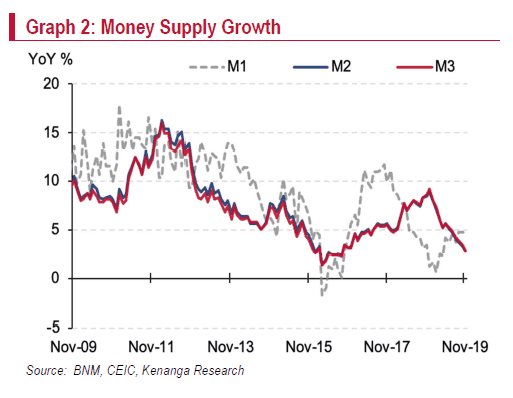

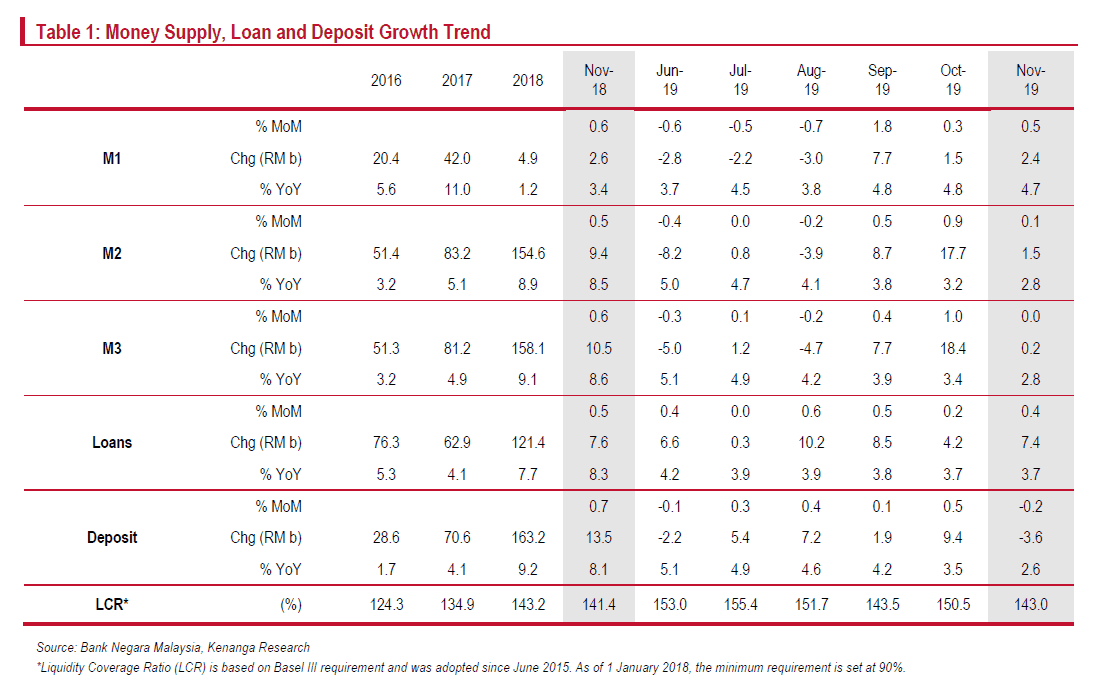

M3 money supply growth weakest in over 3 years, loan growth remained at a 16-year low.

Contents

M1, M2, and M3 Definitions

- Money Supply M1, also known as narrow money, includes coins and notes in circulation and other assets that are easily convertible into cash.

- Money Supply M2 includes M1 plus short-term time deposits in banks.

- Money Supply M3 includes M2 plus longer-term time deposits.

M3 money supply growth weakest in over 3 years, loan growth remained at a 16-year low.

- M3 growth decreased to a 38-month low (2.8% YoY; Oct:3.4%).

- MoM: 0.0% (Oct: 1.0%).

- Moderation led by narrow quasi-money, followed by deposits placed with other banking institutions and M1.

- …as slower growth in public spending outweighed lessened decline in net external reserves

- Net claims on government (2.7%; Oct: 12.3%): dwindled to a 17-month low on a substantial slowdown in credits extended to the government (9.1%; Oct: 17.0%).

- Net external reserves (-1.7%; Oct: -2.2%): smaller contraction steered by those of the banking system (-16.6%; Oct: -19.8%), reflecting increased liquidation of foreign assets.

- Claims on private sector (4.2%; Oct: 4.2%): sustained at amongst the lowest since 2003.

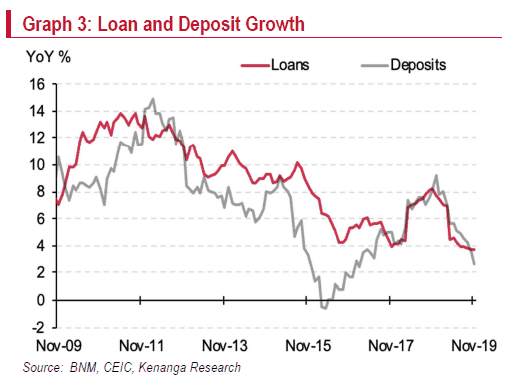

- Loan growth remained at a 16-year low (3.7%; Oct: 3.7%)

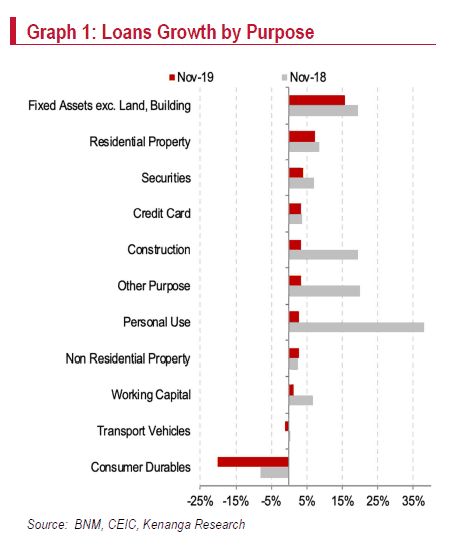

- By purpose: smaller contraction in loans for purchase of transport vehicles (-1.3%; Oct: -1.5%) amid improved car sales, equally outweighed slowdown in loans for purchase of securities (3.9%; Oct: 4.8%) and consumer durables (-20.1%; Oct: -19.3%).

- By sector: weaker credit growth in the construction (3.4%; Oct: 7.1%) and wholesale, retail trade, hotel & restaurant sectors (5.6%; Oct: 7.5%) equally offset improvement in the real estate (-1.3%; Oct: -3.5%) and transport, storage & communication sectors (5.2%; Oct: 2.2%).

- MoM: edged up by 0.4% amid lower average lending rate of commercial banks (4.73%; Oct: 4.76%).

- Deposit growth eased further to a 33-month low (2.6%; Oct: 3.5%)

- Weighed by lower growth in fixed deposits (4.0%; Oct: 5.3%) and Negotiable Instruments of Deposit (-9.1%; Oct: -2.6%).

- Deceleration in loan growth is expected to extend into 2020 (4.0%; 2019F: 4.2%; 2018: 7.7%)

- Cautious growth outlook retained, in spite of the phase-1 US-China trade deal, as the impact of existing tariffs would still weigh on global trade and growth in the immediate term.

- Given the soft growth momentum as evidenced by recent slew of weak domestic economic indicators, we reckon that the BNM may decide to slash the OPR by 25 basis points to 2.75% as soon as early 1Q20.

Signup for Rakuten Trade

Invest in Bursa shares or ETFs by opening a low cost brokerage account today!

Account opening link: RakutenTrade.my

Referral code: MYPF

Share with us your thoughts in the comments below.

{kind=link}

{kind=link}

Leave A Comment