Stashaway is here to explain why there isn’t an ETF bubble. Let’s look at the bigger picture. The original version of this article was published on StashAway.my.

There has been a lot of fear mongering recently around how ETFs and other passively-managed funds could trigger the next bubble. Critics assert that passive investing vehicles, such as ETFs, are a systemic threat because investors are putting more money into entire indices that are based on market values, rather than buying into the underlying assets themselves. These forecasts emerged the moment the passive investment inflows surpassed active management inflows for the first time.

Stashaway is here to explain why there isn’t an ETF bubble. Let’s look at the bigger picture.

With the rising popularity of index funds, critics allege that ETFs give too much importance to large companies. They allege that ETFs’ tracking activities create FOMO (fear of missing out) amongst investors, potentially leading to concentration risk in the market. The reality is that index-tracking ETFs are designed with the purpose of diversification, and do so by buying a broad basket of constituents underlying an asset class. As an example, VWO is an ETF that tracks the FTSE Emerging Markets Index, and it has a total of 4,131[1] underlying companies in a diverse range of industries based in countries, such as Brazil, Russia, India, Taiwan, China, and South Africa, amongst others.

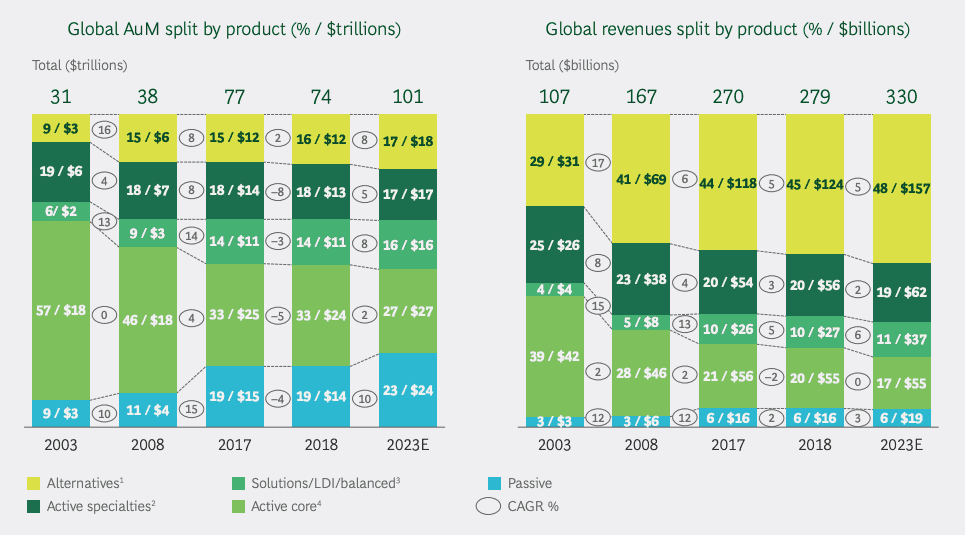

Another reason why there isn’t an ETF bubble is that ETFs and other passive investment vehicles are still such a small portion of the market, and so they aren’t a systemic threat, either. According to ETFGI as of the end of 2018, assets managed by ETFs were around $6.483 trillion USD. This is merely 8.7% of global assets under management ($74.3 trillion USD[2]). Even if we include non-ETF index funds in the mix, passive funds collectively managed about $14 trillion USD. As can be observed on the left side of the figure below, this is still only around 19% of global AUM. Given how small a portion ETFs and indexed funds are of total global fund management industry under management, they can’t possibly be a true systemic risk.

Actively-managed fund products continue to slip

(Sources: BCG Global Asset Management Market-Sizing Database 2019 and BCG Global Asset Management Benchmarking 2019[3])

To put that $14 trillion in perspective, consider this: if we lump actively-managed “core” and “specialty” funds together, the group collectively manages an AUM of $37 trillion USD, which is a whopping 51% of global AUM. This figure would climb up to 67% of global AUM if we also include the “alternatives” category. Alternatives consist of hedge funds, private equity, real estate, infrastructure, commodities, private debt, and liquid alternative mutual funds, such as absolute return, long and short, market-neutral, and trading-oriented. Maybe we should be more worried about active managers crashing the markets. After all, they enjoy the majority share of the funds managed, they can short the market, and they can leverage (borrow multiples times their assets under management).

According to the SPIVA scorecard[4], the majority of actively-managed funds underperformed their benchmarks. Regardless of which timeframe we look at, 3, 5, 10, or 15 years, the numbers are stacked up against the active managers. Why? Because, by definition, there can only be so many great active managers. If they were all great, then, well…

Ultimately, ETFs provide the low fees and diversification that investors need to build meaningful long-term wealth, so that’s not what will crash the market. What will crash the market is when someone misuses tools, like what happened with the CDOs in 2007.

References

- As of 31 August 2019

- “Global Asset Management 2019 – Will these 20s Roar?”, Boston Consulting Group

- Explanatory notes to Figure 1.

LDI = liability-driven investments; ETF = exchange-traded fund. (1)Includes hedge funds, private equity, real estate, infrastructure, commodities, private debt, and liquid alternative mutual funds (such as absolute return, long and short, market-neutral, and trading-oriented); private equity and hedge fund revenues do not include performance fees; (2)Includes equity specialties (foreign, global, emerging markets, small and mid caps, and sectors) and fixed-income specialties (emerging markets, global, high yield, and convertibles); (3)Includes target-dated, global asset allocation, flexible, income, liability-driven, and traditional balanced investments; (4)Includes actively managed domestic large-cap equity, domestic government and corporate debt, money market, and structured products; (5)Includes absolute return, long and short, market-neutral, and trading-oriented mutual funds; (6)Includes target-date, global asset allocation, flexible, and income funds; (7)Includes foreign, global, and emerging-market equities; small and mid caps; and sectors; (8)Includes emerging-market and global debt, high-yield bonds, and convertibles; (9)Includes actively managed domestic large-cap equity; (10)Includes actively managed domestic government and corporate debt and (11)Management fees net of distribution costs. - The comprehensive SPIVA scorecard for 2018 can be found at https://www.spglobal.com/_assets/documents/corporate/us-spiva-report-11-march-2019.pdf

Account opening link: Stashaway.my

Exclusive MyPF x StashAway signup promotion with 100% fees waived! No minimum investment amount needed for initial signup.

You May Also Like

- How to StashAway

- Introducing Malaysia’s First Robo Advisory, StashAway

- Markets Are Noisy, but We’re Not Listening

- The Best Offence Is a Strong Defence, Even in Investing

- StashAway x MyPF Promo

What are your thoughts on an ETF bubble?

{kind=link}

{kind=link}

Leave A Comment