Feeling overwhelmed by your finances and would rather leave it to your spouse? How do you take charge on your own financial needs?

Based on recent survey by UBS in 2019, most women do not plan their own financials. Most married women would instead leave the financial responsibilities to their men. Is it wise to do so? What are the implications in the future? What are the steps that women can take on this matter?

Contents

Low Level of Financial Literacy

Do you know that financial literacy rate in Malaysia is among the lowest globally? In 2016, the Organisation for Economic Cooperation and Development (OECD) reported that the level of financial literacy rate in Malaysia was below average and ranked 26th among 30 other participating countries.

According to statistics published by FENetwork, about 1 in 3 Malaysians admit to having low confidence when it comes to financial knowledge.

“Many Malaysians struggle to manage their money, making them highly vulnerable to the impact of a financial shock such as redundancy, long-term illness or even just a large unexpected bill.”

Tun Dr. Mahathir Mohamed’s message in the Malaysia National Strategy for Financial Literacy 2019-2023.

Growing sophistication of financial products and services accessed via digital channels have made financial literacy even more pertinent.

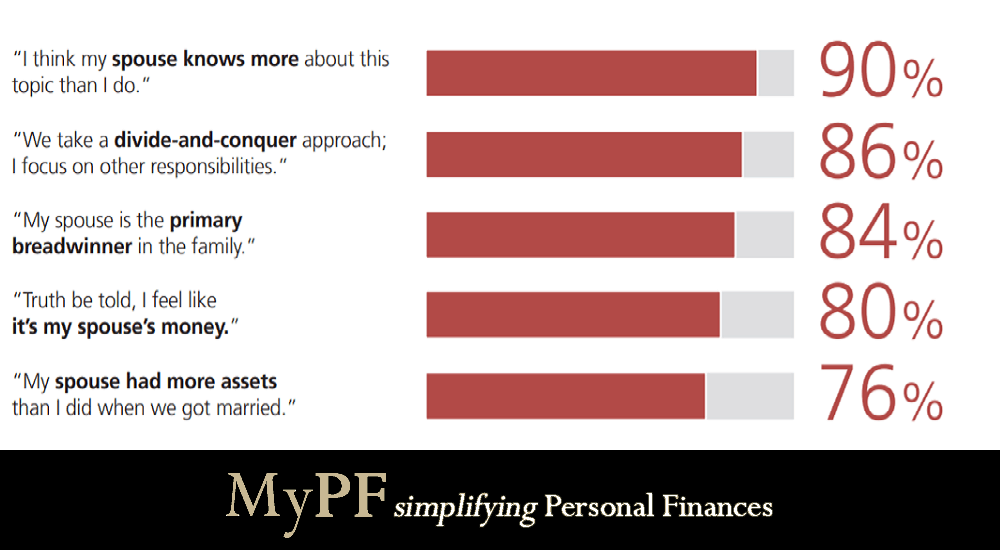

Leaving Major Financial Decisions to Spouse

Despite the low level of financial literacy in our country, most women are depending to their spouses to make major financial decisions.

According to a survey published in UBS Investor Watch, women decided to let their spouses to lead on major financial decisions because:

Nonetheless, can women afford to take a back seat on this matter?

In actual truth, no, women cannot afford to do so. Women have a life expectancy of about 5.1 years more compared to men; up to 77.3 years. In addition, 64% of women believes they will outlive their spouses. If women do outlive their spouses and have always relying to their spouses in making major financial decisions, how will their financial future be?

Leaving It to Circumstances

Men may be taking charge of the household’s finances. However, what if things did not go according to plan e.g. losing your job, premature death of the breadwinner, divorce happened? How can women take charge on the finances when they needed to, when they are not involved in the first place?

These are the most common financial consequences due to unfamiliarity of the subject matter:

1. Unaware of Financial Status/ Not knowing own or family financial status

Normally this is due to:

- No proper tracking of key data such as income, expenses, financial commitments;

- No proper record of assets owned, loans owed and the updated loans balances.

The truth is, many are unsure of what assets and liabilities are in their personal context. Let alone what are their net worth value.

Not knowing your current financial situation is a big blind spot as this is the first step in managing personal finances. It is very important for women to be aware of all these and the documents whereabouts, not only in their name but if possible, including under the spouse’s name.

We never know when a time may come when we have to handle all financial matters by ourselves. It is about survival, not only to women but those who are depending on them like minor children or aging parents.

It is better to know now rather than have to dig for information and handling coping with loss? It is better to be ready rather than to be sorry.

2. Readiness for unexpected life events

When we are not aware of our current financial situation, it is a sign that we are unaware of our financial exposure. In other words, how ready are we to respond to unexpected major life events such as premature death of the breadwinner. It is common to have financial commitments and debts. Common debts include property mortgage, credit card debt, car loan, personal loan and study loan.

You need to quantify whether your existing assets or existing insurance coverage are enough to cover these commitments when eventualities strike to your family. Do note that non-liquid assets which may takes longer to process as compared to your liquid assets. This is crucial because regardless whatever happened, it is always our wish that disruptions are at minimal level as possible.

To achieve this, you can begin with having a list of summary of your existing policies coverage for respective events such as death, total permanent disability (TPD) or Critical Illnesses (CI). Do include the coverage provided by your company, if there is such. It is also important to take note on the coverage period for each policy.

In the case that you are solely depending on your husband, it is critical to understand this as surviving wife, and assume the role as the backbone of the family.

Being Risk Averse

In general women are normally an averse risk taker. The above statistics show women tend to leave it to their spouse to decide on major financial decisions as women tend to take care more on household chores and work.

In addition, women usually earn lesser and start to invest later than men. As a result, this may lead to potential loss of opportunity to earn better returns and there is a risk of insufficient funding for post-retirement period. This issue is crucial knowing the fact women live longer than man.

Therefore, a basic understanding on your risk tolerance, investment decision, and investment options are essential information that every woman need to have.

1. Splurging Your Income

At early stages of working life, many tend to delay the habit of saving. Most reasons are given such as insufficient salary or that will start saving later when one’s salary is higher. However, in real life many people tend to increase lifestyle spending when they get a salary increment or promotion.

There are also women who spends their salary only for their own and the kids, as the spouse will take care of other financial matters. As the purchasing power is more, they tend to overlook on the importance of savings. This has led to a very risky situation whereby you need to adjust your lifestyle if you are unprepared to the unforeseen circumstances which is not easy to deal with. Also as a parent, you are setting a precedent of lifestyle spending for your children.

The right way is to start saving early. No matter how small the amount, it is easier and beneficial to kick-start the saving habit compared to delaying. Consistent small saving can grow to become substantial over a period of time.

2. Unaware of administrative procedures and related cost when death happened

Today’s life arrangements are more complicated than during our parents or grandparents time. For example, it is becoming more common to find both husband and wife taking joint long-term debt commitments together but the asset (i.e. property) is only under one spouse’s name.

Many people do not know how to start estate administration procedure. Where to go, who can advise and what are the associated costs are some of the questions that come up. Inefficiency can be very costly to deal with. Being unprepared, beneficiaries are expected to deal with a lengthy process and in some cases dealing with disputes among beneficiaries.

Proper estate planning while you are alive will enable your beneficiaries to expedite the process and manage associated costs better. Thus, your hard-earned money can reach your beneficiaries as per your intended wishes rather than being frozen. This is of upmost important especially when you have minor children or are depending on a single income earner.

Taking Charge

Women tend to be the most severely affected because of unfamiliarity of their personal finances. It is essential that women take an active interest and more involved in planning their finances.

1. We have various life priorities but very limited financial resources.

It is important to note that cash flows management is the heart of managing your personal finances. Elements of budgeting, keeping track spending and differentiate “needs vs. wants” are among the key essentials. Women may also spend more on luxury products such as handbags, clothes and beauty products.

2. Aligning your needs with resources

Everyone’s financial needs and commitment change at different phases of life. Most people tend to enjoy during earlier phases of working life. However, it is important to realise that there will be peak time throughout that lifeline where one’s expenses are at the max. One’s ability to anticipate and be prepared of this will help not only to manage the situation but reduce stress.

3. Beating inflation

Over the time we notice things just get more expensive. A piece of roti canai today priced more then what it was 5 or 10 years ago. In other word we call this inflation. But the next question is what do we do to ensure our money work harder and can beat inflation? In many cases majority women only look at salary raise or promotion instead of to equip self with relevant investment knowledge.

All women should have this goal regardless of your marital or work status. It would be even better if this goal can be set together with your spouse or family members.

The ultimate key point for women is to improve on financial literacy. This is the best investment for yourself. Know own current financial situation and start to initiate own financial goals are also important. You can read Next 6 Steps for Setting Your Financial Goals in setting up goals.

Additionally, you may seek professional advice for example, a Licensed Financial Planner can help you on this. It is very important to choose a good, qualified licensed planner, who will help you to improve your knowledge and explain the suitable unbiased recommendation to you.

A Value Addition to the Family

Each one of us are responsible to our own financials. You matter, equally as important as your financials. Thus, take heed and act upon your financials now for a better promising future for you and your loved ones. As Arese Ugwu quoted,

“A woman becoming financially independent does not equate to ‘I don’t need a man’. It just means she brings more to the table. Instead of being a financial burden, she becomes a value addition. Her success does not take away from his success. The pie they share just becomes bigger.”

Own your worth. Take control of your financial well-being. Live a peaceful and comfortable life now and for the future.

Sources:

- UBS Investor Watch, Singapore Insights, 2019 Volume 1

- Malaysia National Strategy for Financial Literacy, 2019-2023

- Abridged Life Tables, Malaysia, 2017-2019

- Smart Money Arese – The Smart Money Woman

Helwa and Fateen both previously working in oil & gas industry before decided to leave the workforce and pursuing a career as Licensed Financial Planner with WVA.

They believe it’s about managing own expectations and emotions. Having the confidence and capability to manage own finances are essential life attributes to attain and sustain a good quality of life for women.

You May Also Like

- The Importance of Financial Education

- How To Craft Your Personal Financial Plan With Your Financial Advisor

- Women: Entrepreneurship, Leadership, and Success

So what do you think about this? Do share with us your comments in section below.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment