How would you deconstruct and reconstruct your portfolio? If it looks different before and after, it is time for you to consider rebalancing your investment portfolio.

Contents

Deconstruction

Imagine if your entire portfolio was immediately liquidated into cash. How would you reconstruct your portfolio with your now fully cash holdings?

A virtual exercise of hitting the reset button on all your investments may give you insights on what you should change (or not change) with your investment portfolio.

This exercise of deconstruction and reconstruction helps form the basis of portfolio rebalancing. How will you look at your current investment portfolio and make changes so it moves closer to your ideal portfolio?

Why Rebalance?

The key aim of portfolio rebalancing would be not to maximize returns per se, but to reduce the risks in your investment portfolio. A trade-off for slightly less potential returns will significantly lower your risks.

Rebalancing improves your risk-return ratio. Now go find that sweet spot!

When to Rebalance?

It does not make sense to make adjustments to your portfolio every time your portfolio allocation goes off by 1 or 2%. Nor does it make sense to look at your portfolio every day or every week and decide to make adjustments. The cost for doing that will be both financially and time-consuming.

The best balance for rebalancing would be to look at rebalancing every 6 or 12 months and to rebalance when any allocation is off by 5% or more.

Time and threshold approach: Rebalance at 5% and every 6 months (or longest 12 months)

Asset Alignment

Start with taking a high view of your overall investment portfolio and your personal investment plan goals. We will look at asset alignment in the following areas:-

High Risk Versus Low Risk Assets

The total percentage of high risk versus low risk assets would be the most basic, and yet most important form of alignment. High risk assets would include shares, unit trusts and property. Low risk assets would include fixed deposits, bonds, and endowments. This is as simple as starting out with age-based allocation of high:low risk assets and selling/buying assets to move you towards your desired allocation.

Asset Class Weightage

Within the high/low risk assets, you will also have your asset class weightage. This can be slightly more challenging with assets that are more fixed. For example, buying a single property can take up a much high percentage of your investment portfolio. Or for your EPF savings, you only have limited choices for withdrawing the funds before your retirement age.

Under-Performing Investments

You should have expectations for a particular investment’s performance that falls within an asset class. Are any of your investments under-performing expectations? Is it a temporary under-performance or dip which you don’t have to fret on, or is it symptomatic of a bigger and deeper underlying issue?

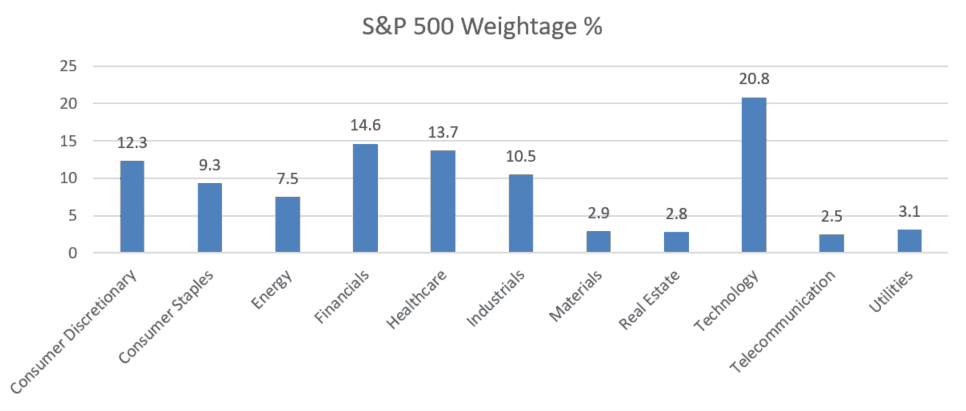

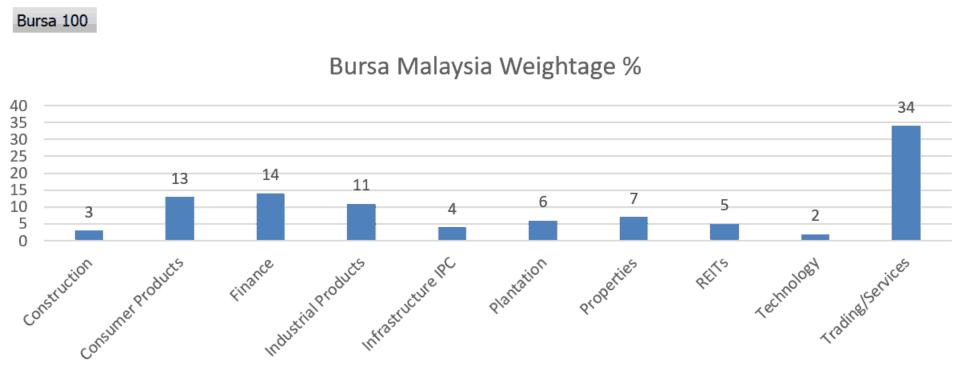

Sector Weightage

You will also want to group up your investments into sectors to see if you’re over/under-weighted in any specific sector(s).

Market/Country Weightage

Are you overweight in any country (usually your home country)? As your investment portfolio grows, you will want to make sure that a designated percentage of your investments are overseas in different markets as well thus reducing your country risks.

Mistakes to Avoid

Too much of any good thing is bad when taken to the extreme. Here are some common pitfalls and mistakes to hopefully avoid.

Don’t Overdo It

Balance is the key in rebalancing (pun not quite intended). Rebalancing too often and when unnecessary leads to unnecessary losses. This includes bleeding from a thousand cuts with increased fees and transaction costs.

Don’t Fall in Love

Emotions can quickly cloud an investors mind. With any investment, you should be able to simply explain why you invested, and in the next breath in what circumstances will you exit the investment. Don’t stubbornly hold on to something (or someone) who doesn’t love you back.

Don’t Be Kiasi

Imagining danger lurking at every possible time and location is no way to live. Otherwise you end up selling your winners too early and losing out on potential profits.

Kiasi [kiaⁿ-sí)] (hokkien) literally, afraid to die, but what it really means is being afraid to take risks or to be overly cautious.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment