As a licensed financial planner, I have been asked a number of investment questions over the years. What are the 5 most common yet often challenging questions on investment?

Contents

Common Question 1: Should I invest now or try to time the market due to X reason (i.e. Novel Coronavirus)?

No one can accurately predict what can happen next. Overall, more importantly than trying to time the market is your overall personal investment plan. This starts with your portfolio in a good asset allocation that is meant to be held throughout different economic conditions. This starts with investing based on your current funds available after allocating for emergency savings. Then, you will want to continue to grow your investments by investing regularly.

Over time your asset allocation will turn stale and no longer be as profitable, thus, you will want to rebalance regularly, typically every 6 months. This allows enough time for investments to gather some gains. While making sure that your overall asset allocation is not too far off that you are overly at risk with increased volatility.

Common Question 2: Should I invest a lump sum or stagger my investment?

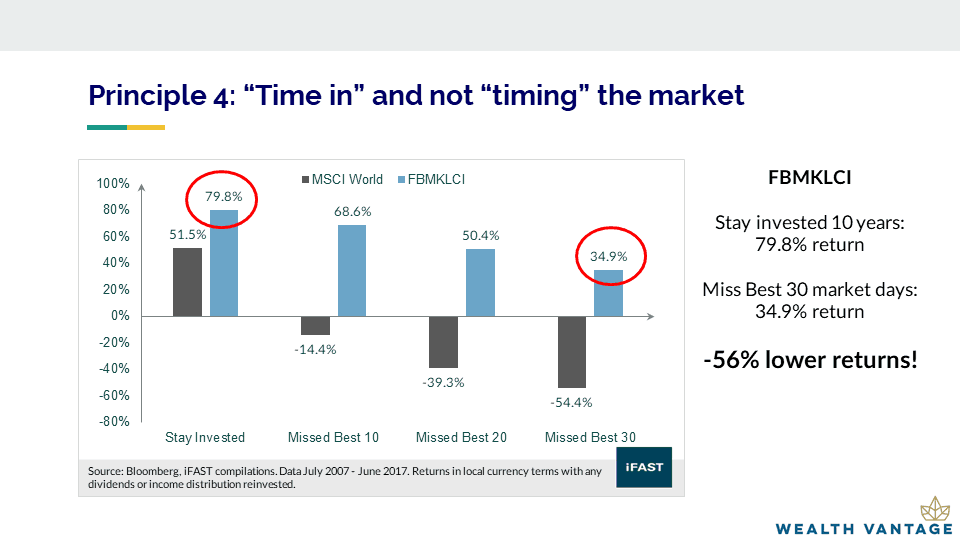

Investing with a lump sum rather than trying to time the market generates on average a 2-3% higher returns. In the longer scale of things it would make more sense to be invested rather than not.

If you miss out the best X number of days in investing you are risking out on a significant amount of returns:

- Miss best 10 days in market: -15% returns

- Miss best 20 days in market: -40% returns

- Miss best 30 days in market: -55% returns

(Source: iFAST and Wealth Vantage Advisory)

Common Question 3: Should I sell off my under-performing investment now or wait for it to recover?

Again, there is no crystal ball to determine where an investment will head next. Generally, if you are switching in the same asset class, the asset class that is generally down will likely also be lower cost when you switch into a similar asset class. If you are looking at a particular single investment you can choose to go through technical and/or fundamental analysis as part of the decision making process for disposing of an investment. This may help to minimize losses/maximize returns although in the larger scale and time of things it does not make that significant of a difference.

Cutting under-performing assets is important as you need to stick to your investment plan including when to exit under-performers. If you continue to hold on to under-performers, your capital is trapped within the particular investment and you are forgoing future income even if the investment just continues to stay stagnant. Selling off under-performing investments is also important for rebalancing your portfolio, if you need cash, and/or you simply acknowledging you made a wrong investment choice.

Common Question 4: Should I invest in X investment?

Asset allocation is responsible for 80% (or higher) of your total returns. Knowing what to buy and when to buy it, is responsible for less than 20% of the total returns. Most importantly is to not consider your investment in isolation but on overall holistic basis of how an investment fits into your overall investment plan.

With that said, you do need to perform due diligence on every investment.

- Do you understand the investment and how it works?

- Is the investment legal and approved by regulators?

- What are the fees and charges for the investment?

- What are the expected rate of returns after deducting fees?

- Are there any other better alternatives to the investment?

- How does the investment fit into your overall personal investment plan and asset allocation?

(Source: NovelInvestor and Wealth Vantage Advisory)

Common Question 5: Should I diversify into X investment?

Diversification is part of asset allocation but not just that. Asset allocation is dividing up your investments among different asset classes (e.g. equities, bonds, property, commodities). This allocation is decided in advance based on life goals and priorities, risk profile, age, and stage of life. Asset allocation is the one key factor that determines where an investor ends up. It’s one of the most important things to do and yet the one most investors neglect.

When investing on a regular schedule using dollar cost averaging in accordance with your asset allocation plan, you are diversifying over time. The fluctuations of the market work to increase your gains (not decrease them). To be a successful investor, you need to rebalance your asset allocation at regular intervals. You also need to rebalance within markets and within asset classes.

Diversification needs to be done purposefully and regularly for overall improved returns at reduced volatility and risk. But over diversification can work negatively by reducing your gains without necessarily reducing your risk while adding unnecessary complexity with too many investments to monitor.

You May Also Like

- The impact of Novel Coronavirus on financial markets

- What should you do with your investments in an economic slowdown

- How to diversify your investments

- Ten simple tips for investing

- How to select a financial planner

{kind=link}

{kind=link}

Leave A Comment