Should you invest in Unit Trusts? Why is engaging with a unit trust adviser or licensed financial planner a wise move? The original version of this article by Royce Tan was published on The Star Online.

Contents

EPF Withdrawals for Unit Trusts Investing

Many people would have contemplated investing in unit trusts by using part of their savings in the Employees Provident Fund (EPF).

For those who have reached retirement age, meanwhile, the question is whether to withdraw their savings and park them in unit trusts.

There are funds that have trumped the EPF’s performance, but how many of them fall into that category or have a portfolio as diversified as the EPF?

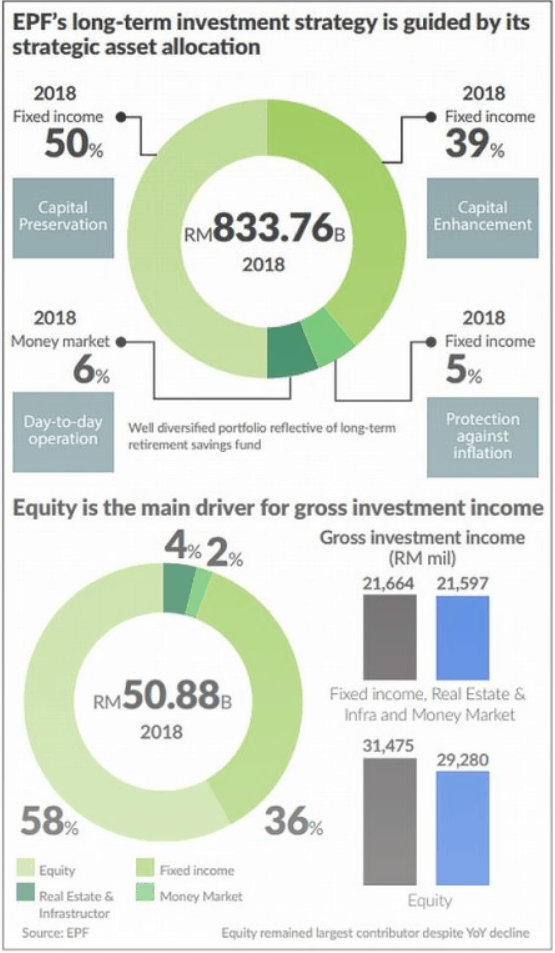

The provident fund declared a stellar 6.15% dividend amid another year of market volatility in 2018. The FBM KLCI has been down for four of the past five years.

The dividend declared by the EPF beats close to 90% or slightly more than 1,000 unit trust funds in the country.

Image source: TheStar Online

Should You Withdraw Your Savings to Invest in Unit Trusts?

So, this begs the question again, would it be worthwhile for those eligible to withdraw their savings to invest in unit trusts?

Only if you know what you’re doing, have a fund you trust or if you have the holding power. Unit trusts are a good product for long-term investment, and then for retirement purposes.

If you can keep it for the long-term, you can practice dollar-cost averaging (DCA). You can never buy or invest at the lowest point but when you average this out, you will get the lower average price. Investments in unit trusts carry a certain risk element and investors might lose their capital portion.

Why the MIS Option for Investing in Unit Trusts?

But if unit trusts are risky and with the EPF issuing dividends exceeding expectations, why is there a need to allow members the option of investing in unit trusts?

One rationale is that the funds in the EPF are too large and with their incremental nature, it cannot manage them entirely on its own.

The redemption rate is much lower than the subscription rate. That’s why the EPF also has foreign fund managers.

The Members Investment Scheme (MIS) is to allow EPF members to have options, and to lessen the burden of the EPF because the larger the size of a fund, the more complications it faces.

Unless investors can find a fund performing better than the EPF or fixed deposits, it is better to retain the funds in the provident fund. If you’re only fetching 5%, you might as well leave it in the EPF. The track record of a fund can only give you some kind of interpretation, not evidence of its future performance.

No One Size Fits All Solution, Work with a Financial Advisor

Former investment and corporate strategy director Pankaj C. Kumar says the EPF is the country’s best fund manager that has consistently performed for all.

“For investors thinking of taking out money to do their own investments or in unit trusts, perhaps it’s best to leave it to the EPF, as it is exposing investments to equities, fixed income, real estate and private equity while being geographically diversified at the same time,”

Stephen Yong, the founder of personal finance firm MyPF, says:

“The EPF’s performance in 2018 has been commendable, consistent and above most investors’ expectations. This is amid the backdrop of an overall poor equity market performance globally and in Malaysia. Most unit trusts’ one-year performance for 2018 with equity exposure saw poor or negative returns and high volatility.”

Meanwhile Rajen Devadason, a licensed financial planner with Manulife Asset Management Services, says the question of whether EPF members should use their contributions to invest in unit trusts when allowed is one that hinges on the EPF contributors’ personal risk appetite.

“Those who prefer certainty and are uncomfortable with investment market volatility should retain all their money in EPF account one until retirement. But those who wish to invest externally should do so carefully and wisely, heeding sound asset allocation in high-quality investments approved by the EPF and long-term diversification using DCA strategies, to try to generate long-run returns.

Each person is different and should only take action that is appropriate to his or her internal makeup and circumstances. As such, working with a unit trust adviser or licensed financial planner is wise. Even those who decide against using their EPF money to invest in unit trusts are likely to benefit from using a portion of their monthly discretionary cash flow from their salaries to invest in cash-funded (as opposed to EPF-funded) portfolios. But this requires disciplined budgeting and a lifetime adherence to delayed gratification that helps people spend less than they make, and to save and invest the difference for a long time. It is the only way to ensure their time in retirement is marked by comfort and sufficient financial resources.

Signup for a MyPF membership and get connected to a licensed financial planner.

You May Also Like

- How to Select a Financial Planner in Malaysia

- How To Craft Your Personal Financial Plan With Your Financial Advisor

- Knowing When to Hire a Personal Financial Advisor

- How to Become a Financial Advisor

- How does your Personal Finances Advisor Get Paid?

{kind=link}

{kind=link}

Leave A Comment