The new Sales and Services Tax (SST) starts this September 1st. For Service tax, which services are fully exempted and which are going to cost you more?Will you need to pay more for your credit cards and electricity? What if you run a professional services or consultancy firm?

Contents

SST Introduction

This article focuses specifically on the Service Tax portion of the SST. For information on the Sales Tax portion, refer to this article instead.

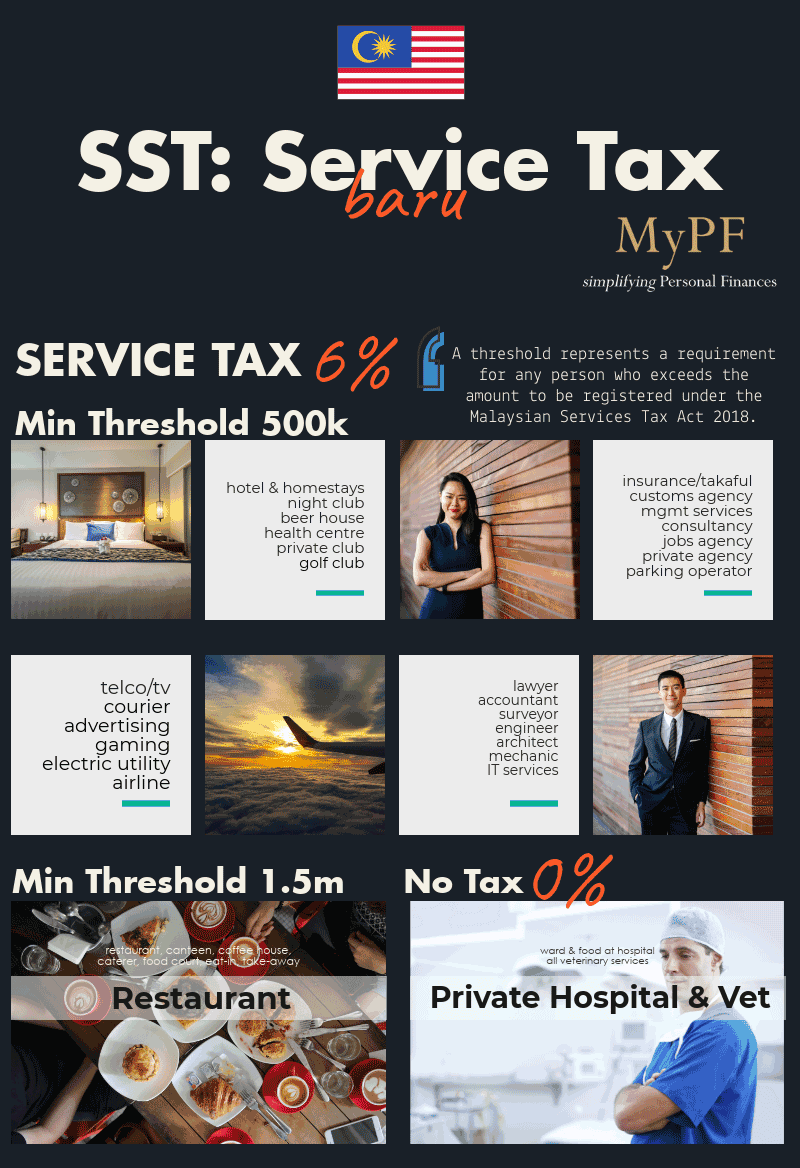

The new Malaysian government has moved to replace the unpopular Goods and Services Tax (GST) with a new version of Sales and Services Tax (SST). Service Tax (taxable services) is a consumption tax under the Service Tax Act 2018 which takes effect on Sep 1, 2018. There are around 30 categories for Service Tax with most having a minimum threshold of RM500,000. A threshold represents a requirement for any person who exceeds the amount to be registered under the Services Tax Act 2018. A threshold of 0 (i.e. Credit Cards) means all that use a credit card/charge card will be taxed). Below is a simple yet comprehensive guide to navigate the new Service Tax in Malaysia, with infographics and lists of items by category.

Service Tax Infographic

Service Tax by Industry

| Category | Service Provider | Taxable Services | Threshold (RM) |

|---|---|---|---|

| Hotel | Accommodation: hotel, inns, lodging house, service apartment, homestay, etc | All services including food, drinks & tobacco products | 500000 |

| Restaurant | Restaurant, bar, canteen, coffee house, caterer, food court operator, eat-in, take-away | All services including prepared/served food, drinks (alcoholic/non) & tobacco products | 1500000 |

| Night Club | Night club, dance hall, cabaret, public house, beer house, health or wellness centre, massage parlour, etc | All services including food, drinks & tobacco products | 500000 |

| Private Club | Private club | All services including food, drinks & tobacco products | 500000 |

| Gold Club | Golf club, driving range | All services including food, drinks & tobacco products | 500000 |

| Insurance | Insurer or takaful operator | General insurance/takaful B2B/B2C excluding medical insurance/takaful | 500000 |

| Telco/TV | Telecommunication & paid television service provider (exc provisions of services to another telco provider) | Telecommunication & related services; Paid TV broadcasting services | 500000 |

| Customs Agent | Customs agent | Services of clearing goods from customs control | 500000 |

| Lawyer | Advocates, solicitors & syariah lawyers | Legal services & other charges in connection to such services | 500000 |

| Accountant | Public accountant | Accounting, auditing, book keeping, consultancy or other professional services etc | 500000 |

| Surveyor | Surveyors including registered valuers, appraisers or estate agents | Surveying services including valuation, appraisal, estate agency or professional consultancy services etc | 500000 |

| Engineer | Professional engineer | Engineering consultancy or other professional services etc | 500000 |

| Architect | Architect | Architectural services including professional consultancy services etc | 500000 |

| Management Services | Management services (exc developer, JMB for strata title property, asset & fund managers) | Management services & other charges etc including project management or project coordination | 500000 |

| Consultancy | Consultancy services (exc R&D companies) | Professional consultancy services & other charges etc | 500000 |

| Employment Agency | Employment agency (exc secondment/supplying employees & employment outside Malaysia) | Employment services etc | 500000 |

| Private Agency | Private agency (exc protection situated outside Malaysia) | Provision of guards or the protection or security of person, property or business | 500000 |

| Parking Operator | Parking operator | Provision of parking spaces for motor vehicles where parking charges are imposed | 500000 |

| Mechanic | Operator of motor vehicle service or repair centre or provider of motor vehicle service or repair | Provision of servicing, engine repairs, tuning, changing, fixing of parts, wheel balancing, body repairs, etc | 500000 |

| Courier | Courier service operator | Courier delivery services for documents or parcels not exceeding 30 kilograms | 500000 |

| Hired Vehicle | Hire-and-drive passenger motor/passenger motor vehicles | Provision of hire-and-drive or hire-passenger motor vehicle services (with/without chauffeur) | 500000 |

| Advertising | Advertising (exc promotion outside Malaysia) | Provisions of all advertising services | 500000 |

| Credit Card | Credit card or charge card services provider (with/without annual subscription/fee) | Provision of credit card or charge card services through the issuance of a principal/supplementary card | 0 |

| Gaming | Betting and gaming provider (bettings, sweepstakes, lotteries, gaming machines or games of chance) | Betting & gaming services, conducting tournaments, card/any game by casino operator | 500000 |

| Electric Utility | Transmission and distribution of electricity provider | Provision of electricity to any domestic consumer excluding first 600 kWh (min 28 days/billing cycle) | 500000 |

| Airline | Airline operator (excluding Rural Air Services Agreement transport route) | Domestic passenger air transport service and all services in connection with such services in Malaysia | 500000 |

| IT Services | Information Technology (IT) services provider (exc sales of goods, services outside Malaysia) | All types of IT services | 500000 |

Non Taxable

- Private Hospital: Ward and food charges only in private hospital.

- Veterinary: All veterinary services.

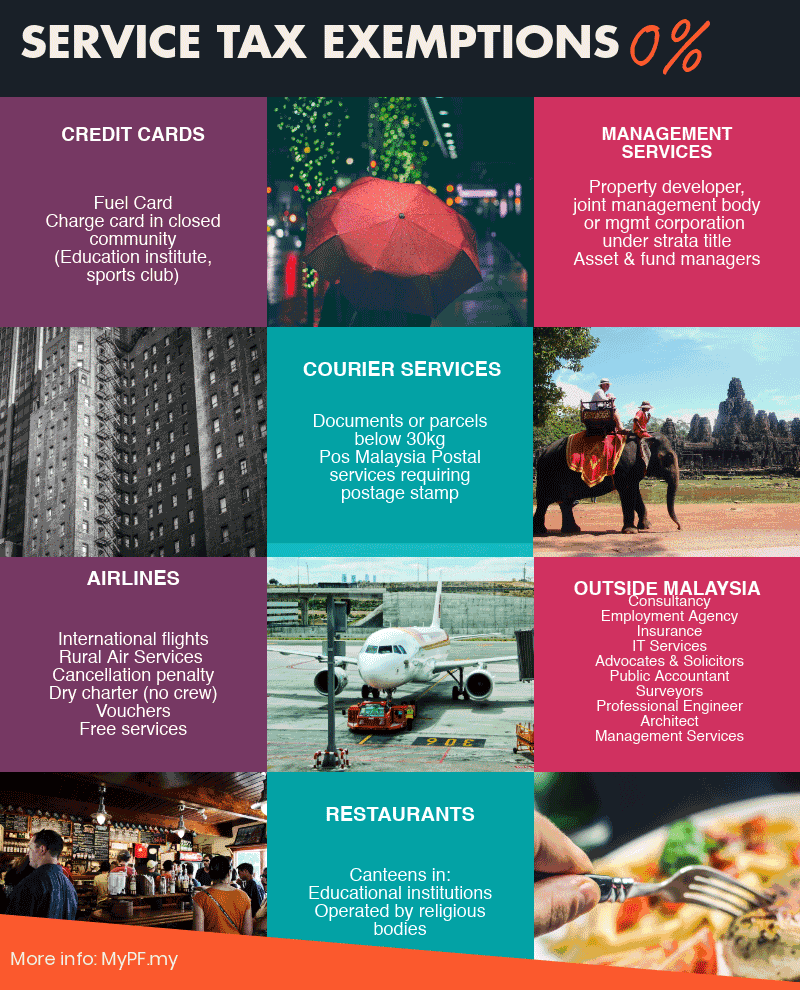

Exemptions

- Restaurant exemption: Canteens in educational institution or operated by religious institution/body.

- Insurance exemption: Insuring or takaful coverage of risks relating to the transport of passengers or goods outside Malaysia; Insuring or takaful coverage of risks incurred on granting credit relating to the export of goods, services or investments outside Malaysia; Insurance contract or takaful certificate to cover risks outside Malaysia.

- Telco/TV exemption: Provisions of services to another telco provider.

- Management Services exemption: Excluding management services provided by the developer, joint management body or management corporation to the owners of a building held under a strata title; asset and fund managers.

- Consultancy exemption: Consultancy services by R&D companies; or relating to medical and surgical treatment provided by private clinics or specialist clinics; or consultancy services in connection with goods or land outside Malaysia or where the subject matter relates to a country outside Malaysia.

- Employment Agency exemption: Secondment of employees or supplying employees to work for another person for a period of time; or employment outside Malaysia.

- Courier exemption: Courier delivery services for documents or parcels below 30kg each including services for documents or parcels:

from a place outside Malaysia to a place outside Malaysia; from Malaysia to outside; from outside to Malaysia. - Credit Card exemption: Fuel card, charge card in closed community (e.g. education institution/sports club).

- Airlines exemption: Air transport route as specified under Rural Air Services Agreement.

- IT Services exemption: Sale of goods in connection with the provision of IT services; IT services in connection with goods or land outside Malaysia or where the subject matter relates to a country outside Malaysia.

- Outside Malaysia / Government / Statutory Body exemption: The following categories are exempted where said services if provided in connection with goods or land outside Malaysia or where the subject matter relates to a country outside Malaysia; or any statutory fees paid to the government or statutory body.

- Advocates and solicitors

- Public accountant

- Surveyors

- Professional engineer

- Architect

- Management Services

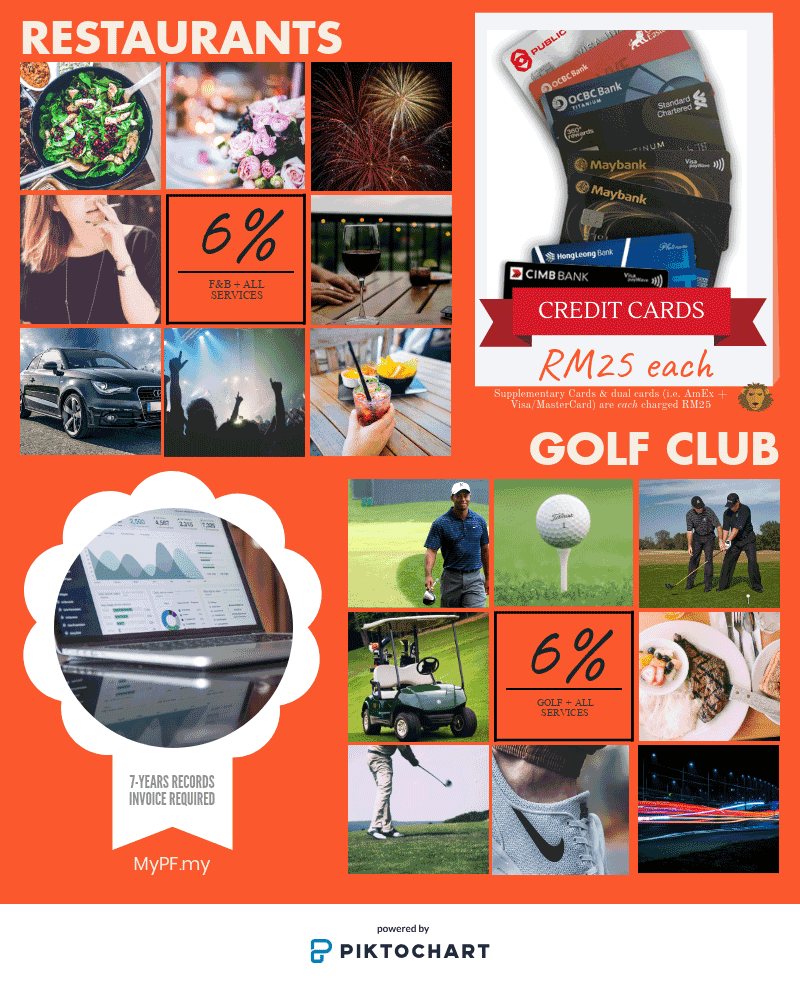

Restaurant – Food & Beverages

Service tax: 6%

Threshold: 1,500,000

Know your restaurants

- Restaurant: A place where people acquire services for meals that are prepared, cooked and served on premises or takeaway. The services that provided may include taking orders, preparing or retrieving items when ready, filling cups with beverages, and accepting customers’ payments.

- Bar: A place where alcoholic drinks are served. This includes pub, bistro, etc.

- Cafeteria: A restaurant in which customers serve themselves (self service) from a counter and pay before eating. This includes coffee house, canteen, cafe, etc.

- Catering: Business of providing F&B services at any event or venue or to another business or person.

- Drive Thru: This service may include drive through service where they allows customers to purchase products without leaving their cars/vehicles.

- Food Truck: A vehicle equipped to cook and sell F&B that moves from place to place. The food may be prepared from scratch and pre-packaged food.

- Retail Outlet/ Snack Bar/ Kiosk: A small store, informal restaurant or kiosk that sells and prepare smaller quantities of product for dining in or takeaway ie. light meals or snacks.

- Hawkers/ Push-Cart: A vendor of merchandise that can be easily transported that sells a variety of food. The stall may be moveable or immoveable. The food may be prepared from scratch and pre-packaged food.

- Food Court: A food court is generally a common area within a facility that is set apart for food concessions. It may consist of a number of vendors at food stalls or service counters.

- Canteen: A restaurant provided by an organisation such as in school for its students, factory for its staff, etc.

Service tax levied on

- All services including prepared or served food or drinks

- Sale of tobacco products

- Sale of alcoholic and non-alcoholic beverages

- Parking Facility (excluding free parking)

- Events/ Conferences/ Meetings/ Seminar Packages

- Celebration Packages

- Space for rental situated in the F&B operator premise

- Hire of a hall for any events

- Hire of a sports, games or recreational room

- Car jockey services

Not subject to service tax

- Canteen located in an educational institution

- Canteen operated by a religious institution or body

Night Clubs etc

Know your clubs

- Night club: Entertainment venue and bar inclusion of stage for live music, dance floor areas, and DJ booth.

- Dance hall: Hall for dancing

- Cabaret: Theatrical entertainment featuring music, song, dance, recitation, or drama.

- Public house: Place permitted to sell and service intoxicating liquors and beers.

- Beer house: Place to sell and serve beers only.

- Health center/massage parlor: Health services and massage services are provided which is approved by the appropriate local authorities.

Private Club

Service tax levied on provision of

- Sports or recreational services including the entitlement to use such services by club members for which membership subscription fees are charged other than golf.

- Sale of food, drinks or tobacco products.

- Services in the form of corkage, towel charge or cover charge.

- Health services, which are normally provided by health centers.

- Massage services excluding massage services provided in barber shops, hairdressing salons or beauty salons.

- Premises for meetings or for promotion of cultural or fashion shows.

- Parking spaces for motor vehicles where parking charges are imposed.

- Rooms for lodging or sleeping accommodation.

- Golf course, golf driving range or services related to golf or golf driving range

Golf Club & Driving Range

Service tax levied on

- Green/ season pass

- Caddy

- Rental of golf buggy/ turf mate

- Rental of golf equipment;

- Guest

- Complimentary play

- Coaching

- Absence

- Competition entrance

- Tournament

- Lighting for night golfing

- Night golfing

- Practice range balls or driving range balls

- Rental of golf shoes;

- Subscription fees.

Telco: Telecommunication Services

Service tax levied on basic telecommunications which are the transmission of voice or data from sender to receiver.

- Fixed network voice telephone

- Analog/digital cellular/mobile telephone

- Satellite Telecommunication

- Internet and other digital data transmission

- Network component rental, sales and service

- Network access and network facilities

- International telecommunication basic infrastructure

- Wireless paging

- Resale of basic telecommunication

Service tax levied on value-added services, for which Telco adds a value to the telecommunication services.

- Fixed telephone network value added services

- Mobile network value added services

- Satellite network value added services

- Internet value added services

- Other data transmission network value added services

TV: Paid Television Broadcasting Services (PTBS)

Service tax: 6%

Service tax levied on

- Supply of TV package to customers

- Supply of Satellite TV Box / Set-top box (STB)

- Change/Upgrade of package

- Installation/re-installation (reactivation) fee charged to the recipient

- Repair charges

Customs Agent Services

Service tax: 6%

Provision for clearing of goods from customs control by customs agent which is a prescribed service, the value of the taxable service for the charges of service tax is the actual price of services charge to his clients at point of services rendered.

Courier Services

Service tax: 6%

Service tax levied on

- Service provider licenced under Section 10, PSA 2012

- Domestic courier service

- Service provider registered under Service Tax Act 2018 (STA 2018)

Not subject to service tax

- Postal services by Pos Malaysia Berhad by way of sending letters that require postage stamp including bulk mailing and franking machine

Hired Vehicles (Hire-and-Drive)

Service tax: 6%

Service tax levied on

- Vehicle rental fee (time / mileage)

- Driver service fee (vehicle for hire)

- Drop off / delivery charges (charges imposed on returning rental cars elsewhere from where they were taken.)

- Child-seat or booster-seat rental.

- Fuel surcharge

- Insurance charged by the operator

- etc

Not subject to service tax

- Summons

- Car wash

Credit Cards

Service tax: RM25 per card

Service tax imposed on date of issuance or renewal of credit/charge card OR every 12 months after the date the card is issued or renewed. Service tax is inclusive for co-branded cards. Service tax excluded for debit card, fuel card, charge card in private community, loyalty card, and electronic money (e-money/e-wallet). If an old card is reused/reinstated, service tax shall be imposed on the date the new card is issued. Service tax is imposed even if used in (duty-free zones) likes Langkawi, Labuan, Tioman, Setulang Laut or Pengkalan Kubor.

Airlines (Domestic Flight)

Service tax levied on

- From a place to and within Malaysia including between Sabah and Sarawak

- Ancillary services: excess baggage, seat selection, lounge access, meals on board, fuel surcharge, basinet, wifi-on-board, class upgrade, insurance, other charges/fees, etc

- Wet charter (with crew)

- Private jet

Not subject to service tax

- International flights inbound/outbound

- Rural Air Services (RAS): operated via MASwings with 49 RAS routes

- Sales of goods and services (except food & beverage)

- Penalty for cancellation

- Dry charter (without crew)

- Freight transportation (re: Courier Services)

- Intragroup Shared Services

- Vouchers (compensation by airline)

- Loyalty proramme

- Free services

More Info

- SST: Simplified Malaysian Sales Tax Guide

- GST vs SST Guide

- Guide on Credit Card and Charge Card (customs.gov.my)

{kind=link}

{kind=link}

Can I clarify that pertaining the ‘Display price must be in nett as per Single Pricing Policy with clause on inclusion of taxes’? Shall all the pricing comes with nett selling price which include SST% for everything which taxable?

Hi! Does the Service Tax applies for training providers and HR advisory companies?

Hi there, my company provides training as a training provider to company. Would this fall under management services? Thank you so much for your great advice

Hi, is education exempted from service tax? For example, kindergarten business.

Thanks!

Hi! Is Service Tax applicable to Employment Service for LMW status company?

any guidedance for itemise billing for event management services

Hi! Is Service Tax applicable to Management Service for Real Estate Investment Trusts (REITs) status company?

Hi there, is real estate agents/agencies subject to SST?

Is there any extension allowed when changing from GST to SST for a company? For example, can you still transact in GST if you are in the process of switching to SST?

Do the followings subjected to sst:

1. Rental of domestic homes.

2. Rental of business/commercial buildings

3. Rental of cabins

https://mysst.customs.gov.my/assets/document/1.%20Guide%20on%20Accommodation_~1.pdf

Hi, is Sales IT Goods retailer exempted from service tax? Example selling laptop and computer shop without service.

Service contract signed before May 2018 indicate client to pay GST. Client now refuses to pay SST because contract specifically states GST. What can be done, or is there guideline for automatic change from GST to SST in existing contract clause?

Hi

Would like to ask is IT services like Webpage layout and design, Webpage coding, Copywriting subject to service tax?

I received a swift transfer from india for a work carried out in malaysia for insurance survey purpose. Is the remittance amounting to USD 1491 (MYR 6232) taxable i.e 6%SST imposed ?

If we sale of company asset such as we dispose company’s car, do we need to charge SST upon sale of those assets?

Hi

Our full wedding package among others inclusive hall rental for the wedding venue. Should we include hall rental charge to the customer to calculate the threshold of 1.5mil?. Thanks.

Hi,

For wedding package signed during GST period (March 2018, actual day of wedding on Jan 2019), partial payment (RM 20,000 out of RM30,000) made during Tax free period (0% GST and SST)

How should the SST of the Hotel be calculated? Will it only imposed to the balance of RM10,000? Or it will crawl back and charge the full amount of RM30,000?

Cheers

Hi I need clarify on your statement below and General Guide on disbursement. The exemption might be conflict each other. Does I need to comply with the disbursement clause ?

Malaysia / Government / Statutory Body exemption: The following categories are exempted where said services if provided in connection with goods or land outside Malaysia or where the subject matter relates to a country outside Malaysia; or any statutory fees paid to the government or statutory body

Thanks

HI I refer to the General Guide on disbursement stated as below

Payment to third party or on behalf of the principal will be treated as disbursement if the registered person fulfils all the following criteria:

(i) Incur expenses on behalf of the client;

(ii) The client is the recipient of the services (invoice is in the client’s name);

(iii) The payment is authorised by the client;

(iv) The client knew that the services is made by a third party;

(v) The exact amount is claimed from the client and has no right to alter or add on the value of the services;

(vi) The payment is clearly an additional to the services made to the client.

In the exemption given to any statutory fees paid to the government or statutory body, all the receipt or invoice issue by the statutory body its not under the client name as per item no. (ii)

My issue which to follow ?

Thanks

Hi sir

May I know if car dealer earns agent fees from agents, is the agent fees billed to agents subject to 6% service tax?

Can i know that imported service tax, online service from oversea subscription fee need to subject to 6% service tax start from Jan 2019?

Company borrow staff to other company. The staff monthly salary is RM2,000 and back charge to other company with salary RM2,000.

Kindly advise whether the monthly salary RM2,000 back charge to other company is subject to service tax?

Hello

Can I know whether provision of sauna services for customers and selling sauna units are subject to sst? If our company voluntarily register for sst, does this mean we hv to start charging sst from day one of services even if we hv not exceeded 500k threshold?

Hi, i m in real estate agency, may i know sub sales (second hand)subject service tax or not?

May I know purchase software license from oversea then sell to reseller, retailer need to declare Imported Taxable Service?

Does sponsorship subject to 6% SST?

My customer is a Machinery Consultant who provide end-to-end solutions in circuit, layout and network design from drafting through to manufacturing stages. We are one of the sub-contractor who provide steel fabrication, installation, service & repair. For steel fabrication service, my client has apply Exemption C5 for certain items. But for installation, service & repair, do we need to charge Service Tax 6% if more than 500k turnover?

If a Malaysian individual provides contract management consultancy services to a Vietnamese registered company in Vietnam, and where he will be paid in US dollar by the Vietnamese company for his services, is his income subject to a 6% Services Tax?

Hi, my company is exempted from register SST (manufacturer of jewellery), however we also use our own company to register as custom agent for custom purpose. In this case we still have to register for SST?

Hi, recently I’ve receive notice of the 6%sst for my music lesson will be imposed. Why consumer have to pY for the sst for enrichment lesson. Isnt This is part of education? This is not sales and service.

Hi, My company lease out security bag especially to money changers and gold supplier. I guess its come under equipment leasing. Is this subject to SST? Thank you,

Hi, My College offer diploma program and at the same time conduct short courses program. Does my college have to charge SST to our students?

Hi. Can I get sources of your articles, especially pertaining to the Credit Card section above?

customs.gov.my

Hi there,

I need your input on the following situation, to confirm whether my understanding is correct or not.

Subject: Digital Services, Imported Taxable Services & Withholding tax (WHT)

Status: Reseller of Cloud Services B2B & a registered SST

Situation: Double tax situation if selling via a reseller. If consumer buy direct from the website, a consumer only self-account on WHT & Imported Services (in 1/1/2020, it will be WHT + Digital Tax)

Current practice:

– Cost

1] Cost of Services (Cloud)

2] WHT 10% (foreign provider insist cost of WHT is on reseller)

3] Imported Service 6%

– Sell

* Above Cost [1, 2 & 3] + Fixed Margin = New Selling Price + 6% SST

Is my current tax calculation above correct?

Based on the above calculation, the cumulative tax is 22% (10% + 6% + 6%), if the end-user buys from a reseller. However, let say if the end-user buys directly from the website on 1/1/2020, the cumulative tax is 16% (10% + 6%).

As a reseller, I am expensive by an additional 6% because of imported taxable services.

In your opinion, is there any way that I can get an exemption on imported taxable services because I am already collecting 6% SST from the end-user?

My company is providing accounting service and we do collect membership fee, is the membership fee subject to SST?

Hi, we recently open a restaurant and bar ( less than one month), the threshold is RM1.5m for hospitality when it comes to SST registration, hence, in my situation, does my restaurant and bar still subject to SST? or the SST is based on the actual sales to determine the threshold and not forecast sales? thanks

Hi, we are consultant. we charge SST to client let say RM4482 and the same job we sub to another Consultant . the sub consultant charges SST RM 2550 to us. whether the SST can be contra . RM4482 less RM2550 = RM1932 only RM1932 pay to customs?

We are selling/export software as a services product that was developed in Malaysia and open for global market, thus we display our selling price in our website in US$, do we need to apply SST to those buyers from Malaysia?

Hi, may I know whether the rental income from factory rental subject to SST?

Hi, if a related company provide marketing services to another related company within the same holding Group. Do this service to related company subject to SST?

Hi, may i know rental of laptop is subject to SST?

hi is florist subjected to sst?

Hi, is SST for consumer an expense? For example; telephone charges, is the expense less SST or total bill?

Hi, my business service is rental of the credit card terminals to merchants (customers). The monthly rental includes provision of thermal paper rolls, mobile SIM card and 24/7 maintenance service. Please advise if I would have to charge SST on my customers – if yes, would the threshold be RM500k and which industry would this fall under?

Thank you

Hi,

For new Advertising company, we do not know if the yearly threshold will reach 500k given the MCO circumstances as well.

1. So do we hold on from registering first, and after it hits RM500k in the year only we register?

2. If it hits RM500k, the projects before 500k will not be charged SST?

How do we go about it?

Hi, Fatin here. May I know is nursing home/old folks home (pusat jagaan warga tua) subject to SST? This is Sdn Bhd company and a tax payer. Thank you :)

Hi, i wonder is a jewellry retail shop is subject to service tax? webpage online selling jewellery subject to service tax? Online selling coffee bean and coffee powder subject to sst?

HI,

FIXED DEPOSIT INTEREST INCOME SUBJECT TO SST?

how about for law firm FD interest subject to sst?

Thanks

Hi, does a music school need to register for SST?

IS FIXED DEPOSIT INTEREST EARNED SUBJECT TO SST FOR COMPANY AS INCOME?

Hi! Do we need to charge SST on the sub-consultant service to client?

Hi. Are real estate agent professional fees (aka commission) by for the sale of property subjected to SST?