The headlines this week has been on the yield curve. What’s happening? Why? What can you do about it?

Contents

The Yield Curve One-Liner

A yield curve inversion is when the US 10-year Treasury note goes below the US 2-year Treasury note. (T10Y2Y)

What’s Up YC?

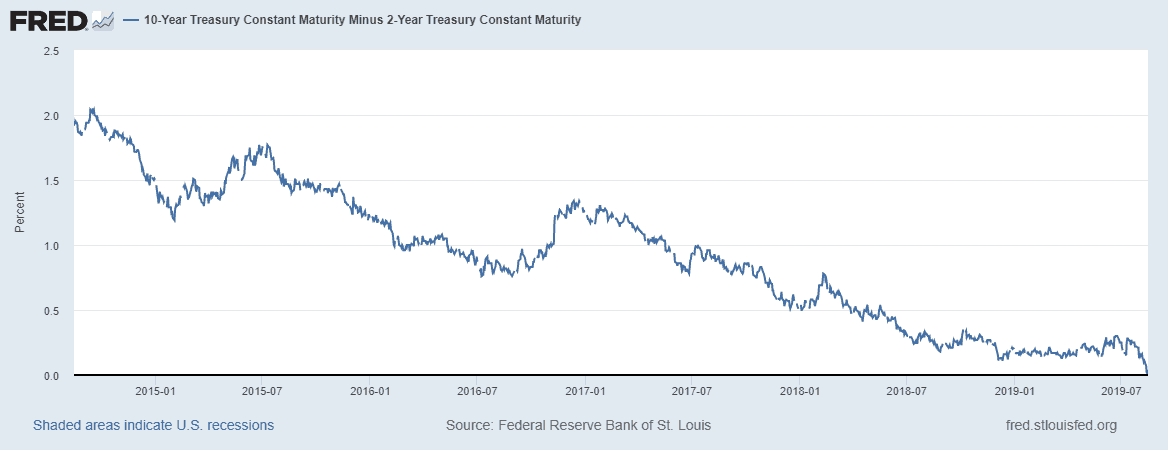

(Click to enlarge)

- On Wed Aug 14, 2019: 10-year Treasury note 1.623% dropped BELOW 2-year Treasury note 1.634%. Or basically, that short-term rates rise above longer term rates.

- The previous T10Y2Y yield curve inversion was in December 2015 (while the last T10Y3M inversion was in March 2019). The yield curve had actually begun flattening since 2013.

- A yield curve inversion is a leading indicator that investors are fearful of long term government bond returns, and a possible economic indicator of an upcoming recession.

- This caused the single worst US market day of 2019 with the US Dow falling 800 points (-3.05%) in a single day.

- However on Fri Aug 16, 2019 the yield curve righted itself with the 10-year Treasury note yield rising above the 2-year and markets followed suit in reverse.

What are We Curving Into?

“Historically, [the yield curve inversion] has been a pretty good signal of recession and I think that’s when markets pay attention to it but I would really urge that on this occasion it may be a less good signal.” Janet Yellen, Former US Feds Chair

What Can Reverse the Inverse?

- US Feds (and other central banks) traditionally have the option to cut interest rates although it is increasingly questioned how effective it may be.

Key economic signals to watch out for are

- Government debt growing

- Stock markets at all time high

- Unemployment rate increasing

- Falling industrial production

- Prolonged yield curve inversion

Recession: A Million Billion Dollar Question

Recession: a period of economic decline during which trade and industrial activity are reduced, generally identified by a fall in GDP in two successive quarters.

- An inversion usually eventually leads to a recession but not all inversions do.

- Recession likelihood only on prolonged inversion and typically happens 1.5 to 2 years after the inversion.

Asset/Sector Impact

- Perceived safe haven assets such as Fixed Income, Gold and selected safe haven currencies (i.e. Japanese Yen) rise.

- Recession proof sectors (and corresponding Stocks and ETFs) such as utilities, f&b, consumer staples, and selected REITs will be lesser impacted.

- Banks may slow down lending when deposit rates costs more than the interest rates earned from loans.

- Oil prices drop on recession fears (this is a mixed back as oil is also influenced by many other factors).

FAQ

Q: Should I liquidate my stocks?

Follow on with your personal investment plan and working with your financial planner (hopefully you have one!). You can take some profits or rebalance your portfolio as necessary following your investment plan exit strategies. Try to aim to be at least portfolio neutral if a recession wipes out 30-40% of your equity portfolio value. (Our internal A.I. team’s “crystal ball gazing” opinion is that we aren’t that pessimistic but instead view it as a relatively milder correction).

Tip: Come join in the discussion at the Personal Finances Community Fb group.

Q: How much cash should I hold?

It may be good to increase cash (and cash equivalents) holdings. A good range for many would be around 10%-20% of your overall investment portfolio (and 30-40% of your equities portfolio). Our Premier members would have noticed a buying activity slowdown in our long term value investing model portfolios (Bursa / US) as markets are near highs and fundamentals show very few good opportunities.

Q: Should I stop investing totally then for now?

No man (or woman) can actually tell you when the next recession is going to happen (till it happens!). You will lose out on opportunity costs if you’re not invested. Consider taking a less risky approach by buying a basket of asset classes including a possibly heavier weightage in fixed income/bonds/neutral sectors whether its through managed portfolios, ETFs or robo advisory (as opposed to investing in individual companies).

Q: What else can I do to prepare?

Talk to a licensed financial planner here or at SmartFinance.

Also seriously consider having gold in your investment portfolio to reduce your overall investment portfolio volatility.

(Note: Premier members, we have a few other gold investment options so do contact your licensed financial planner and not the earlier link)

You May Also Like

- A guide to bonds investing

- Former Fed chair Janet Yellen says yield curve inversion may be a false recession signal (cnbc.com)

- US Federal Reserve Bank 10-Year Treasury Minus 2-Year Treasury (fred.stlouisfed.org)

- Is Malaysia in recession or depression?

- Latest Base Rates, Base Lending Rates and Interest Rates

{kind=link}

{kind=link}

Leave A Comment