How to build and track a seven-figure investment portfolio. How to get started, diversify, rebalance, and manage your expectations.

Contents

Why Invest?

As in all things one does, there needs to be a why. Although it differs in the details, overall just about everyone wants to be able to live comfortably whether you call that retiring well or being at any stage of financial independence.

For me, one my 3 key life goals is achieving financial independence.

Financial independence is when all your ‘needs’ and ‘wants’ and covered by your investment/passive income. You’re at a stage that enables you to pursue any other goals, purpose or passions that you desire. A measurable goal is that your investment/passive income is at least twice (200%) of your expenses. You are fully free you to choose to not work if you so desire, to fire your boss, or to have your business run without you being involved daily. You can volunteer or work on a cause or purpose that you are passionate on without worrying about your pay.

Investing is also one of my key priorities in life coming in at number 6. Having a priority list helps me to focus and decide what to pay attention to.

My Priorities

- God – Daily unhurried time with God

- Spouse – Daily quiet time, pray together, conversations, dates, travel

- Self – Daily exercise, read & eat healthily

- Business – Financial planning clients, financial advisory business, MyPF site

- Church – Bible study, serving

- Investing – Asset allocation, investment selection

- Family – Immediate family, in-laws

- Friends – Social media, real-life

Investment Methodology

Having a personal investment plan is at the core of investing. Investing needs to be a well thought out process and planned in advance.

Asset Allocation

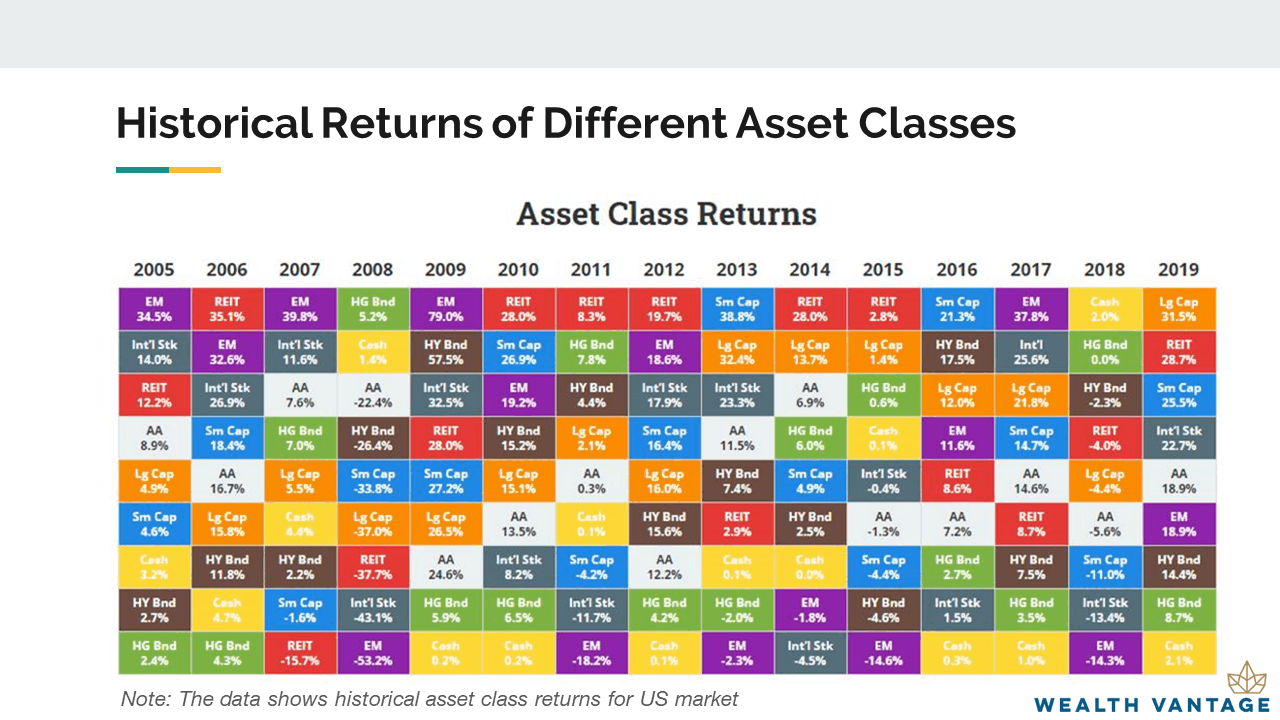

One of the most important determinants comes from deciding on asset allocation which accounts for ~90% of volatility and ~40% of returns. What is asset allocation? Asset allocation is to set how much of one’s investments goes into various asset categories to get the best balance between returns and reduced overall portfolio volatility.

Investment volatility measures the statistical dispersion of returns whereby the higher the volatility, the riskier the investment.

(Source: NovelInvestor and Wealth Vantage Advisory)

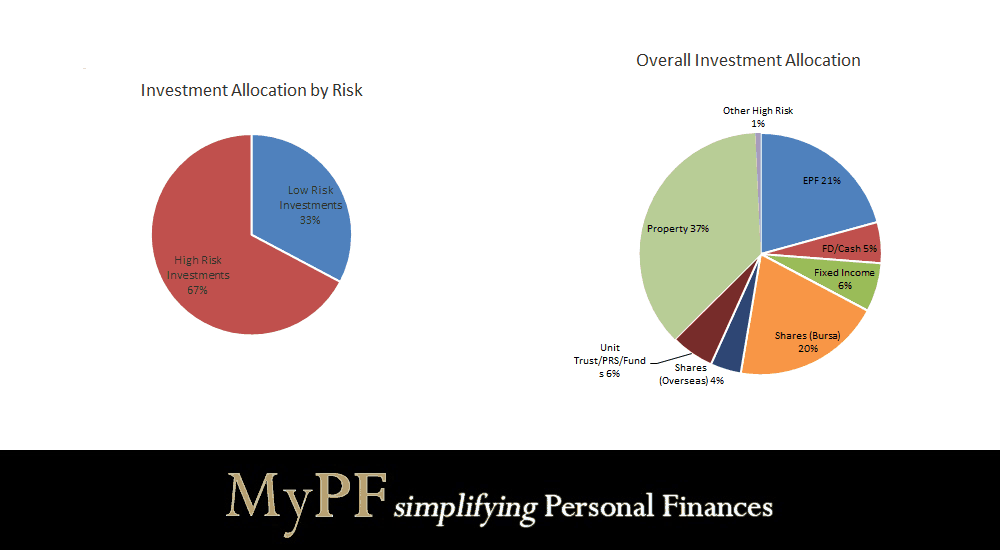

My Asset Allocation

My asset allocation is based on a 7-figure million dollar portfolio. Granted it does not start as such and is a measure of slowly building up your investments over a period of time and consistently reinvesting your returns. This is the reason why compounding interest is described as the 8th wonder of the world as compounding over time has your money working for you and growing at a rapid pace with time acting as your friend. My investment journey started more than 20 years ago while I was still in my teenage years squirreling away funds. Over time, I became increasingly aware of the importance of asset allocation, what are my investment options, and knowing how much investment risk I can take.

My Asset Allocation Current vs Goal

- Fixed Deposits/Cash: 7% vs 5%

- Fixed Income: 18% vs 25%

- Equities: 37% vs 50%

- Property: 38% vs 10%

- Other Investments: 1% vs 10%

- Overall Asset Allocation: 67% high risk vs 70% / 33% low risk vs 30%

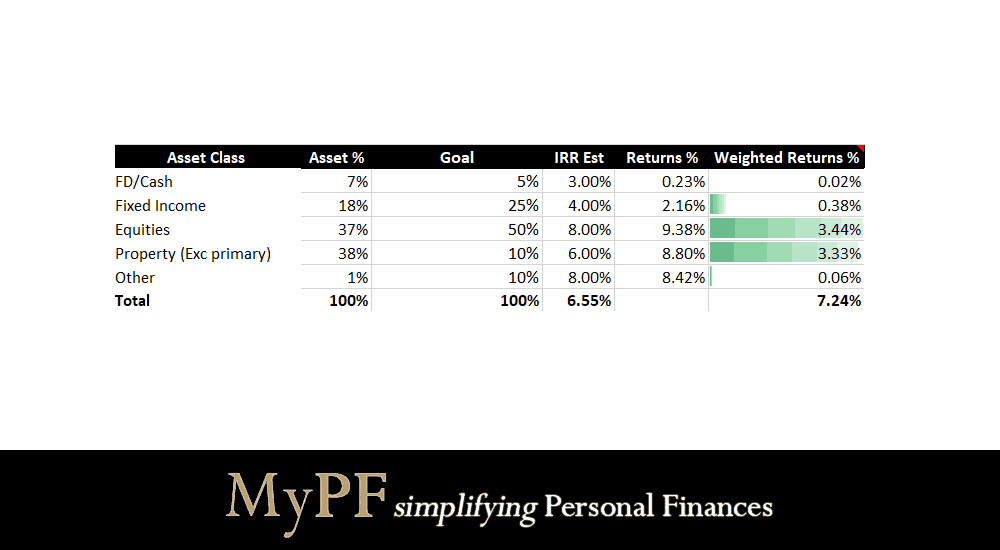

Investment Returns

Investment returns for the overall portfolio would correspond to the overall asset allocation. Different asset classes would also give you different expectations of investment returns. One can also estimate the overall returns of the entire portfolio based on your desired asset allocation.

My Investment Returns

- Fixed deposits/cash returns at 0.23% is below 3.00% goal. Primarily this is as I placed all fixed deposit/cash investments into new fund placements. If an investment is held for less than a year, the performance to date is taken for better accuracy. By year-end, the returns should be close to 3.00%.

- Fixed income investments at 2.16% are also below expectations of 4.00%. One area to look at this year is to increase both yields and exposure to bonds/bond funds.

- Equities is generating 9.38% overall above 8.00% returns goal. The highest performing equity investment has been overseas direct stocks which have a compounding return of 15.88% with the best performing being Visa Inc ($V) returning 95.68%. Funds (excluding EPF) have been returning 12.96%. While Bursa direct stocks have been lagging at 8.04% with the worst-performing being AirAsia Group Bhd ($AIRASIA) down 29.94%.

- Property has been generating 8.80% above 6.00% returns goal. This is considering rental income and property capital appreciation (excluding primary property and under construction property).

- Other investments have been generating 8.42% above 8.00% returns goal. Gold has been on an uptrend clocking in at 8.16%. While peer-to-peer (P2P) lending has generated returns at 8.40% as I switched to a lower risk exposure in view of default rates rising which worked out to reducing the defaults to nil.

- Overall investment weighted returns at a decent 7.24% above goal of 6.55%. Targeting to improve overall performance towards hitting 8.00% or better.

Next Steps

Making regular new investments and rebalancing existing investment regularly is required to make sure your entire investment asset allocation is still in place. Rebalancing is recommended once a year to allow time for performing investments to gain some profits.

My Investment Rebalancing and New Investments

- Fixed deposits/cash is slightly over allocated and to be reduced from 7% to 5%. I will likely reallocate some funds from FD/cash to fixed income funds.

- Fixed Income and Equities remain below the goal of 25% and 50% respectively. I have allocated new funds on a regular monthly savings plan to be invested into managed portfolios and digital wealth managers with a 70:30 allocation into equities and bonds. Direct shares equity investing also require some sector and stock rebalancing.

- Property remains significantly above allocation at 38% versus a goal of 10%. While not ideal, I am not planning to dispose of any other properties currently. I would expect the property % to naturally reduce as I continue to allocate more funds into other investment asset classes.

- Other investments goal was increased from 5% to 10% as I looked to further reduce the volatility of my overall investment portfolio. I am planning to further increase with both lump sum and regular investments into gold and other alternative investments. Another consideration is on whether any other non-gold commodities may be worthwhile diversifying into. Crypto is also a possible consideration as I had liquidated the majority of my position in early 2018.

- My next major rebalancing will be at the end of December 2020 as I choose to time rebalancing at the end of every calendar year for ease of remembering when to rebalance.

How to Get Started

Investing is not easy but it is simple to get started. Below is a flow to get started.

- Before Starting: Get your emergency savings, and cash flow in order. Set out your budget especially on allocations for investment for the year.

- Know Yourself: List down all your assets and liabilities. Determine your asset allocation goal, expectations, and entry/exit strategy based on your investment risk profile and age.

- Know Your Investment Choices: Gain knowledge on both the current investment asset classes you are currently holding and new asset classes you are keen to explore. Know what are your choices within each asset class and select the best vehicle that meets your needs.

- Invest Regularly: Start with your current cash assets on hand that are sitting idle. Invest and allocate your current funds to be placed into your targeted investment asset classes. Automate your regular monthly investing following your ideal asset allocation.

- Monitor and Rebalance: Over a period of time and depending on the economic condition, different investments would have performed differently. Some may have done well while others may have performed poorly during a period. Once a year do work on rebalancing your portfolio based on your asset allocation. This is true whether your portfolio size is RM10k, RM100k, or RM1m above.

“The best investment you can make is an investment in yourself. The more you learn, the more you’ll earn.”

You May Also Like

- My Personal Finance Independence Portfolio Updated 2020 July

- The 7 stages of financial independence for Malaysians

- Compounding to a million ringgit

- Investing in an economic slowdown

- Equites and shares investing guide

- Fixed income investing guide

- Alternative investing guide

Share and discuss on investing and asset allocation

Talk to a licensed financial planner to walk alongside you on your investment journey towards your financial independence goals!

{kind=link}

{kind=link}

Leave A Comment