurance Benefit

Coverage: Death, and Total and Permanent Disability (TPD)

Death Benefit:

- Ringgit matching deposit amount

- RM2,000 (depositor)

- RM500 (beneficiary)

TPD Benefit:

- Ringgit matching deposit amount (up to RM2.5m maximum)

SSPN Contribution Methods

- PTPTN Counter: debit card/ATM card

- JomPAY

- Salary auto-deduction

- e-SSPN-i online portal

- PTPTN agents

- Boost e-Wallet

SSPN Account Withdrawal and Closure

SSPN Withdrawals

- SSPN withdrawals can be done online through the SSPN portal.

- SSPN partial withdrawal can be at any time with min RM20 to keep account active.

SSPN Account Closure

- SSPN complete account closure can be done at any time.

- You can opt to reopen your account again

- SSPN account closure also occurs upon depositor death.

- SSPN account closure requires submission of deposit withdrawal form, account closure form, copy of savings account book front page, and matching grant form/death certificate/other relevant documents (if applicable).

- Account closure process time frame is 14 working days with full and complete documents submission.

Overall on SSPN

SSPN is an option to save for your child’s higher education for tax benefits, provided returns continue to average ~4% above, and you do not mind your funds being tied down in the account.

Pros

- Tax relief is decent especially if your chargeable income is at least above RM35,000 (above RM2,916 monthly).

- Low PTPTN repayment interest charges.

- Extra perks of PTPTN loan qualification and scholarships for excellent educational results and free takaful insurance coverage.

Cons

- There have been some complaints about inefficiencies and delays for funds disbursements.

- PTPTN has faced difficulties collecting back loans made out although PTPTN has since denied it is facing any financial difficulties.

- If you don’t pay back your PTPTN loan, it will affect your credit score and you may be blacklisted.

More Info

- SSPN- Prime online account status, deposits and tax relief statement (ptptn.gov.my)

- Tax calculator (hasil.gov.my)

FAQ

Q: Can I open a SSPN-i account if it is not my child? Can I claim tax relief?

You need to be the legal parent or guardian of the child. Tax relief is only for the legal parent or guardian.

Q: Can I open a SSPN-i account if my child has a birth certificate but not MyKid?

A: Yes you can at SSPN-i counter. You are encouraged to update the record once MyKid is available.

Q: Can I open a SSPN-i account for my child even though I am declared bankrupt?

Yes you can.

Q: What banks (agents) can I make payments through?

Maybank, Bank Islam, Agrobank, Bank Rakyat, RHB Bank, CIMB Bank, and BSN.

Q: Does the SSPN tax relief include dividends?

No. Only the (up to) deposited in the year qualifies for tax relief. SSPN dividends are tax exempt though.

Q: Will dividends be given if I withdraw the amount before dividends are declared?

A: Yes but pro-rated on monthly basis.

Q: What is SSPN-i Plus? Will I qualify for another RM6,000 tax relief?

SSPN-i Plus although similar sounding is different from SSPN. SSPN-i Plus is takaful (insurance) coverage which costs you from RM30 upwards monthly providing. This qualifies for a further RM6,000 tax relief BUT only if you have not maxed out your EPF/life insurance contribution.

Q: After graduation, can child continue to maintain SSPN? e.g. for post-grad studies. If yes, does the parent/child get tax relief?

Yes, SSPN-i accounts can be continued on. Tax relief would only be for parent as depositor paying for child beneficiary. The child account must be converted to an individual account at age 29 to continue saving with SSPN.

Q: Does account closure have to be for one of the reasons stated above?

A: Checking with PTPTN, you can close your SSPN-i account (full withdrawal) at any time (not necessarily for withdrawal from child withdrawal from education/public university or other reasons listed above).

Q: Is SSPN protected by PIDM?

A: It is protected/guaranteed by the government. But not under PIDM.

{kind=link}

{kind=link}

Is tax relief allowed for EPF self contribution by the self employed?

I am self employed aged 64.

I pay my own EPF contribution.

Am I allowed tax relief up to 6000 p.a.?

Am working for a company and I am Single age 56 years old.

Can I apply for SSPN.

Will I get a tax relief up to 6,000 p.a.

I have open a SSPN account last year for the tax relief purpose. However should I continue to invest ANOTHER 6,000 this year so I can get the tax relief next year?

Is sspn or sspn-i account protected by PIDM?

I am still under employment. My son, aged 25, starts employment this year (2017) . MY query :

a) Can I operate a SSPN account with my my son as beneficiary, even though he has started employment ?

b) If the answer to (a) above is “YES”, am I entitled to Tax Relief for Resident Individual up to RM6,000.00 as per LHDN regulation?

c) If the answer to (b) above is “YES”, will my SSPN Tax Relief entitlement lapse upon my Son attaining age 29 i.e. in 2021 year of assessment?

Thanks.

Rgds: Kenneth Tan

What is the maximum deposit sum within a year?

Hi. If both me and my husband are filing separate tax claims, can both os us open accounts for the same child name?

hi, if my Husband had open an Account sspn-i for my son, can myself open another new account with my son again for claiming tax Relief under my personal tax 8k?

compare SSPN-I and SSPN-I Plus, which one is better?

hi.. if i already have the sspn-i plus account, i need to deposit 6k in order to qualify for the tax relief right? does the 6k include takaful contribution as well? thanks!

I have a SSPN account for my child. But If let say, i need money for use, in THAT situation , am i allowed to withdraw the money for myself to use anytime?

Hi there,

I have opened SSPN account deposited RM6k in 2016 and gotten my tax relief for the year 2016. If I would want to have my tax relief for year 2017, meaning I have to deposit another RM6K by end of 2017 is it? Thanks

Hi, based on your post

“SSPN partial withdrawal is only allowed after 1 year. SSPN partial withdrawal amount is only allowed once a year for RM500 OR 10% of account balance (whichever is lower).”

I thought SSPN can withdraw at anytime. The above only applies to SSPNi+ right?

Hi what about SSPN? Can i apply to withdraw in full at anytime as well for SSPN and where can i get the withdrawal done? Thanks

If we can withdraw anytime , let say I had deposited RM6000 last year, wont that mean I can withdraw it and bank it in again just to have the tax rebate?

If I have 2 kids, can I deposit 6k to the first one, and withdraw next year and deposit to another kid account to claim the tax relief?

Hi I have opened account for my two kids. May I know if the amount entitled for deduction is net saving in to SSPN as a whole or by individual sspn account ? What is the amount entitled for tax relief in 2016 & 2017 for below scenario. Thanks.

Kid1 : deposited 6 k in 2015 and withdraw 6 k in 2016. Just deposited 6 k in 2017.

Kid 2: deposited 6 k in 2016 and withdraw 6 k in 2017. No deposit made in 2017.

Hi, the question ask above is:

for Kid1, deposited of 6k in 2015 entitled for tax relief. (Saving done)

in year 2016, withdrawal of 6k. Expected, no relief.

in year 2017, deposit 6K again. would he/she get the tax relief for year 2017?

how a non malaysian but a Resident pass holder for 10 yrs can open a SSPN account for his children?

My daughter is enjoying PTPTN loan for her university education. She has open an SSPN-i, when i deposit into this account :-

(1) Am i entitle to my personal income tax relief on RM6K deposited?

(2) Will the money in SSPN-i automatically pay down partially her student loan when she graduates ?

Thanks

I have called the PTPTN careline to check and there would be no condition for withdrawal. Can you please confirm that the conditions below are correct?

SSPN account closure and withdrawal conditions:-

Child offered a place in approved higher learning institution.

Child voluntary withdrawal from education system.

Child has been expelled.

Suffering from incurable critical illness certified by doctor.

Depositor/child total and permanent disability or death.

hi , may i know if can exempted the tax every year in the following scneario every years? :)

Year1. 31/dec/2017 deposit 6k to sspn and then widthdraw all $ on 2/jan/2018

Y2. 31/dec/2018 deposit 12k to sspn and then widthdraw all $ on 2/jan/2019

Y3.31/dec/2019 deposit 18k to sspn and then widthdraw all $ on 2/jan/2020

Y4.31/dec/2020 deposit 24k to sspn and then widthdraw all $ on 2/jan/2021

Y5.31/dec/2021deposit 30k to sspn and then widthdraw all $ on 2/jan/2022

and sequence year until kids year 29?

please advice.

thank you.

The one who tried would not want to make this public. As soon, the regulation will change. Brilliant!

I have an account few years ago through CIMB, i wanted to continue, please contact me where to bank in the money.

Link: PTPTN Branches

Hello there. i don’t understand regarding the tax relief example table. what does it mean by tax rate, simple tax saving and effective tax savint. FYI, i monthly income is roughly 6k. thank you in advance.

Hello there. Applying online on the PTPTN website is so confusing. If I am applying for an account for my daughter who is 1 year old, what type of account should i select?

1. Akaun untuk Anak Jagaan yang Sah

2. Akaun untuk Diri Sendiri

3. Akaun lain-lain

I am assuming “Butir-butir Pendeposit” refers to the parent, and “Butir-butir Penerima Manfaat/Diri Sendiri” refers to my daughter?

Would you recommend opening online or going via one of the banks?

I deposited additional sum on 28 Dec. through online payment to add up to the total of RM6k investment for 2017. Will the last minute deposited amount count on for the year 2017 tax relief or it will be forwarded to 2018?

Hi Admin,

Thanks for your detailed post and for answering each and every question from visitors.

I just opened an account for my daughter via the PTPTN portal https://www.ptptn.gov.my/esmas-open-acc-web/#/openAccount and paid online, etc. Also got the transaction receipt via e-mail.

But how do I log-in to view the account, or perhaps get any acknowledgement/proof that I have opened the account?

Link: https://www.ptptn.gov.my/saving/sspnlogin.html

Did I mention you are awesome?!

Thanks again for all your help and great content. Happy New Year to you!

Hi admin, I’ve opened an SSPN-i account for my daughter, but now that I’ve changed my mind, how do I upgrade it into SSPN-i plus? Or should I open another account?

Thank you for the prompt reply!

Hi, I have registered my kids for SSPN-i Plus and is paying a monthly commitment for RM50/month/child.

I saw that RM10 is been deducted monthly. If i top-up the account to RM1000, will i get the free insurance (thus you wont deduct the Rm10/month)?

TQ

so, the rm10 is deducted right? means i only save rm40/month rigtht? sorry im a bit confused. tq

Hi,. I need some clarification on below:

Both of my husband and myself are working and filing separate tax assessment. We have only one kid. In order to enjoy the maximum tax relief, please advice if :

a. Is the account no. different when both of us opened the SSPN accounts separately.

b. If yes, since my husband and myself deposit RM6,000 separately and snce we are filing separate tax, can both of us claim the tax relief of RM6,000 each.

c. If yes, my son will have 2 different SSPN accounts with combined fund of RM12,000.

Thanks in advance for the advice.

Good day! can I claim tax relief for the amount from both my children SSPN accounts? Pls advise thanks.

Hi there,

I have 3 accounts for my kids SSPN and need to know 1 of my son is 7 year old this year 2018. Did my son will get money rm500 bajet 2018. If yes please advice me which bank I can get.

is sspn same as sspn-i ?

Hi, admin

Noticed that every q is answered crystal clear n with a sense of humour.

My enquiry:

I hv an sspn account for my child.

Recently I got Anugerah Perkhidmatan cemerlang. The government gv 1k as reward which was deposited automatically in sspn account.

Does that mean I have 2 sspn account now?

Hi there, good day.

so SSPN = SSPN-i, all the benefit above will be same.

e.g. SSPN offers returns of ~4% and annual tax relief of up to RM6,000.

is that a way to check my Child’s SSPN account online? e.g. transaction.

Thank you.

https://www.ptptn.gov.my/saving/sspnlogin.html

hi,

is there a limits for this sspn-i ? i mean can i deposit for example 100k into this sspn-i, knowing its getting a good interest return rates ?

https://mypf.my/contact

I have opened a SSPN account. 2 question:

1) How and where to make deposit to SSPN account? Can bank in through Maybank?

2) How to withdraw money from SSPN account?

Thank you.

http://www.ptptn.gov.my/web/english-tutup/savings/withdrawal-closure

Hi,

(1) Do I still enjoy personal tax relief up to RM 12000 if I open a SSPN1M i (2018) account for my son and deposit RM 12000 into the account every year after 2021..? According to the T&C, I am eligible to gain tax relief from year 2018 until 2020, how about after 2020 until 2035, if I continue to deposit RM 12000 every year?

(2) Do the previous “pendeposit SSPN and SSPN-i” still can enjoy their tax relief every calender year until nowaday even they have brought it for more than 4~10 years?

Thank you !

Hi,

From 1 January to 31 December 2018, the government will give a one-off RM500 to 500,000 Malaysian students aged seven to 12 years old, provided they open an SSPN account with a minimum deposit of RM500.

https://simpanan.my/sspn1m/rm500-sekolah-rendah/

Hi, my son is 17 years old and not opening any account in ptptn. Am i entitle for the tax relief i bank in RM 6000 in sspn1m account.

Hi, Admin,

May I check with you the followings:

1) SSPNi+ is for insurance coverage, the 6k tax relief is max combined with EPF and other life insurance, right?

2) We only have SSPNi (previously SSPN, i.e. opened 9 years ago when my son was 7 then), not necessary to open SSPNi+ if EPF and life insurance already exceeded 6k, right? i.e. can’t enjoy further tax deduction.

3) SSPNi contribution entitlement for 6k tax relief is until YA2020?

4) For PTPTN loan application, is SPM certificate a must? If my son is sitting for IGSCE, he will not be entitled to apply for PTPTN if he is accepted by local private colleges?

5) If IGSCE results entitle to apply for PTPTN when accepted for higher education in local private college, is there a condition set for household income?

Thank you very much.

Hi Admin,

My daughter opened a SSPN-i account for her PTPTN loan when she was just over 18 years old. She is the pendeposit and Penerima Manfaat.

Question 1 : Can I (parent) claim for the tax relief of 6K if I deposit into her account?

My other daughter is just over 18 years old.

Question 2 : Can she open a SSPN-1 account?

Question 3 : If can for question 2, can I (parent) be the pendeposit and claim for the tax relief?

Many thanks

Hi Admin,

Thank you very much for your prompt respond.

1. Can I change the depositor to be MY name as my daughter is now the pendeposit and Penerima Manfaat (as printed on the card)? so that I can entitle the tax relief.

2. Even if my daughter is over 18 years old, can I still be the pendeposit and she is the child beneficiary?

Many thanks

Hi Admin,

Thank you for your very prompt reply.

How can I change the account to list me as the depositor so I can entitle for the tax relief?

Many thanks

http://www.ptptn.gov.my/web/guest/cawangan-ptptn

Hi admin,

There are some query required your clarification.

1. If I still don’t have child, can i create an account under my name (depositor and beneficiary both under my name) for my future child and claim the 6k relief now?

2. Who is the one that can withdraw the money? (depositor or beneficiary)

Thanks in advance.

Hi. I have my own SSPN account. If i deposit money into my account am i eligible for tax relief?

Is there an age limit for depositor ? If there is , what will be it ? Will this be a age criteria even though the depositor has a college studying child ???

I am working overseas and have 2 children studying in international school in the country we are living in. We are all Malaysians. Can we open accounts for our children? Any exclusions or constraints we should be aware of?

Hi,

I am a foreign national married to a Malaysian and my children are Malaysian by birth. If I have my Malaysian wife open the accounts, could I then deposit the SSPN contributions and claim the 6k tax relief?

What is the supporting document when withdraw the deposit?

I am a working adult of age 32 and not married nor having any child yet.

Can I still save a 6k in SSPN for tax relief purpose?

Hi,

I have just completed my study and started my fulltime job.

Can I take my SSPNi as a saving account by putting money in every month since it provides a better dividend compared to normal saving account?

I am still single so I am not looking up for the tax relief, just wanted to save some money up somewhere else other than normal saving account.

Just wanted to confirm:

1) am I able to close the account and take all my money back in the future for other financial purposes?

2) when I apply sspn i for my ptptn I just received a card, there is no bank book? Is that normal?I save money in sspn i via autodebit every month ever since.

High yield savings accounts

Contact MyPF

the returns is calculated based on savings or savings + takaful?

I’ve deposited a certain amount into my SSPN account sometime in December 2016 but wasn’t entitled to the dividend payout in 2017. I did the same thing in 2017 not knowing that and only got a dividend payout based on the carry forward balance from 2016. May I know when’s the typical deadline for any deposits to be qualified for dividend entitlement?

Hi,

1) If I want to claim for the tax relief for SSPN, the beneficially (my daughter) need to open the a/c before age 18?

2) Can husband and wife SSPN A/C put the same beneficially, and claim for separate tax relief (6k each)?

Thanks.

Referring to the same beneficiary but 2 different depositors (husband and wife), if husband deposit 3k, wife deposit 3k, can claim separately 6k?

Thanks in advance.

Hi,

I am interested in opening an account SSPN i PLus for my son .There are a few packages . I am keen on the BERLIAN . It says that the monthly contribution is Rm500, Rm 200 goes to saving and Rm 300 goes to Takaful. If I invest for 6 years, the amount I am getting back is Rm14400. What about the monthly Rm300 i paid monthly?

Kindly advise

Hi,

I am a foreign national married to a Malaysian and my children are Malaysian by birth. If I have my Malaysian wife open the accounts who is not working, could I then deposit the SSPN contributions and claim the 6k tax relief? If not is it mentioned on LHDN website?

https://mypf.my/pf/tax/

Hi i had bank in rm1000 in yr 2017 and i get tax relief for year 2017 rm1000. If i bank in rm500 for 2018, will i get tax relief for 2018 rm1500 or rm500?

Still have this incentive RM500?

SSPN1M matching grant (Insentif Geran Sepadan RM500 or GS500). Incentive of RM500 with minimum contribution RM500.

Age 7-12 in primary school

New contribution of RM500 in SSPN1M-i or SSPN1M-i Plus in 2018

Withdrawal only after age 18

For first 500,000 contributors only

Hi.

In 2017 i had deposited rm6k in my son sspn-i acc & didnt make any withdrawal in 2018.

if i didnt make any additional deposit in 2018, how much tax relief i can get for 2018?

tq

hi

is it difficult to make a withdrawal from the sspn-i account? can it be done through the bank?

Does PIDM cover SSPN investment?

This year , can I bank in RM 12000 and report tax relief RM 12000 for 1 person only? Can I get the refund if take cancel the sspn? Thanks

Hi,

I deposited 6k to my daughter, both can claim tax separately 6k or only 3k each?

Hi I just open a SSPN-i Plus Delima account, which means a committed Rm50 mthly deposit. If I deposit a sum of Rm1000, do I still need to deposit the mthly Rm50?

Hello, I have deposited RM6000 every year to my kids SSPN account. Every year my dividend is about RM1000/ year. Total dividend already >RM8000. Therefore, I would like to ask if I withdrawl RM8000 dividend out from my account for year 2019. Am I still entitled RM6000 tax relief if I deposited as usual RM6000 into my account. Possible the account can differentiate between dividend and principle?

Hi, good day.

i would like to know about the dividend payout timing each year.

mean what is the perfect timing to withdraw out the money, in order to get tax relief and also the dividend.

thanks.

Hi,

I married 2 years ago and have two step-children below 18 from my wife’s previous marriage.

Am I eligible to open a SSPN account?

Hi,

As I wish to open a SSPN-I for my step-son, do I have to go to a PTPTN office to open the account? or can I go to the branch of the designated banks? Do I need to bring any additional documents to confirm I am the legal parent? (my wife’s previous husband had passed away)

hi

im married malaysian n with longterm social visa.

im filing as malaysia residence of tax pay.

1) my husband has open child account under his name.

if i want to tax relief under my name, should i need to open again under my name?

or bank account under husband name and sspn beneficiary name can put my name?

2) if my epf ard 6k tax relief, which one can tax relief for other 6k? sspn i or sspn plus??

Hi Admin,

Would like to seek clarification on the SSPN account as below:

1) if i deposited 6K to the account in 2018 and withdraw it in Jan 2019, I can get the tax relief for 2018, correct?

2) since i have withdrew the 6K in Jan 2019, by Dec 2019, I will need to deposit “12K” in order to get tax relief of 6K, correct?

3) then in Jan 2020, i withdraw the 12K and by Dec 2020, i would need to deposit “18K” in order to get the tax relief?

Hi Admin,

I understand the tax relief I based on net difference between deposits & withdrawals for the respective tax year, If let say, I have withdraw the deposit e.g. MYR6k, without any new deposit being made for the year , will this resulted a negative MYR 6K impact on my tax assessment , and I need to pay extra tax on negative MYR6k ?

Questions 1

If my son is over 18 and I open sspn account with me as depositor and son as benefitionary. I still entitled for tax releave

Questions 2

Do we need to have sspn account before can apply for PTPTN loan ?

Hi, my kid is 15 this year and I wish to open an account to finance probably further studies in future. Is it too late? Will the loan amount be subjected to the balance sum in my PTPTN ?

Hi Admin,

1) If my children turn 29 years old in 2019, does the contribution in year 2019 qualify for tax relief?

2) And if I turn 65 next year, year 2020 (August), does my contribution in year 2020 qualify for tax relief?

Hello,

Question:

I have continously deposited money into my kid

sspn account, Yr 2018 my sspn account dividen about 1000, can I just deposit 5000, to claim for 6000 tax relief for the year.

Thanks

Hi

I have invested for the past 3 years. Say , in 2019 I dont invest as my income is low and benefit little in tax relief and i make a withdrawal of 5k in Dec 2019. in 2020 I make 8k contribution . Will I get the full tax relief of 8k in 2020 ? Or will the 5k withdrawal be deducted in 2020 tax relief ? Please advise

Thank you

HI, please explain

i plan to homeschool my daughter in couple of years. (2 yo) and plan to send her to oversea to continue her studies once she completes her IGCSE exam.

Can i invest in SSPN-i and withdraw the amount for her studies in overseas later on.

Please clarify.

Thank you

My last contribution was done in December 2019 and I will be claiming the tax relief in my 1029 tax return.

I am over 64 years now.

Can I still make contribution in 2020 and claim tax relief for 2020? My son, aged below 29, is still in university.

I claimed the tax relief annually when my child was still at university. Now that my child has graduated and started working since Jan 2019 (still below age 29),

am I still entitled to the RM8k tax relief for year 2019 if I still save RM8k for the year ?

Hi Admin,

Please help with following my case:

1. i had open and deposited RM5000 for SSPN i year 2014. Tax relief 5K done for year 2014. (Saving done).

2. In year 2015, closed this account (withdraw all $$). No tax relief regarding this for year 2015, 2016, 2017.

3. in year 2018 Dec, open new SSPN i account and deposited RM 6000. Tax relief 6K done for year 2018. (Saving done).

4. In year 2019 Dec, deposited RM8000 to the account. In this case, did I entitled for RM8000 tax relief?

Hi Admin,

I have 2 kids and both me and my wife opened 1 account each and tied to 1 kid each. Both of us have been claiming income tax for a few years separately. However, my wife stopped working and no longer have income, thus i am claiming income tax under myself (with my wife as no income). Can i still claim SSPN income tax deduction for her SSPN account as i continued to deposit into her SSPN account s well? If not, what would be the best approach – change the current SSPN account to my name? Appreciate your advise. Thanks.

Hi Admin,

I am choosing the Topaz package today when I register. If I am more capable in the future, can I upgrade to Zamrud or Nilam later?

Hi Admin,

How does the dividend return calculated for SSPN-i ?

eg i) Deposited lump sum on 1st Jan

ii) Deposited lump sum on 31st December

Would both scenario will receive the same amount of dividend ?

Thank you

Hi admin, a clearer explanation would be much appreciated, maybe with some examples of calculation to help us understand better otherwise it’s akin to not replying at all.

Hi, this might be a repeated question,

Just want get some clarification about the overseas studies.

If my child going to pursue her studies overseas after her secondary school, am i allowed to withdraw the whole amount saving?

If yes, is it a straight forward application or will there any justification needed ?

Thanks.

Hi. The yearly dividend payout computed on principal invested only or compounded (principal + dividend payouts, assuming no withdrawals were performed).

Hi. I have a few questions.

1. i have 2 daughters. I have open a SSPN account for my first daughter and plan to deposit 8k this year to get the tax reduction. If i want to enjoy the tax reduction next year, can i withdraw from my first daughter account and deposit it into my second daughter account? the net deposit is based on depositor or based on account? if is based on depositor, then i might want to open another account for my second daughter and deposit 4k each for each of them.

2. Assumed that we will get 4% dividend on year 2020, if i deposit 8k by 30th June 2020 and leave it until end of the year, do i get to enjoy 2% as i just deposited for half a year?

3. I read some of the comment above, may I know how some of the account managed to get up to 1k dividend payout in year 2018? they have total saving of 25k inside?

thanks

Hi Admin,

Thank you for your prompt reply.

Since SSPN-i is like an account with account number, if i make deposit, or my wife use her bank to make deposit into this account, who shall benefit from the tax deduction? when i register the SSPN-i account, i put my name as the depositor. i guess is me, but just to double confirm.

Thanks.

Hi Admin,

Can I ask in this example if i make a deposit of RM 5020 in 1 Jan 2020 but make a withdrawal of RM 5000 in 30 Dec 2020 ie only the balance of RM 20 remaning. Will i still earn a dividend next year in 2021 for the placement of 12 months or i get nothing because on 31 Dec 2020 there is only a rm 20 balance in my sspn account.

Thanks

Dear MyPF, Good job! I believe this article helps a lot of ppl and many quality answers from the Q&A.

I don’t have a SSPN-i account currently. Seeing the many benefits of SSPN-i account, I plan to open one for my child. I have a few enquiries that I hope you can help me with.

1. I see that PTPTN has a Jompay code. Can we make monthly contribution to SSPN-i account thru Jompay?

2. If yes, I plan to use my credit card when making payment to Jompay to get the credit card points. :-) (of course, I will need to settle my credit card bill in full to avoid the credit card interest)

3. Do you think using credit card to make deposit to SSPN-i account thru Jompay is considered an advanced cash withdrawal?

Thank you for your kind reply.

Hi MyPF team,

I have deposited into SSPNi on January 2020. If now i urgently need to withdraw from SSPNi.

Am I still will earning the pro-rated dividend around 4% in next early of the year when dividend declare ?

Hi

can a child-free retiree deposit into SSPN?

Dear MyPF, Retiree cannot open individual account? I thought there is a category for individual account. Thanks.

Kategori 3 (Akaun Individu):

Warganegara Malaysia yang berumur 29 tahun ke atas, perlu membuka akaun individu.

https://www.ptptn.gov.my/kategori-had-umur-sspn-i-side

Hi MyPF team,

Is it possible if I take this SSPN as an investment? Currently I’m 21 and single. As I see the return rate is quite high. So am I advise to invest in this?

Dear MyPF, Just want to share, there is now option for online withdrawal when you login to SSPN portal. No need to do it over the counter. And the money is in your bank account the next day. :-)

BTW, do you know if we can nominate different beneficiary for the takaful payout? Thanks.

Hi… Would like to know the interest count is base on the balance on 31 December ?

no mater which month i deposit money ?

example:

1. balance at Jan = RM12,000 , i deposit on Jun RM8,000, total = RM20,000

2. balance at Jan = RM12,000, i deposit on Dec RM8,000, total = RM20,000

Is it the interest for 4% are same = RM800 ?

Dear MyPF, may i just check if i deposit this in August this year – both husband and wife each gives to our kids RM8K (split into 2 children), say RM4k first child + RM4k second child – will both of us entitled for RM8K each (separate assessment)? in short, the relief is per assessment (individual) and not per Family/household? Thanks.

Sorry admin – i read through again your earlier comments and realized you’ve answered it much earlier back in 2018. i trust it’s still valid. By the way, can you also recommend other investment options as i find this to be relatively stable with 4% return each year. I dont have the time to do all the analysis for shares and i find it too risky. Appreciate if you can share some better return investment for my consideration. much appreciated

https://mypf.my/contact

Hi,

May I know how to get the dividen 4%? Since 2018 years, I have deposit RM30 every months, but I didnt notice 4% dividen every year.

Hi mypf,

1. Can i deposit RM10k into SSPN-i account although the tax relief is max to RM8k per year?

2. Will i get the 4% dividend from RM10k or RM8k only?

3. If I have 2 kids, can I deposit RM8k to each of their SSPN-i account? Will the 4% dividend issued separately to each of their account?

Thanks.

Hi mypf,

If I save RM8000 in January, but I withdraw it in November, then is there still interest count for this RM8000?

Thank you very much.

You are incorrect on statement:

“Parent/guardian tax relief of up to RM8,000 for SSPN-i per annum ONLY for parent/guardian of qualified child beneficiary.”

SSPN-i = RM8k tax relief

SSPN-i Plus = RM15k tax relief inclusive takaful

I don’t see any dividend paid to both my chidlren’s sspn-i account for 2019 or 2020, I have contributed RM8k total to both my children’s account and no withdrawal since I started in 2019. Am I missing something?

angie

Don’t mind sharing what’s the follow up on your non receiving dividend case?

Hi Admin,

Seeking your advice how can I change or amend the direct debit amount for my kids accounts

Appreciate if you can confirm as I have been reading different comments about withdrawal from SSPN-i :

1. Can I withdraw any amount at any time?

2. What is the process / condition for withdrawal?

3. Do I need to pay back the withdrawal amount?

Hi Admin, would like to enquire during the event when one of the SSPN account depositor demised (and the child is still under 18), how should the process of withdrawal should go about? The depositor currently having 2 joint accounts with his kids. Is the account still active and can the child can get full withdrawal upon reaching age 18?

Hi Admin, may I ask how do you calculate in your example table above by the 5th year with a yearly input of RM3,600 and with a total of RM20,279? Assuming it is 4.0% for each year. Thanks.

https://mypf.my/calculators/compounding-interest-calculator/

If I already deposit RM8000 this year and get the tax relief, can I still deposit RM8000 next year and still get the tax relief ?

Matching RM500 savings for RM500 invested in for children aged 7-12 (withdrawable only after age 18)”

Can you tell me what does this mean?

Hi Admin,

*Note: If both parents filing joint tax relief, total is for combined limit only.

What if both parents filing separate tax relief so we each entitled RM8000 tax deduction?

Hi

“Matching RM500 savings for RM500 invested in for children aged 7-12 (withdrawable only after age 18)”

My daughter is age 11 now, will her account entitle the above benefit till her age 12 only? Or till her age 18?

Thank you.

Hi there,

I want to check my SSPN status/account via online, but when I want to sign up, it will say “pendaftaran tidak berjaya” even though I have my SSPN account and other details. Is there any way I can sign up?

Thanks in advance.

Hi Sir, would like to check if there are any tax exemptions for individual (own higher education) contributions (SSPN-i or SSPN-i Plus? Thank you for your input.

Hi Sir,

I am now over 64 years old.

If we don’t withdraw the saving, do I still earn dividend for the saving after 64 years old?

Another question: I was told that by the time we reach 65 years old, we must close the account and there is no more dividend.

Thanks

Dear MyPF, Just to share, I recently found out that there is cut off date for SSPN saving. You need to deposit money before 5th of every month to be eligible for dividend for that month. If not, the deposit will only be eligible for dividend the following month.

BTW, I would like to seek your opinion on using SSPN as a cash management fund similar to Stashaway Simple. As mentioned in your article the average dividend is 3.84% which is better than 2.4% currently offered by Stashaway Simple. Do u think this method is workable? Any disadvantages u can see? Appreciate your kind thoughts on this. Thanks.

Hi MyPF, Thanks for the reply. I do not have any email record but this was informed to me by the contact center staff. Also, when I check my 2020 dividend, it seems to be the case. I tried withdraw money from SSPN-i using online, it takes just 2 days. :-)

Hi Max, if I understand correctly, any amount deposited during the month from 6th onwards would not be eligible for dividend for that month? Let said I deposit on the 7th May for RM1000, that RM1000 would not enjoy any dividend for the month of May as I deposit after 5th May? Cause this is important for deposit and withdrawal planning if this is the case.

HI Admin,

Thanks in advance for the help.

Would like to confirm, if i have to kids, so i need to open 2 SSPN i account? or under one account can add 2 Penerima Manfaat?

THANKS.

Hi My PF, can I just open a SSPN account and deposit an amount inside to earn the annual interest purpose? and also can I withdrawal any amount at anytime like a Bank Saving account?

Hi MyPF, I would like to know that is there any difference in the dividen if i deposit somewhere in May and if I deposit in Dec? Is the dividen be given regardless of how long the money has been deposited in the account? Thank you.

Hi, I have contributed in SSPN-i plus in Nilam package.

1) Can I change to Berlian?

2) If Yes, what would happen to the fund contributed earlier in Nilam package?

HI, if i have existing package under Nilam and i would like to add another account for Topaz, will the takaful benefit and tax relief double too?

What’s the downside of having sspn account?

I am 55 and plan to open a SSPN account, mainly as alternative for FD. I have a son who is 21 and he is pursuing a professional accounting qualification, full time. Can I put him down as beneficiary in order to get 8k tax incentive?

Hi, may I know how long it takes for the online account application to be activated?

Will there be two userID for online access if there are two kids’ accounts, or only one userID that is tagged to the depositor? Thanks.

I”ve 2 children and I’ve opened 2 SSPN accounts in their respective names. Can I deposit Rm4,000.00 each into the 2 accounts( totalling Rm8,000.00) and claim tax relief on the total sum of RM8,000.00?

THKS

Hi, firstly thanks for your time.

1. I understand I can deposit SSPN-i thru Jompay Maybank.

2. Withdraw: Can transfer from my SSPN-i account back to my Maybank account via online.