What you need to know about the changes in investment-linked life insurance policies which has started in 2019 and 2020. Effects include medical repricing and higher premiums to be paid.

Contents

New Regulations on Investment-Linked Insurance

These changes were made after the consultation period of the Life Insurance and Family Takaful Framework (LIFE). Changes made are to strengthen requirements on the conduct of investment-linked (IL) business with the primary objective to protect the interests of consumers. The changes are effective for both conventional and Takaful Investment-Linked Policies (ILP).

Key Changes

- Implementation of standards on Minimum Allocation Rates to protect the account values of IL policy/certificate owners;

- Minimum standards on sustainability tests and communication to policy/certificate owners to improve long term persistency of IL policies/certificates and consumer awareness; and

- Strengthened disclosure standards on product illustration to facilitate more informed decision-making by consumers.

New Minimum Allocation Rate (MAR)

Effective: July 1, 2019 (For Takaful: effective July 1, 2020)

Change: New life insurance policies issued are required to comply with new Minimum Allocation Rate of at least 60% for ILP policies with contribution 20 years or longer. ILP policies with contribution 3 to 19 years are also capped on maximum allocation to non unit fund(s) based on the length of the contribution years.

| Year of Premium Contribution | MAR |

|---|---|

| 1 to 3 | 60% |

| 4 to 6 | 80% |

| 7 to 10 | 95% |

| 11 onwards | 100% |

Impact: While life insurance costs remain the same, the premium required to make sure that the new MAR is met will see an increase in the premium amounts. Existing life insurance policies issued on or before June 30, 2019 will not be affected by the new MAR guidelines.

Source: BNM

Management on Sustainability of Cover

Effective: January 1, 2020

Change: Annual statements sent to life insurance ILP policy holders will show the length of coverage based on current premium. Policy owners with ILP policies which will lapse within 12 months will be notified. Maximum fund management charges are also capped at 1.0% of the fund’s Net Asset Value (NAV) for money-market/fixed income funds, and 1.5% of the fund’s NAV for other funds.

Impact: Policy owners can voluntarily increase the premium payment, or make single top-ups which will in turn increase the length of coverage. Lower fund management charges are beneficial for policy owners as it reduces the costs of owning a life insurance policy. A licensed person must ensure that premium / takaful contribution are able to sustain its coverage until the end of contractual term.

Note: It is misleading to tell consumers that premiums are definitely going to increase, and anyone providing ILP products should refrain from doing so.

Source: BNM

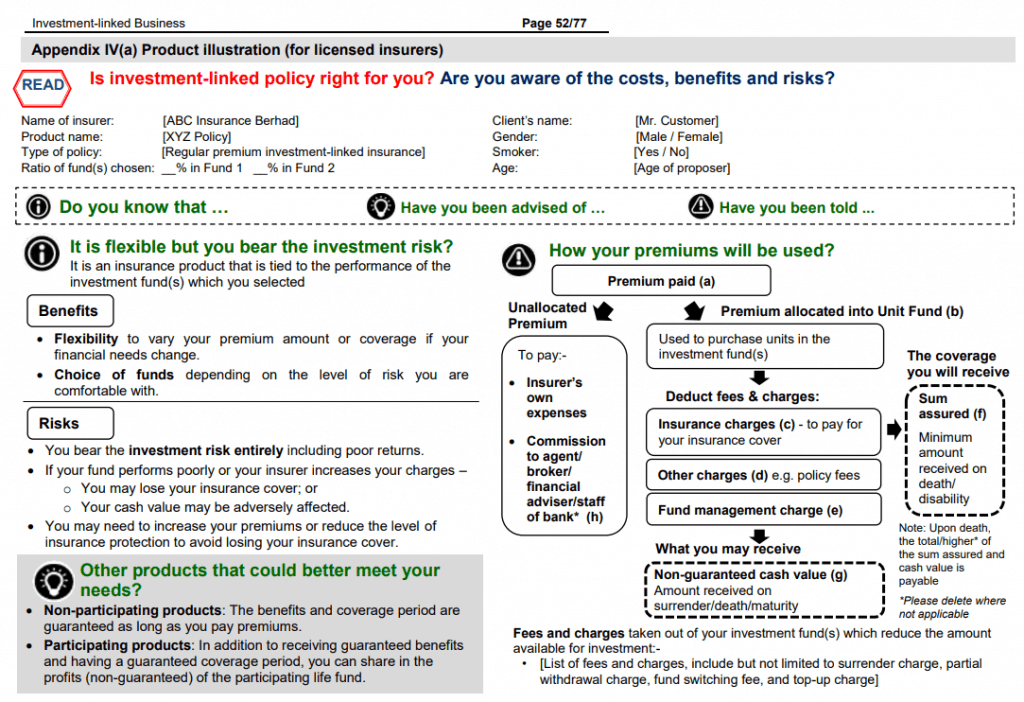

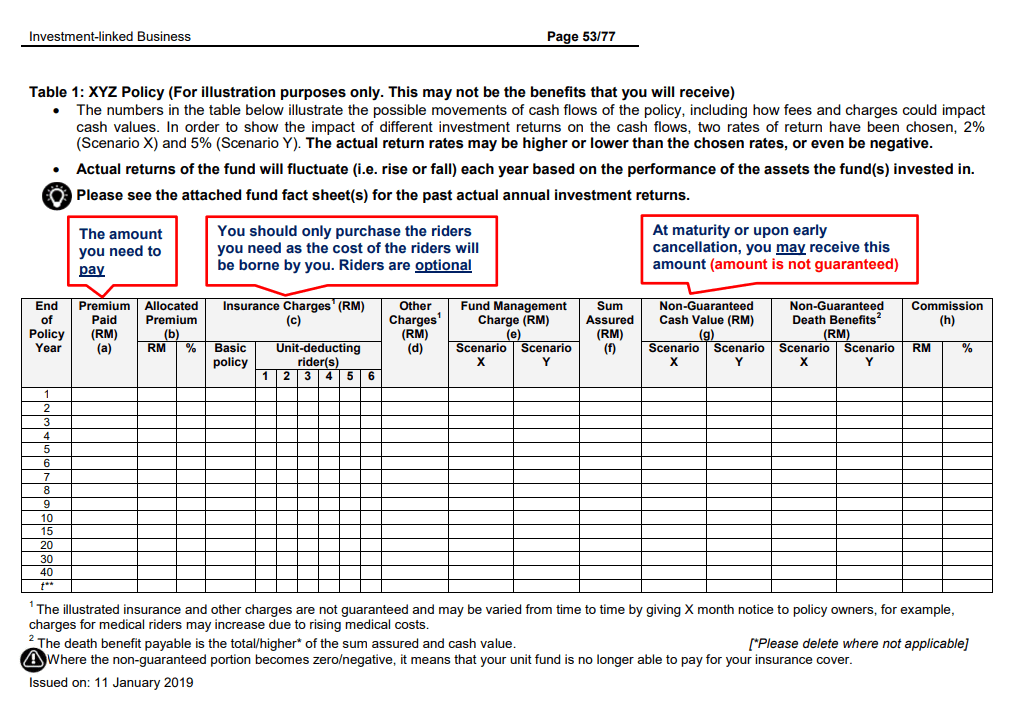

New Product Illustrations

Effective: January 1, 2020

Change: ILP policy illustrations must show projected return X and Y scenarios of 2% and 5% respectively (For equity funds, the historical 10-year average historical FTSE Bursa Malaysia KLCI returns can be used for Scenario Y for year 1-year 20). The non-guaranteed portion must be clearly illustrated in the product illustration.

Impact: The new projected returns X and Y scenarios can better demonstrate to policy owners the interactions between the cash flows described on the summary page of product illustration, without giving rise to undue expectations. This provides better standardisation at more conservative return projections.

You May Also Like

- Policy Document on Investment-Linked Business (bnm.gov.my)

- Insurance Premiums Unchanged for Investment-Linked Product Policies (thestar.com.my)

- Life and Disability Insurance

{kind=link}

{kind=link}

{kind=link}

Leave A Comment