A Malaysian shares her story and views on education funding and PTPTN. Your help is needed for the sake of your children and future generations.

Contents

My Formative Years

Do you care enough about education?

I was born into a low-income family, and this is something I am not embarrassed to admit. This period of my life is one of the unique chapters of history that shaped me into whom I am today. My primary and secondary schools were nothing spectacular – I attended a rural Sekolah Kebangsaan with financial assistance from my siblings and school food assistance programs like Rancangan Makanan Tambahan (RMT) at the time. This happened more than 20 years ago, and the burden of financial support was unremarkably stressful, even for a young ten year old girl.

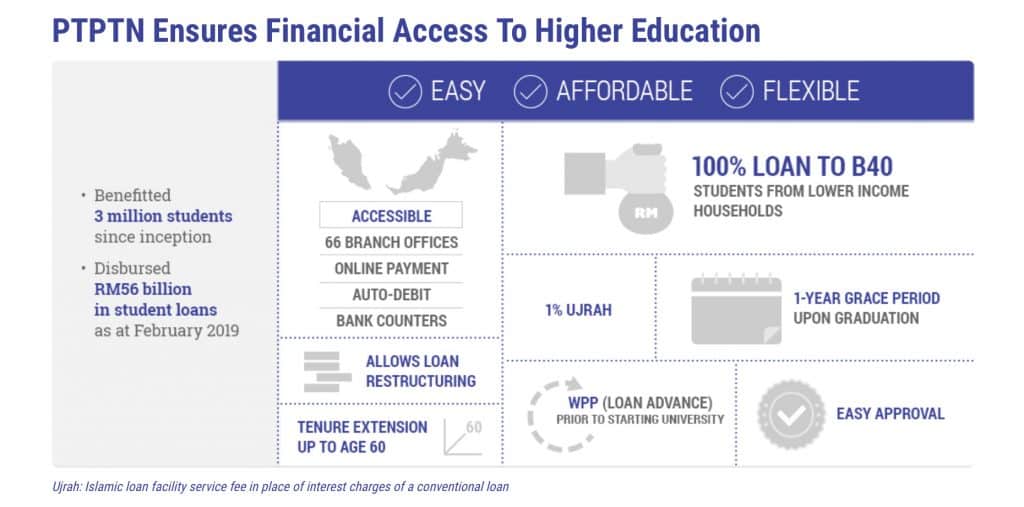

Despite the challenges, I managed to secure a place for a degree in Accounting studies. During that time, PTPTN (Perbadanan Tabung Pendidikan Tinggi National or National Higher Education Fund) was my primary source of fund that helped meet my financial needs and stay afloat throughout the duration of my studies. To help cover living expenses, I started a business on the side which helped make ends meet.

Source: PTPTN

A “first-class degree” was my one and only aim in mind, knowing that it was the golden ticket for me to convert the scheme from a loan into a full-fledged scholarship. This thought motivated me tremendously that I decided to forego my thriving business to make sure I was not distracted from achieving this goal. It was not easy to let go of my personal business which I had poured in blood, sweat, tears and countless hours.

Nevertheless, the difficult yet necessary decision that I made started to show merit. My name was listed in the Dean’s list for the of my studies. My study tips, inspirations and aspirations were shared by the Malaysian Institue of Islamic Understanding (IKIM). I was even featured on a program on ASTRO OASIS with a prominent motivational speaker. But the most memorable moment was still when I received an official letter from PTPTN stating that my higher education loan has been converted to a full scholarship. It was most definitely worth it!!

Dark Clouds Gather

Do you realise that the weather always changes?

But it was not all clear blue skies. Little did I know that dark clouds were gathering on the horizon. With the absence of my business as a significant source of income, financial burdens started building up and I was under tremendous financial pressure.

The realisation hit me that I needed to balance both strengthening my credentials for future prospects yet to start earning in order to survive. I applied for many promising opportunities and was finally accepted as a research assistant in International Shariah Research Academy (ISRA). During my tenure there, I worked hard and contributed in several international publications . I was joyous to be elected to join the first batch of Maybank Islamic Shariah Full Scholarship trainees. Looking back, none of this would be possible without the assistance from PTPTN during the fundamental stage of my studies.

Source: PTPTN

The recent media focus on PTPTN reminds me of my own journey which I have penned down in a few words. And as I reflect back, I know that not everyone has the opportunity and liberty I enjoyed with smooth-sailing approval of my education funding. The requirements for applicants Continue to become increasingly more stringent and even the process has become more complicated as my nephew and niece will attest to. Even the amount of funding that PTPTN provides may not cover the full cost of tuition, and excludes allowances and living expenses.

I am neither pointing fingers with regards to the new process required by PTPTN nor delving into politics. It is clear that these measures are necessary as PTPTN continues to struggle with late and non-payment. My five years experience working in a leading bank in Malaysia showed me the depth and seriousness of this recurring issue faced by PTPTN.

This Concern is Yours and Mine

Do you need to be concerned about education?

As a parent of two beautiful children, my priorities will always be “what is best for my children?”. And for any parent, education is especially important. Some parents would even start planning for their child’s education even before they welcome their child into the world. Many parents try their very best to strategically arrange that money will not be a limiting factor for their child to get a world class education and be the best he or she can be.

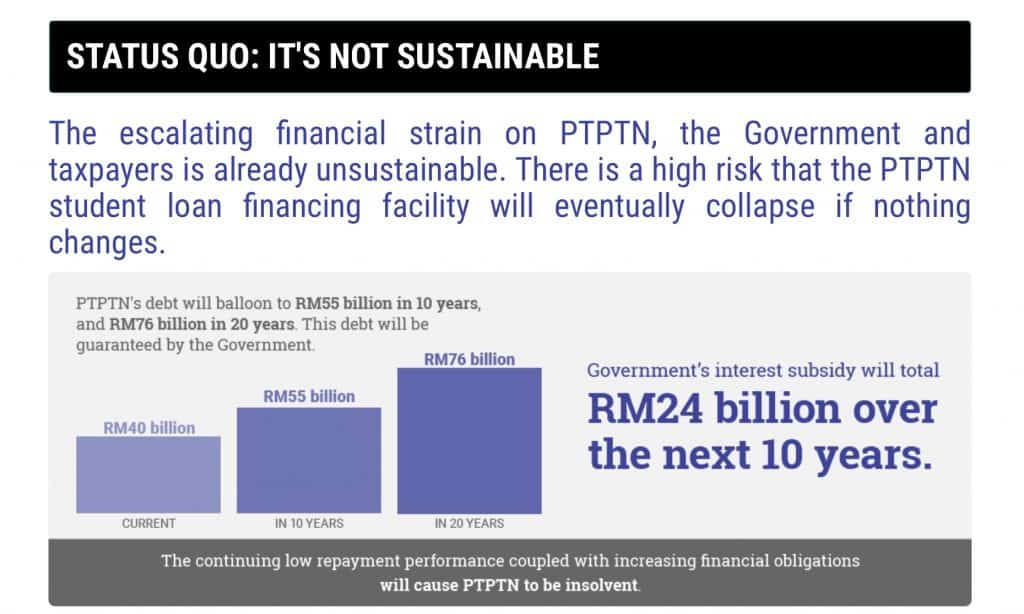

PTPTN in its public consultation paper highlighted that “more funds will be needed to support the growing number of students, which is projected to reach 250,000 by 2040″. PTPTN’s situation is dire with the following facts (as of end 2018):

- 51% (972,000 borrowers) default on payments.

- 32% (616,000 borrowers) pay inconsistently owing RM3.5b.

- 19% (356,000 borrowersj have never paid a single cent owing RM2.8b.

- Only 26% (499,000 borrowers) have paid back their education loan in full.

Source: PTPTN

Malaysia is a growing country with a growing population. This growth requires educational funding support to support human capital development. However, the scale is currently imbalanced due to inconsistent and non-existent repayments from current borrowers. If this continues on, it will inevitably lead to the collapse of the fund or require massive bailouts. The ones who will need to bear the consequences will be your children and your children’s children!

Now that you know the seriousness of the issue, what steps will you take? What proactive steps can you take to make sure education and future generations are prioritised?

Are you formulating a plan for the benefit of your children? Have you ever sat down and start gathering information on your child’s education plan? Have you anticipated the estimated future costs of education with rising inflation? Will your income and future income growth be able to match your child’s education needs in another 5, 10 or 18 years’ time? Are you gambling that your child will get a scholarship or that you will suddenly get a windfall “durian runtuh” when the time comes?

Education Starts with a Plan

Do you have an education plan?

For those who have a plan and are working towards it, props to you. You are not only one step ahead in securing what is best for your children but you are also applying another layer of protection towards your own wealth stability. This is because many parents love their children so much more than their own selves that they withdraw all their hard-earned retirement savings and EPF monies, sell off their home, or even take a personal loan to give their child an education.

This action, while self-sacrificial, is less than prudent as the parent ends up depleting their retirement monies which is meant to cover your living expenses in your golden years. What is worse than having children a world away is the possibility of being poor and having absent children.

Then there’s the other heart-breaking extreme where parents withdraw their children from school and are made to work in low productivity activities to help the family in coping with their lives. Subsequently, there are negative effects on the future of the children and on the earning potential of the household. This implication is making life more difficult and stressful” (Churchill, 2002; Matul, 2005; Hoogeveen et al., 2005; Cohen and Sebstad, 2006).

At the same time, we also hear of parents who have opted to pay for their children’s education by withdrawing from their EPF account whereby this imprudent action may lead to a depletion of retirement funds and a loss of future earnings.

Education is a Plan in Motion

Do take consistent and proactive action!

It is important that you and your spouse share similar ideologies when it comes to planning for your child’s education. Think and talk with your spouse about your child’s education plan to make sure your goals and actions are aligned. Consider having constructive discussion among your friends and family. Not only will such discussion be more worthy compared to gossiping, it also attracts individuals with similar ideas to you. This will also benefit those whom have not started planning for their child’s education to start thinking about it as well.

Be informed and get educated yourself on good ways to fund your child’s education (and no we are not necessarily talking about “education plans” or other insurance / takaful products). Be wary of wolves in sheep clothing who are only out to get your money into their pockets by preying on your vulnerability and emotions when it comes to matters concerning your children. Reach out to professionals who have your interest at heart and who can assist you in realising you and your child’s education dreams.

Your child’s education funding plan needs to be more than just buying an investment property, saying a prayer, and hoping for the best (or at least another property market boom right before your child needs the money). Have your own retirement funding plan in order or at least being worked on while you save and invest for your child’s education. Know what are the best options available for you and your child whether locally or internationally. Manage your cash flow well to prevent leakages and put your money to work for you.

And if you, your child or anyone you know is part of the 51%, remind the person to start paying immediately.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment