BNM reduced the Statutory Reserve Requirements by 0.5% to 3.0% to ensure sufficient liquidity in the banking system. We are positive on the cut as it will release extra liquidity into the system, mitigating downward pressure on NIM. Easing monetary conditions is supportive of loans growth and help stabilise asset quality.

BNM reduced its Statutory Reserve Requirement to 3.0% last Friday. BNM announced the reduction in the statutory reserve requirement (SRR) ratio from 3.5% to 3.0%, effective from 16 Nov 2019, to ensure sufficient liquidity in the domestic financial system. The last time BNM cut the SRR was in Feb 2016 when the central bank cut the ratio from 3.5% from 4.0%. The central bank highlighted in a statement that the SRR is an instrument to manage liquidity and is not a signal on the stance of monetary

policy.

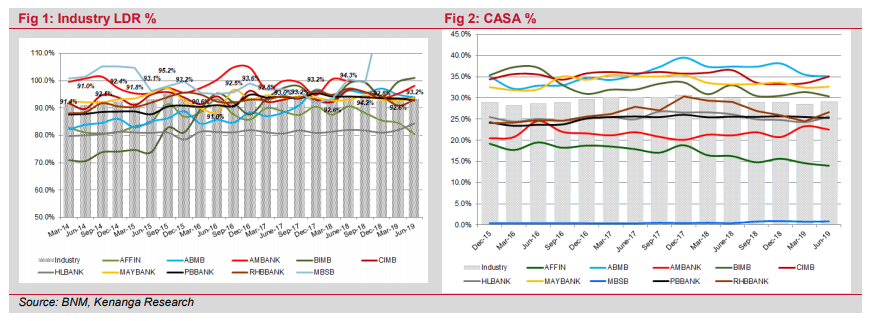

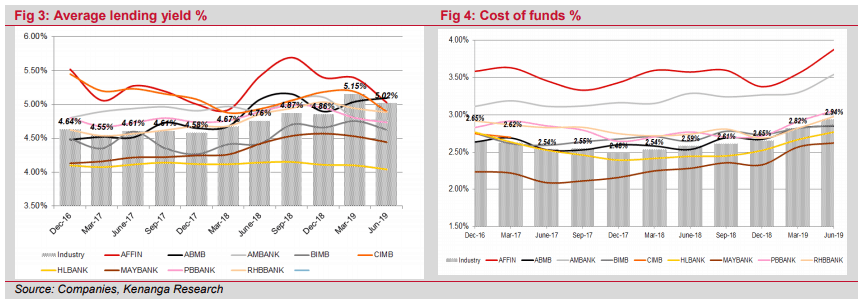

Higher deposits growth resulting in higher cost of funds. As of Sep 2019, Loan to Deposit Ratio (LDR) in the Malaysian banking system stood at 89% with excess liquidity at 10.5% as compared to 90% and 10.1%, respectively in September 2018. Slower loans growth as compared to deposits contributed to the uptick in LDR. This resulted in higher costs of funds (COF) as banks chased deposits by giving better rates with 3-month FDs outpacing average lending rates by 27bps to 17bps (from Sep 18 to Sep 19) despite the overnight policy rate (OPR) cut in May 2019.

Near term positive for banks, Net Interest Margin (NIM) likely to improve. As the Statutory Liquidity now stands at RM32b, the reduction will release an estimated RM4.6b into the banking system, compared to total deposits in the banking system estimated at around RM1,952b. We see this benefitting banks with above sector average LDR ratio and tight CASA namely AMBANK (98%), BIMB (101%) and MBSB (117%) relative to the industry LDR (93%) as these non-income generating liquidity released from reserves can now be lent out by banks in meeting loan demand. Cost of finances (COF) should stabilize (with the amount released coupled with net stable funding ratio (NSFR) fully complied and credit demand expected to be moderate for 2020) and NIM to recover, should credit demand turned upwards given the accommodative interest rate environment ahead.

Maintain OVERWEIGHT. As such, we reiterate our OVERWEIGHT call on the sector. With the SRR reduction we may see deposit rates on an easing bias. Coupled with resilient asset quality, this augurs well for banks as they will have help lower COF ahead. Easing monetary conditions is supportive of loans growth and help to stabilise asset quality, improving prospects of recoveries. These, coupled with the sector being undervalued, in our view, as the larger banks have largely underperformed year-to-date are reasons why we have maintained the sector at OVERWEIGHT.

Definition of Sector Recommendations**

- OVERWEIGHT : A particular sector’s Expected Total Return is MORE than 10%

- NEUTRAL : A particular sector’s Expected Total Return is WITHIN the range of -5% to 10%

- UNDERWEIGHT : A particular sector’s Expected Total Return is LESS than -5%

**Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage.

Signup for Rakuten Trade

Invest in Bursa shares or ETFs by opening a low cost brokerage account today!

Account opening link: RakutenTrade.my

Referral code: MYPF

Share with us your thoughts in the comments below.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment