The markets are more concerned about the uncertainty of the trade deals, that might not even last long-term, even if some version of a deal does get finalized. Yet, because the markets are focused on pricing in the content of Trump’s tweets, the markets are missing this huge detail about the trade war: that even if the tariffs go through, they’re negligible to the economy.

Investors (collectively: the market) are missing the bigger picture when it comes to US (re: Trump) and China’s trade war fallout impact. The media has been reacting to Trump’s twitter account (and getting labeled as “Fake News”) are making a big fuss about the potential impact of the trade deal.

As a result, the markets are increasingly concerned about the uncertainty of the trade deal. Concerns are that it might not get signed OR even if some deal gets finalized eventually, it will not last. Markets are overly focused on pricing in the content of Trump’s tweets about the trade war and missing the one key thing about the trade war. Even if the tariffs go through, it has a negligible impact on the economy. This short-sightedness is what’s causing the recent volatility in the markets.

Contents

Trade Drama Plot-Twist

Trump and China’s back and forth are a picture-perfect example of how the markets can so easily react to meaningless noise. The latest episode of ‘Trump versus China’ started on 5 May when Trump, complaining of sluggish progress in the trade talks, tweeted that he would raise tariffs from 10% to 25% on the existing $200 billion of goods. Trump also threatened to slap tariffs on all remaining Chinese imports if the two parties couldn’t agree on a deal by 10 May. Not surprisingly, China wouldn’t agree to his terms, and, this didn’t go over well with the markets.

For 10 months, China has been paying Tariffs to the USA of 25% on 50 Billion Dollars of High Tech, and 10% on 200 Billion Dollars of other goods. These payments are partially responsible for our great economic results. The 10% will go up to 25% on Friday. 325 Billions Dollars….

— Donald J. Trump (@realDonaldTrump) May 5, 2019

In an attempt to cheer up markets, both sides chalked up the talks as “candid and constructive”. The cosmetics proved short-lived, as more “tweet volatility” over the weekend suggested progress is anything but smooth.

Talks with China continue in a very congenial manner – there is absolutely no need to rush – as Tariffs are NOW being paid to the United States by China of 25% on 250 Billion Dollars worth of goods & products. These massive payments go directly to the Treasury of the U.S….

— Donald J. Trump (@realDonaldTrump) May 10, 2019

On 13 May, the markets priced in retaliations from China, and, like clockwork, China’s Ministry of Finance announced by midday in New York City that it will raise tariffs on US goods starting 1 June. Trump’s response only fired up media and market speculation more:

I say openly to President Xi & all of my many friends in China that China will be hurt very badly if you don’t make a deal because companies will be forced to leave China for other countries. Too expensive to buy in China. You had a great deal, almost completed, & you backed out!

— Donald J. Trump (@realDonaldTrump) May 13, 2019

Once again, the markets like the response didn’t either.

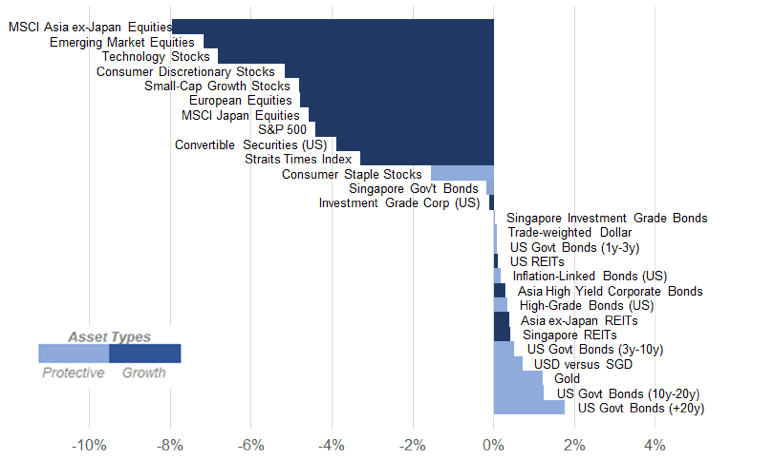

Month-to-Date Asset Class Performance

At the close of 13 May, the Shanghai Shenzhen China Stock index declined 6.2% on a Month-to-Date (MtD) basis, and the S&P500 lost 4.4%. The Asia ex-Japan region has been particularly sensitive to the trade tension. Aside from China’s large market share of 32.4% in Asia ex-Japan, the region also has 14.3% invested in South Korea, which is a highly export-dependent (and hence trade-sensitive) country. As of 13 May, Asia ex-Japan equities lost 8% MtD. As shown below, the Asia ex-Japan region has thus far underperformed the most across the majority of the growth-oriented assets (dark blue) we monitor. Emerging Market equities follow Asia ex-Japan’s underperformance, as Emerging Market exports depend heavily on Chinese consumption.

Tariffs Don’t Really Matter Much

From a geopolitical perspective, US-China relations matter a lot. The current US foreign policy path risks bringing the world to a more dangerous place over the long run. Supposing these tariffs go through, would the impact actually matter that much to the health of the global economy?

Trump’s critics, while vastly more accurate than he is, also, I think, get a few things wrong, or at least overstate some risks while understating others. On one side, the short-run costs of trade war tend to be overstated. On the other, the long-term consequences of what’s happening are bigger than most people seem to realize.

In the short run, a tariff is a tax. Period. The macroeconomic consequences of a tariff should therefore be seen as comparable to the macroeconomic consequences of any tax increase. True, this tax increase is more regressive than, say, a tax on high incomes, or a wealth tax. This means that it falls on people who will be forced to cut their spending, and is therefore likely to have a bigger negative bang per buck than the positive bang for buck from the 2017 tax cut. But we’re still talking, at least so far, about a tax hike that is only a fraction of a percent of GDP. ~Professor Paul Krugman in Killing the Pax Americana, New York Times

We are really talking about a fraction of a percent: the $65 billion in tariffs amount to a grand total of 0.19% of the combined GDP of the US and China ($34.1 trillion as of end of 2018 according to the US Bureau of Economic Analysis). If the $325 billion in tariffs also come into play, that’s still only 0.43% of the combined GDP.

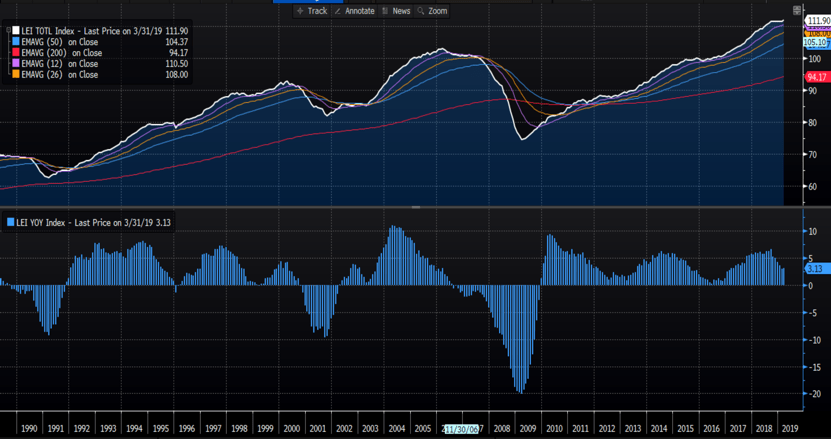

Truth be told, American consumers are the ones paying for Trump’s tariffs. Even then, it is not likely that tariffs would cause a recession in the US: firstly, leading indicators such as the Conference Board Leading Economic Index (LEI) is showing that the US economy has been stable and absolute level of output did not decline at all (re: above top panel). In terms of its rate of change (re: above bottom panel), the LEI has also stabilized after declining from its peak of 6.6% yoy in Sep 2018.

In fact, the latest print is starting to see a small pickup in LEI’s rate of change. Additionally, earnings expectation of S&P 500 companies have been revised upward since February 2019, confirming broad economic strength of the US economy. Lastly, the US can offset tariffs by some other form of tax cuts (e.g. another round of cuts that is focused on personal income tax). The US government can also hand out more subsidies to ease the pain for consumers, even if it’s financed by more government debts.

Lastly, although the trade fight is targeted at China at a time when its economy is slowing down, retaliatory tariffs that impact Chinese consumers are much smaller than what American consumers are paying. As we have already mentioned earlier, we are talking about a fraction of a percent of GDP in either country.

What Should Investors Do?

It’s not all fake news but don’t believe everything you read in the media. In the end, tariffs are not what is important, even though the media is making that out to be the story. What is important is that the economy is actually chugging along nicely, and leading economic indicators are still trending upwards. So, keep your head down, turn off your news notifications (if you relate to chicken little), and continue investing your savings at regular intervals (e.g. monthly).

In volatile times such as these, your consistent contributions is now buying you more units of securities than before – you can think of it as getting a discount on your purchase. Volatility is the price any long-term investor must pay in the short term in order to reap the returns that equities provide over the long term. If you feel uncomfortable with the ups and downs of your portfolio, you probably are taking on too much risk. Adjust it downward: sacrificing some returns but reducing the risks of you being but into a position to sell your investments at the wrong time for the wrong reasons.

Have enough drama and ready to invest in real life?

StashAway robo advisory signup with MyPF promo: 100% off fees for up to RM100,000 invested

{kind=link}

{kind=link}

Leave A Comment