If you want to know how healthy your debt level is, you can use financial ratios as a check-up. That’s what your bankers do before they decide on a loan request as the banks need to understand how strong you are financially.

If you are looking to buy a house, a car, or pursue further education, taking a loan from a bank is a common step. However, despite having good income and good debt payment records, banks may still reject your application or may choose to approve it with a higher interest rate. Why? One possibility is excessive debt. The bank assessment concluded that your future capability to service a new loan is doubtful. You already carry too much debt. Taking on another debt may just be the needle to prick the swollen bubble. What it means is…. your financial health is deteriorating, and the bank is not willing to take the risk.

But, how are banks so certain they know your financial future?

Banks use financial ratios as part of their stringent assessment process to determine a potential borrower capacity to repay a loan. If you failed to get a loan from banks, it is a strong indicator that your finances are not as healthy as you thought.

Getting turned down by banks won’t harm your credit score but the credit inquiry caused by the loan application, will. Know and monitor your financial health through financial ratios. So, before you apply for any loan, use these financial ratios to self assess your eligibility or chances of success. Also, the ratios can highlight any red flags or signs of excessive debt so you can take remedial actions soonest.

Contents

So, what are the 5 important financial ratios you must know?

PF Ratio #1. Personal Net Worth (your wealth)

How to calculate?

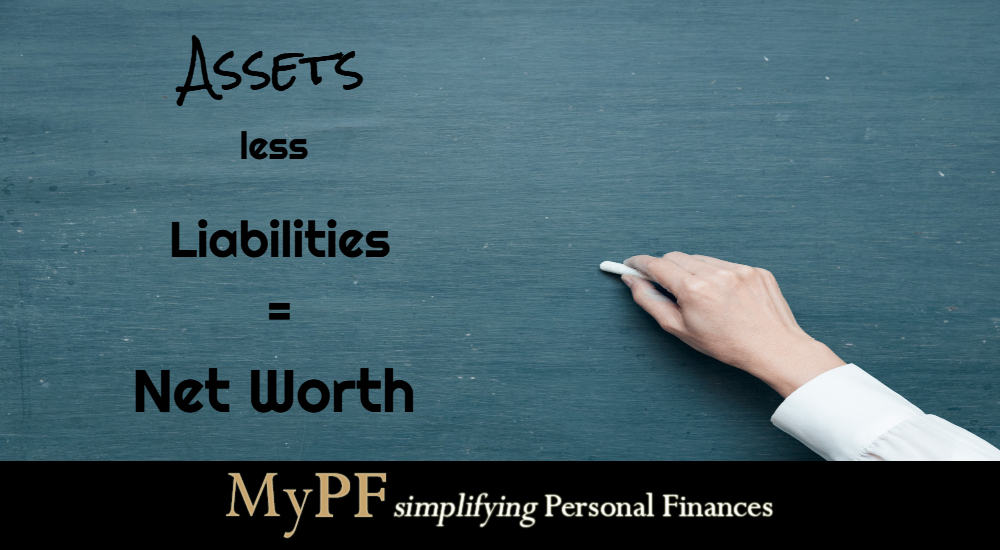

Your Personal Net Worth = Assets minus Liabilities

- Your assets are things that you own and can sell for cash. Examples are stocks, bank accounts, EPF retirement funds, properties (house, land), cars, jewelry, and cash.

- Liabilities are your debts, such as bank loans, credit cards, unpaid bills, and education loans.

What does it tell you?

The differences between what you have (assets) and what you owe (debt) is your net worth. And, while this may not be a ratio, it is a major factor driving many ratios. Net worth gives you an overview of your finances. It can be positive or negative. Negative values may not mean that you are facing doomsday or that you are someone who is not good at managing your finances. It just shows, for now – you have more liabilities than assets. That all. What’s more important is the overall trend.

While the value of net worth is helpful, recording the progress over time gives you a deeper insight into your wealth. You can see your net worth as a financial report card when measured regularly. This encourages you to review your current financial situation and allows you to do what you need to do to meet your financial goals.

Example

Your assets = RM100,000,

Your liabilities = RM50,000

Therefore, your Net Worth is RM50,000. If we exchange the figures, it becomes negative (-veRM50,000). It’s ok to have a negative net worth now. The important part here is to note down the number and track it periodically.

Goal/Action

Net worth is a measuring meter of your wealth and how successful you are in managing your money. Don’t compare your net worth with other people. It’s meaningless. Every individual’s situation or circumstance is unique. Comparison is only meaningful on your progress.

So, concentrate on growing your net worth at least 5% each year. How? Pay down your debt and/or pile up your asset.

PF Ratio #2. Assets-to-debt ratio (Solvency)

How to calculate?

Assets to Debts Ratio = Total Assets / Total Debts

- Assets are things that are worth money such as stocks, bonds, or your family home.

- Debt is what you owe someone such as a car loan, a house loan, credit cards balance, or a personal loan.

What does it tell you?

- This ratio tells you if you have over-borrowed, i.e. you are struggling with financial insolvency issues. (Financial solvency is the capacity of a person, business, or organisation to meet their debts and have the cash to pay for future requirements).

- Want to apply for a loan? Use this ratio to find out whether your finances have any room left for another loan. If you cannot afford the new loan repayment because you have exceeded your repayment capability limit, then do not force yourself to take up a new loan. If possible, wait until you reduce your existing loans.

Example

If total assets (RM40,000), total debt (RM80,000),=;

Assets to debts ratio = total assets (RM40,000)/total debt (RM80000) = o.5 or 50%

This ratio means you owe twice what you own. With an asset-to-debt ratio of 50%, you are technically considered financially insolvent despite you earn adequate money to meet your prevailing debt on time.

Goal/Action

Aim for a ratio greater than 1 (100%) which means you have more assets than what you owe (debt). If you keep your ratio above 1, you may better qualify for a loan.

PF Ratio #3. Basic Liquidity ratio (Liquidity)

How to calculate?

Basic Liquidity ratio = Cash and near-cash / Monthly expenses

- Cash and near-cash equivalent include savings, bank current account, fixed deposit, marketable securities, and any assets which can easily turn to cash within 3 months.

- Monthly expenses are gross expenses for a month.

What does it tell you?

- A measure of a person’s capability to cover his / her everyday expenses if faced with an emergency or unexpected circumstance.

- Or, how many months would the saving last if all the income streams unexpectedly stopped. For example, losing a job.

- Enables an individual to know their financial resilience.

Example

If you have RM6,000 in your savings and you spend RM 2,000 a month, then your basic liquidity ratio is three (3) months (RM6,000/RM2,000).

This means you can take care of three months of daily living expenses if you suddenly lose your income.

Goal/Action

Target to maintain a specific level of liquidity (emergency fund to cover 6 months’ expenses) to avoid unforeseen financial difficulties.

PF Ratio #4. Total debt payment to gross income ratio (Debt Servicing)

How to calculate?

Debt Servicing ratio = Total Monthly Debt Payment / Total Monthly Gross Income

- Total monthly debt payment (house, student, car, credit cards, etc.)

- Total Monthly Gross Income is all your income

What does it tell you?

- It tells what percentage of your earnings is used to pay off debts. And if you still have room to take out a new loan with your current income.

But banks have their own calculations where the total amount of debt repayment cannot exceed 60% of total income. Though most banks use the 60% rule, there are exceptions. Beside the DSR, banks also look at other factors such as net worth, employment status and income consistency.

Example

For instance, if your total monthly income was RM2,800 and your overall debt expenses are RM1,000 a month, the percentage would be 0.36. What it means is each month your debt settlement take up 36 percent of your gross revenues.

Goal/Action

Your goal should ultimately be zero debt and high savings as your age/earnings go up.

PF Ratio #5. Savings ratio

How to calculate?

Savings ratio = Savings / Gross Income

What does it tell you?

- This ratio shows how much a person is saving for future purposes.

- But, more important question is, “Are you putting enough money into your savings?”

Example

The simplest manner to grow your wealth is to reduce spending to increase savings. But how can you tell whether you have put in enough savings? For instance, say your gross monthly pay is RM2,000 and you save RM200 a month. Your amount of savings is 0.10 or 10%. Is this enough?

Goal/Action

How much to save each month? This is a common question posed by everyday man-in-the-street. To be honest, there is no one-size-fits-all ratio. Your age, income, lifestyle, and financial goals dictate that ratio.

Financial experts advised:

- The minimum amount to save is 15% to 20% of your gross income.

- If you want a comfortable life during retirement with no financial worries, you need to have 70% to 80% of your pre-retirement income.

Conclusion

Use these 5 financial ratios as a quick check-up tool to monitor and quick overview of your financial health. Having a clearer picture of your finances helps you to take action to get it back on track if it deviates from goals set.

It’s advisable to recalculate these financial ratios when you:

- plan to get a loan,

- have a notable increase in income or

- certain debts reduced/settled

There are other financial ratios you can use to zoom into the specific areas. We will discuss those in another article. But, for now, let’s start off with the above top 5.

You May Also Like

- Warren Buffett’s Annual Letter 2018

- What do Malaysians Ask About Financial Planning According to Google

- 5 Life Reasons for an Estate Planning Review

Find out what are your ratios for these top 5 and let us know if you have any queries on the results.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment