How does peer-to-peer property crowdfunding like FundMyHome work? Is it beneficial for a buyer? Are there risks?

Contents

Property Crowdfunding

Malaysia’s Budget 2019 announced the launch of Peer-to-Peer (P2P) property crowdfunding. Home buyers need to pay 20% upfront of the purchase price while the other 80% is paid by investors. The home buyer can stay/rent out the property without having to make any additional payments for the next 5 years. After 5 years, the home buyer decides whether to keep the property or sell it.

Keep

Home buyer will need to buy up the entire property via a home loan or “refinancing” with FundMyHome after 5 years.

Sell

Home buyer will share in the profits (or losses) of the property based on market price versus original purchase price (5 years prior).

How it legally works

The developer grants an option to buyer contributor to purchase property with right to nominate buyer upon exercise of option. The buyer is the legal and beneficial owner of the property but until the property is fully paid for, the buyer’s rights as owner will be subject to the rights of institutions as assignees/chargee of the property.

Property Crowdfunding Framework

Property crowdfunding framework by SC details it as:

a form of fundraising that envisages a homebuyer obtaining funds to pay for the purchase price of a property by way of investments from a relatively large number of investors, through an online platform responsible for publicising and facilitating such transactions.

Buyer must fulfil requirements (see below), is only eligible for completed property and the buyer must stay in the property (but can rent out rooms).

FundMyHome

FundMyHome.com is the 1st property crowdfunding site in Malaysia and is developed by EdgeProp Sdn Bhd.

- High-rise & landed residential properties

- Developer partners: EcoWorld, UEM Sunrise, PKNS, MahSing, IJMLand, PNB, Sunway, IOI, Trinity Group

- Institution partners: Maybank, CIMB

Eligibility

- Malaysian

- Age 21 years above

- First time home buyer (never owned property solely or jointly)

- Non-bankrupt

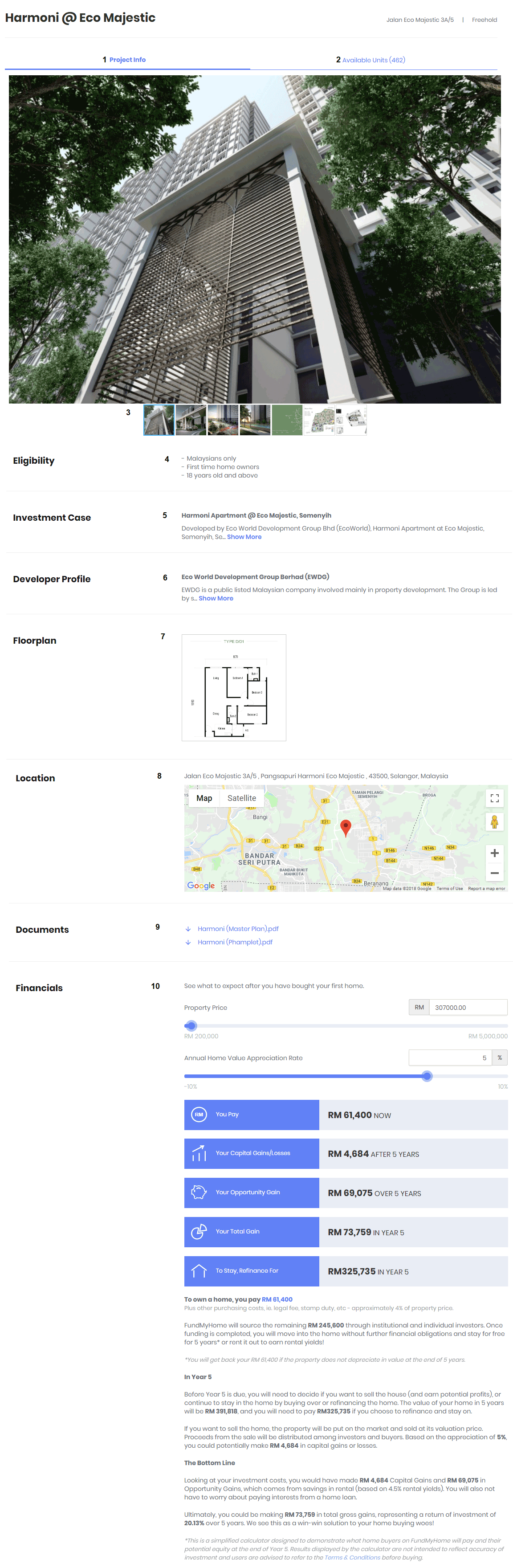

Info Available on Free Registration

- Project info

- Available units info: including market price, property price, pay to own, car park, unit type, unit details, size, layout

- Project photos

- Eligibility criteria

- Investment case: why you should buy

- Developer profile

- Floor Plan

- Location map

- Brochures

- Financial projection calculator

(Source: fundmyhome.com)

Buying Process

- Register for account online at FundMyHome.com

- Provide personal info

- Verify identity

- Agree to term of use: including providing consent for FundMyHome to obtain your Personal Credit Information for Credit Reporting Agencies Act 2010 & PDPA Act 2010 upon making a transaction to buy.

- View and select property (min RM200,000 and max RM500,000 in 1st phase)

- Pay 2% booking fee (first-come-first-served basis) which is non-refundable if you withdraw with no cooling-off period

- Pay balance of purchase price & all fees within 14 days from date fully funded (if not fully funded within 30 days monies refunded with no interest)

- Other purchasing costs (legal fee, stamp duty, etc): est 4% property price

- Legal conveyancing process: singing SPA, stamping, etc (~2-3 weeks)

- Vacant possession at discretion of developer

Property Owned

- Buyer can now stay or rent out the property (within 5 years from purchase date)

- Buyer is responsible for all home ownership fees including management fees, quit rent, assessments, repairs and maintenance

Exit Process

- Note: The property CANNOT be sold before the 5-year commitment period

- At the 4.5 year mark, an independent valuer conducts valuation of house with cost borne by buyer

- Buyer decides to stay

- “Refinancing” via FundMyHome by topping up funds to 20% of new valuation

- Buy the remaining 80% share held by institutions based on valuation price by using own funds or via bank borrowings

- Buyer decides to sell

- Property advertised for sale on open market for at least 3 months at valuation price

- Buyer pays for all selling 3rd party costs such as agent fees

- Buyer is subject to Real Property Gains Tax (which with Budget 2019 is at 5% after 5th year)

- Buyer is required to pay 5% rental yield if does not vacate property after 5th year

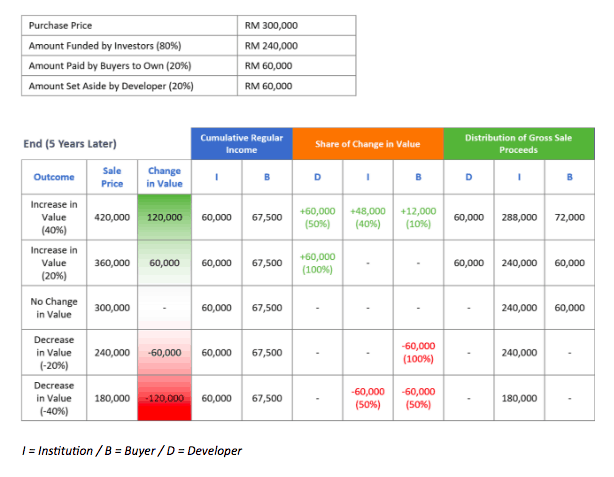

- Sales proceeds disbursement by priority

- Institutions’ capital

- Buyer’s capital

- 20% of original purchase price paid to developer (if property appreciates by more than 20% upon exit)

- Balance shared proportionately by investor:buyer 80:20

(Source: fundmyhome.com)

Pros & Cons

Buyer

Pros

- Pay only 20% of purchase price & not required to pay rent/loan to stay/rent out property

- Able to buy a property if unable to qualify for conventional housing loan from financial institutions

- Buyers not personally liable in the event sale proceeds from foreclosure or normal sale insufficient to repay institutions

Cons

- If property price goes down by up to 20%, the buyer loses the initial capital of up to 20% (capital not returned)

- Basically all property maintenance, buying, selling & other fees including RPGT are borne by buyer

- Selling the property may take time (~3-6 months) & may not be able to find a ready buyer

Institutions

Pros

- Investment exposure to Malaysian residential market for a medium-long term without having to manage individual homes/handle monthly repayments

- Guaranteed returns 5% p.a.

- Potential capital gains

Cons

- If property price goes down by more than 20%, the institution risks lost of capital

Developer

Pros

- Developer has wider market to sell property even for those who fail to qualify for conventional housing loans

- Developer profits additional 20% of original price if property appreciates by more than 20%

Cons

- Developer needs to set aside 20% of property price in trust account & is not paid to developer upfront.

Government

Pros

- Government helps meet rakyat’s needs of property ownership using technology

Cons

- Risk of failure of initiative is project fails to be successful

Projections

- Property purchase price: RM300,000

- PAY 20% upfront purchase price: RM60,000

- PAY 4% legal/fees/purchase costs: RM12,000

- SAVE Rental savings/rental income at 4.5% rental yield: RM67,500

- Overall savings/loss: -RM4,500

Exit at 3% p.a. appreciation (after 5 years)

- Property market valuation: RM347,700

- GAIN Capital appreciation: RM0

- LESS 2% legal/fees/exit costs: -RM6,900

- Overall savings/loss: -RM6,900

- Total savings/loss: -RM11,400

Exit at 5% p.a. appreciation (after 5 years)

- Property market valuation: RM382,800

- GAIN Capital appreciation: RM4,500

- LESS 2% legal/fees/exit costs: -RM7,600

- Overall savings/loss: -RM3,100

- Total savings/loss: -RM7,600

Exit at 7% p.a. appreciation (after 5 years)

- Property market valuation: RM420,700

- GAIN Capital appreciation: RM12,100

- LESS 2% legal/fees/exit costs: -RM8,400

- Overall savings/loss: RM3,700

- Total savings/loss: RM800

Overall

Property P2P crowdfunding can be a good way to buy a property if you are unable/do not want to take up a conventional housing loan. Property developer participation appears positive including developers with strong backgrounds. As a home buyer, you can view what units are available, and are provided information on the project. However, potential gains as a buyer are limited especially after factoring in all the fees/costs that you will need to bear unless the property appreciation is significantly above historical average returns and/or you are able to rent out the property at good price (above the projected 4.5% p.a. yield).

Overall, the key benefits for buyers is more opportunities for first time home buyers to own property, and the flexibility to decide whether selling off or fully purchasing the property after five years BUT as a buyer one should have not overly high expectations for investment returns.

FAQ

Q: What is the difference between Fully Funded VS Funding in Progress

A: Fully Funded properties are ready to be purchased with 80% funding already obtained. Funding in Progress properties are pending full funding. If you reserve a unit that is not fully funded, there is a 30 day period to fully fund the property. If it’s not fully funded yet, there’s a 30 day period to fully fund else your deposit is fully refunded (with no interest).

Q: How can I invest as an investor instead of home buyer?

A: At time of article publication, it appears investors are only open for institutional investors. You can only participate as a home buyer.

Q: Can the purchase be a joint property purchase?

A: Yea as long as both parties are eligible.

Q: Can the buyer renovate the property?

Yes at buyer’s own cost.

Q: How is property P2P crowdfunding different from Rent to Own?

A: Property P2P crowdfunding does appear to have similarities to rent-to-own schemes (RTO) with a key difference being you pay for the 20% upfront instead of on a monthly basis. You also get access to a wider range of properties and developments. The mechanism for profit (or loss) sharing is different as well compared to RTO.

More info

- FAQ on Property Crowdfunding Framework (sc.com.my)

- FundMyHome Terms and Conditions (fundmyhome.com)

- Rent to Own (RTO): Maybank HouzKEY Review

{kind=link}

{kind=link}

{kind=link}

can i know the procedure that will be required in the sale and purchase in detail?

Does it mean that the property is charged to the financial institute until five years later when the purchaser decides to buy or sell the property?

May I know if I were to use a crowdfunding platform to finance my home, upon the payment of 90% (or is it 80%?), under whose name will the MOT be executed?

Hi, i just want to know further regarding the refinancing if you choose to stay after the period of 5 years. Is the refinance price is the price that we have to pay if we choose to stay? Does it means that we just pay the original price of the house plus the appreciation value? Can you elaborate further when we choose to stay after the period of 5 years ended. thank you!