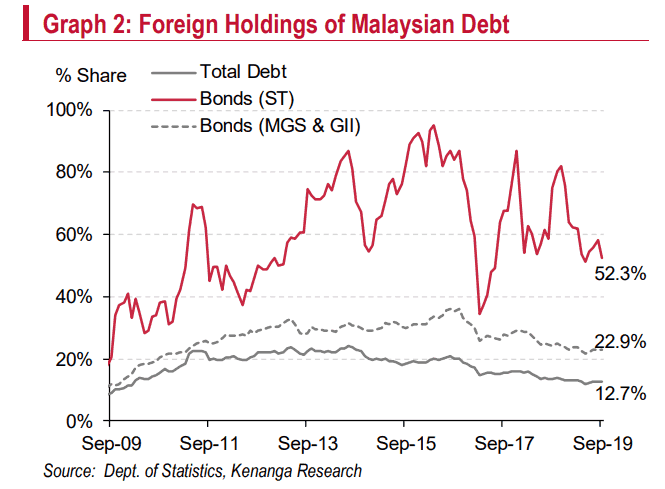

Foreign holdings of government debt expanded in September.

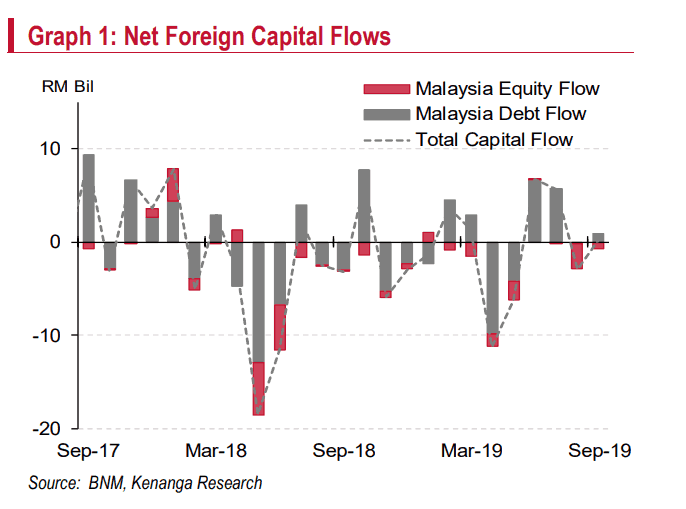

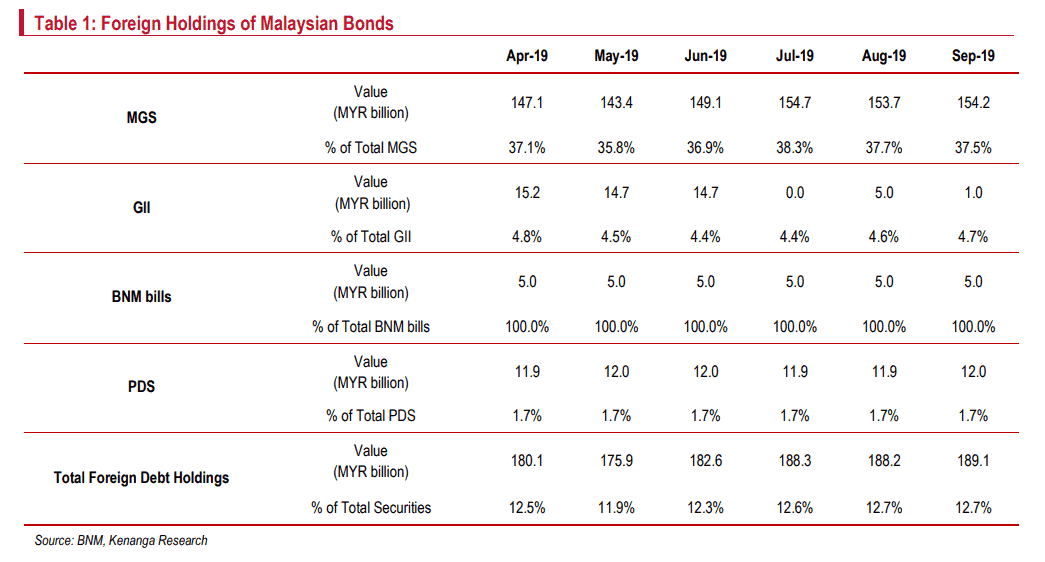

Foreign investors turned net buyers of Malaysia’s debt securities in September, as total foreign holdings expanded by RM0.9b (Aug: +RM0.1b) or 0.5% MoM (Aug: +0.05%) to RM189.1b (Aug: RM188.2b). However, the share of total foreign holdings of Malaysia’s debt was unchanged at 12.7% for two consecutive months, while Malaysia’s total outstanding debt increased RM3.0b in September. Meanwhile, foreign investors remained as net sellers in the equity market in September with foreign holdings fell by RM0.6b (Aug: -RM2.8b). Collectively, the capital market registered a net inflow of RM0.3b of foreign funds during the month (Aug: -RM2.8b) despite uncertainty in the global economy and financial market.

September’s net inflow in debt capital market was largely driven by a net increase in holdings of Malaysian Government Securities (MGS) (+RM0.5b; Aug: -RM1.0b), Malaysian Islamic Treasury Bills (MITB) (+RM0.2b; Aug: +RM0.4b), Malaysian Government Investment Issues (GII) (+RM0.1b; Aug: +RM0.5b) and Private Debt Securities (PDS) (+RM0.1b; Aug: +RM0.02b). Though the debt capital market recorded a net inflow of foreign holdings, its share to total debt remained unchanged at 12.7%. However, share to total government bonds inched up marginally by 10 basis points to 22.7% in September, after FTSE Russell decided to keep Malaysia in the watchlist until the next review on March 2020.

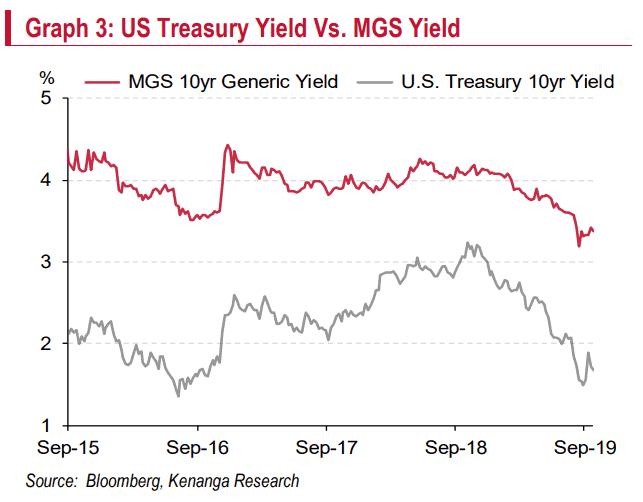

As of September this year, total capital outflow thus far stood at RM3.8b, far lesser than RM31.2b of outflow recorded in the same period of last year. This was supported by a net inflow in the debt capital market (Jan-Sep 2019: +RM4.3b) despite continued outflow in the equity market (Jan-Sep 2019: -RM8.1b). In the near term, we expect net-outflow to persist mainly due to elevated geopolitical risk and uncertainty over US-China trade negotiations as it resumes high-level trade talks in Washington this week. Nonetheless, the outflow for this year is expected to be less compared to the previous year, given that major central banks led by the US Fed and European Central Bank have pivoted towards monetary easing. Against this development, the US 10-year Treasury note average yield recorded an increase of 8 basis points (bps) to 1.71% in September, while the benchmark Malaysian 10-year MGS average yield continued to edged down by 2 bps to 3.36%, bringing down the average yield spread to 165 bps (Aug: 174 bps).

Overall, we maintain our view that Bank Negara Malaysia (BNM) may still have the scope to cut the overnight policy rate by another 25 bps to 2.75% at its last Monetary Policy Committee meeting in November this year. While the domestic sector seems to be resilient, the downside risk emanating from the external sector with regards to growth slowdown in major markets, declining global trade, and a prolonged US-China trade feud may weigh down domestic growth. Moreover, the easing cycle by major and regional central banks would give more space for BNM to embark on another rate cut. This would also exert more downward pressure on the Ringgit, which we project to depreciate to RM4.20 against the greenback (2018: RM4.13) by year-end.

Signup for Rakuten Trade

Invest in Bursa shares or ETFs by opening a low cost brokerage account today!

Account opening link: RakutenTrade.my

Referral code: MYPF

Share with us your thoughts in the comments below.

{kind=link}

{kind=link}

Leave A Comment