Employees’ EPF contribution will be reduced from 11% to 7% from April 1 to December 31, 2020 as part of stimulus package. Will you opt out?

Contents

EPF Employee Contribution Reduction

- Announcement date: February 27, 2020

- Change: Reduced minimum statutory contribution rate for employees from 11% reduced to 7%

- Why: Part of Malaysian Government’s economic stimulus package intended to cushion the blow from the economic fallout following the global COVID-19 outbreak

- Effective date: April 1, 2020 – Dec 31, 2020

- For employees age 60 and above: no change (remain at 0%)

- Employer responsibility: ensure the correct amount is deducted from their employees’ wage/salaries based on the Third Schedule, Akta KWSP 1991

- Employee option: reduced contribution to 7% (automatic) or choose to maintain current contribution rate of 11 per cent by completing Notis Pilihan Mencarum Melebihi Kadar Berkanun KWSP 17A (Khas)

Download

Notis Pilihan Mencarum Melebihi Kadar Berkanun KWSP 17A (Khas) (kwsp.gov.my)

How to submit: Notice must be presented to employers to be submitted to EPF.

More info

- EPF website at kwsp.gov.my

- Call EPF Contact Management Centre at 03-8922 6000

- Visit any EPF branch

EPF Lowered Contribution Opting In or Out

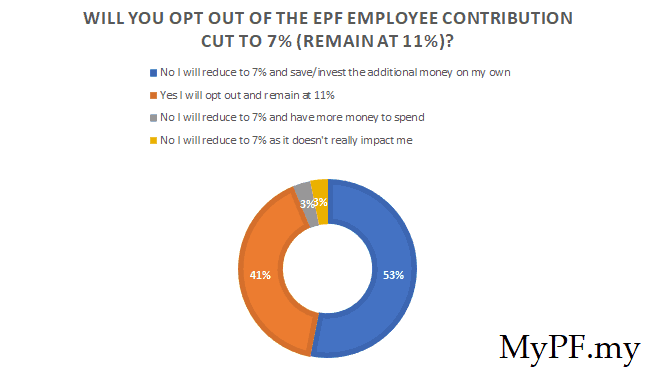

Poll results of the My Personal Finances Facebook group show the majority of contributors are ok with the cut but will save/invest the additional money on their own. Below are the results:

Q: Will you opt out of the EPF employee contribution cut to 7% (remain at 11%)?

- 53%: No I will reduce to 7% and save/invest the additional money on my own

- 41%: Yes I will opt out and remain at 11%

- 3%: No I will reduce to 7% and have more money to spend

- 3%: No I will reduce to 7% as it doesn’t really impact me

What factors should I consider whether I cut my EPF contribution rate to 7%?

- Maximising EPF Tax Relief: for YA 2020 (Year of Assessment), the maximum EPF tax relief is RM4,000 and is in a separate category (previously combined with Life Insurance). To max out the tax relief of RM4,000 in 2020 at employee contribution 11% Jan-Mar and 7% Apr-Dec your monthly gross income needs to be RM4,166 monthly (RM50,000 annually). TLDR: If your monthly income is below RM4,166, you should keep your EPF employee deduction at 11%.

- Maximise Other Tax Relief: for YA 2020 if you have not maxed out the tax relief, you can use the additional monthly cashflow for additional tax relief. Some common examples for tax relief include PRS (max RM3,000), life insurance (max RM3,000), and SSPN-i (max RM8,000).

- Investments with Higher Returns: If you have access to investments with potentially better returns than EPF returns, you can consider investing in these instruments. Besides potentially higher returns, you also gain the benefit of extra liquidity in those investments.

- Clearing off High Interests Rate Debt: If you have debt with high interest rate (e.g. above 6% per annum interest rate charged), you can use the additional money to pay off debt.

Overall, if you have a plan on how to wisely use the additional cashflow from the reduced EPF employee deduction you can proceed as such. However, do avoid lifestyle creep whereby you end up spending more with the temporary additional cashflow money. Don’t get overly used to the additional cashflow as the reduced EPF employee deduction rate as it is temporary.

You May Also Like

Share and discuss on whether you would opt for EPF employee deduction of 11% or 7%.

{kind=link}

{kind=link}

Leave A Comment