Upon approaching 40 years of age, most people are unsure of how to feel at this turning point in their life. Turning 40 is considered by many as the official entry point into middle age, which sounds depressing yet compared to ten years earlier, you are now more likely to be wealthier, have a career is progressing well, and have a personal life that is more or less stable.

All of life’s developments entail some modifications to your financial circumstance. Although such developments take place gradually, your 40th birthday is a good reminder to review how much your financial situation may have changed and what adjustments you need to make to adapt.

Contents

1. Have and maintain a healthy EMERGENCY FUND

Keep or maintain a 3- to 12-months emergency fund, depending on your family situation.

A report by BNM shows that about 75% of Malaysians cannot deal with an emergency of RM1,000. An independent 40-year-old with no dependents should ideally have saved living costs for three to six months to be used to cover needs in the event of work loss, vehicle failure, or home repairs. This emergency fund is essential to your welfare. If it comes to financial concerns, most people anxious about unforeseen expenses than anything.

A substantial emergency fund offers a sense of security.

2. Get down to business on your savings plan for RETIREMENT

An average retirement fund more than doubles between the 35–44 age category and the 45–54 age category. What this means is, you need to increase your retirement savings so that:

- you can start building up a substantial amount.

- you can have an improved retirement lifestyle based on new higher retirement targets since your current earnings (and expenses due to lifestyle creep) are higher compared to 10 years ago when the previous retirement target was set.

If you’re behind, few things you could do to catch up. For example:

- Increase your EPF contribution

- Earn more money – side gigs

- Cut major expenses

- Get healthy and fit to reduce medical expenses.

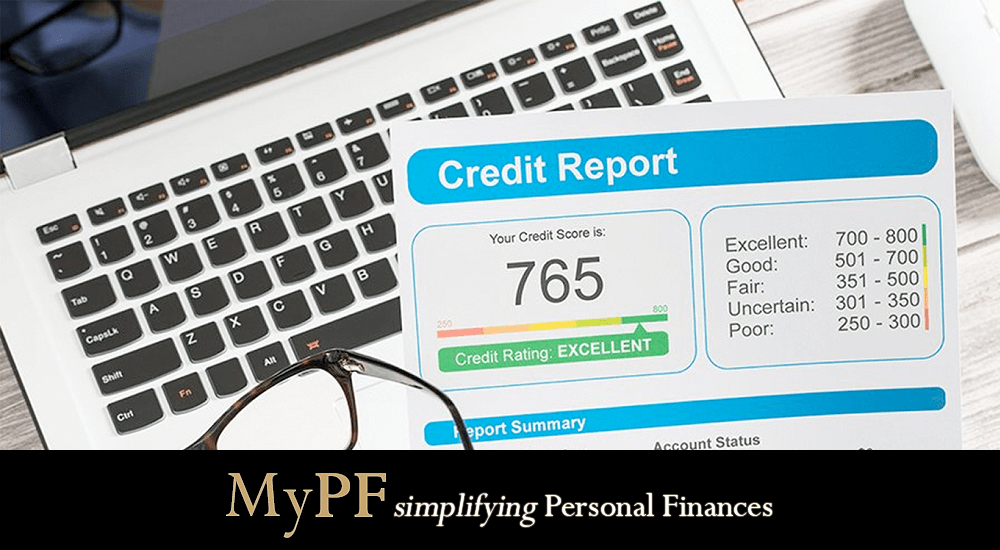

3. Keep up-to-date with your CREDIT SCORE

A higher scoring places you in a better position of getting a loan with a reduced interest rate than the norm. A 40-year-old average credit score is 685. To be on the safe side, just be ready to verify your credit score with CTOS. Getting your score from CTOS is free. You need not be a paying client.

4. Eliminate high-interest DEBT

It’s time to grow up if you’re still paying just the minimum dues on your credit cards balances.

Early in your career, it may be hard to match your earnings to your expenses. You might even have felt entitled to spend more than the cash you have. However, as your career progressed and your mind matured, you should have realized that living within your means is the most sensible choice. Debt with high interest will only drain your earnings. Accumulating debt, in particular a credit card debt, not only drains but continuously eats away at your wealth.

To plug this leak, plan a debt repayment scheme over a specified period to at least clear off the debt with the highest interest, and when it makes sense, move on towards clearing all other debt or at least towards not starting new ones unnecessarily. Not all debt is bad, but be wise in identifying which are which, especially high-interest debt.

5. Funds for your children’s higher education

If you have not started this yet, then it is high time you pull your socks up and look towards your children’s higher education savings fund urgently. With your age nearing 40, your children are like to be approaching college age. With limited time left, it is no longer a matter of saving up their “ang pow” money or birthdays monetary gifts, but rather saving at this point now requires customization to a particular program to reach the funds needed when the time comes.

6. Get organized

Organize, organize, and organize!

When you just started your career in your 20s, it is likely you gave little thought to your finances aside from coping with expenses. Back then, it was convenient to dump all your financial documents into a drawer as your “filing” system. But by your 40s, or even 30s, your financial affairs are more complex as it is no longer about simple expenses. You have more areas of personal financing to take care of such as various types of insurance for you and your family, loans (house, car, credit cards), more income to invest, and more expenses to pay. Do have all your financial documents neatly filed away so you can easily access them quickly when you need to reference any of them.

7. Establish and keep a budget

Do you maintain and track your finances in a budget? Or the “budget” is all in your head with only a general understanding of what your fixed and variable expenses are each month?

At 40 years old, what you spend and save every month should be documented somewhere quickly accessible. Don’t keep it in your head as we have so many things going on everyday it is easy to miss things out. You can use a paper system, a spreadsheet, else there are many apps available nowadays that are really useful. Whichever you choose, make sure it is something that you find convenient to update and maintain regularly. Have the discipline to key in your money movements. Set an alarm if that helps.

Why is this important? A budget is a pillar for your money policies. For example:

- How will you know how much you are likely to spend in your retirement if you do not know how much you are spending on wants vs needs now?

- How can you save an emergency fund if you do not know how much you need in an average month?

- How aggressive can your investment plans be if you do not know how much excess cash you have to play with?

Know what you have if you want to know what you should have.

8. Read widely about personal finances

Choose a topic you like to know more about–shares, savings, international markets–and begin reading. Many books on personal finances are out there. Reading these books will increase your financial knowledge and are there to you take charge of your finances.

Setting your financial goals is commendable. But, more important is to develop actionable action plans and carry them out consistently.

You may be on your way to achieving financial freedom with the right book.

9. Review your life insurance needs

The purpose of life insurance is to assist your family members to replace your income if you are suddenly incapable of providing for them. You may need to review the sum insured (to a higher amount) if the policy was effected years ago when your income was low. The new sum should take into consideration the standard of living they would be comfortable with.

10. Are your skill sets updated for relevancy?

Consider getting fresh training if you feel your skill sets are outdated. Or, perhaps, you just need a refresher course to keep yourself relevant.

If you already possess in-demand skills, consider if you are optimizing those skills career possibilities. If you are not, then why don’t you? What is holding you back?

11. Are there options to save on your housing loan?

Is there a possibility to garner some saving from your existing housing loan?

Refinancing is an option if the existing market interest rate is lower than what you are paying now. Another option is to reduce your interest payment by either reducing your loan period (paying more), or by paying the entire loan off if you can afford it.

Whichever way you choose, it all depends on your personal finances plans and where you want to prioritize “parking” your money.

12. Have you mastered or have the time for investing in the stock market?

If not, stop wasting your time. If you have not got into it by the time you are 40, then let it go. Rather than let your money idle in a low-interest generating asset or wait for you to master share investing, it is much more sensible to let a professional financial adviser handle your equity investing.

If you had invested since your younger years and your investments have not brought you wealth, now is the right time to seek professional help. Time is running out.

13. Stop keeping up with the Joneses

The days when you kept comparing yourself to others should be over for good.

Everybody has their own path, their own priorities, and have made their own choices, making each and every other person or family unique. At 40, you are definitely your own person. Even if it does not feel like it, by now, you already have sufficient accomplishments, your own thoughts about the world issues, enough knowledge to tell people what works and what doesn’t, and most importantly, the ability to decide what matters most to you.

A lifetime of constant rivalry and competition with everyone will not bring wealth and happiness for you. Contentment would.

If you cannot accept this then if it makes things easier, just believe that you are the winner. Afterall, truthfully, you are the only one in the race since nobody else is on the exact same path, so the only competitor is also the only winner. Strive to improve yourself by comparing to yourself. No matter how little or big the improvements are, you are already winning. Be happy.

Conclusion

Hopefully, your midlife personal financial examination will be better than previous reviews in your younger years. In fact, you may even be reaping in the benefits of reviews done in your younger years, setting yourself on the right path early on. If not, it is not too late, but it is time to wake up, play catch-up, and get going so that you’ve got some significant progress to show when you turn 50.

Don’t let this opportunity pass because you are only 40 once.

Are there any other areas you think need a midlife personal finances review should cover? Share your thoughts with us in the comments below.

{kind=link}

{kind=link}

Leave A Comment