Sharing my thoughts on investing and asset allocation, and the details of my investment portfolio towards building the best investment portfolio I can. Learn how to start an investment portfolio and the 5 types of investment assets.

Contents

Financial Independence

My definition of Financial Independence

I define Financial Independence as passive income (or semi-passive income such as rentals) generating you twice or 200% your expenses. Interestingly in the last 30 days, this topic came up numerous times in chats with a professional fund manager cum multi-millionaire, interviews on MyPF PodCat, the book publisher of the upcoming MyPF book, and my fellow licensed financial planners.

Financial Independence = Passive Income > 2x Expenses

Financial Independence is a journey and not quite the end goal and there’s even a stage after FI. It starts for just about everyone from financial dependence to debt freedom to financial independence and lastly financial abundance.

- Stage 0: Financial Dependence

- Stage 1: Financial Solvency

- Stage 2: Financial Stability

- Stage 3: Debt Freedom

- Stage 4: Financial Security

- Stage 5: Financial Freedom

- Stage 6: Financial Independence

- Stage 7: Financial Abundance

Tip: Watch the following video or read this article for more info on the 7 stages of financial independence

My thoughts on FIRE (Financially Independent, Retire Early)

Financial Independence is a goal that we can all strive for. And for many people, it’s something you can achieve in as short as 10 years with a very disciplined approach. Not everyone wants to retire early though with retirement being a relatively new concept (over the last century). Prior to that and the effects of the industrial revolution, people basically worked their entire lives until they could no longer work.

Early retirement may not be for everyone. Sure it is nice at first to spend time on the beach on in the garden totally at leisure. But that will get old (and you yourself too) pretty fast. Life requires meaning, passion and stimulation. So throw away the image of margaritas everyday on a sun-kissed beach. Early “retirement” is good when it allows you to focus your time and energy on who and what matters to you without having to worry (much) about any financial concerns.

A final concern on financial independence, retire early (FIRE) is having the bare minimum needed to survive with any potential expenses increases or a significant drop in your investment portfolio forcing one to return back to work. For brevity, we will cover the different types of FIRE and details of pros/cons in a future article.

Investment Portfolio

My Investment Asset Allocation

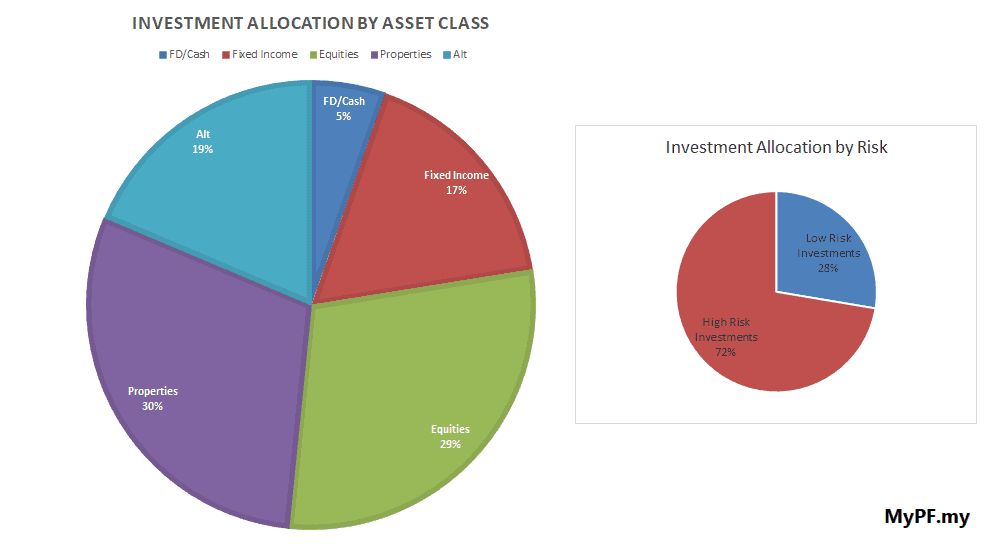

5 Key Asset Allocations (Current vs Goal)

- Fixed Deposits/Cash/Cash equivalents: 5% vs 5% goal

- Fixed Income/Bonds: 17% vs 25% goal

- Equities: 29% vs 50% goal

- Properties: 30% vs 10% goal

- Alternate Investments: 19% vs 10% goal

- Overall Asset Risk Allocation: 72% high risk vs 70% / 27% low risk vs 30%

Recent Portfolio Changes

- Fixed Deposits/Cash/Cash equivalents: total amount remained the same but moved funds from fixed deposits/high yield savings accounts in view of the OPR cuts into an income portfolio.

- Fixed Income/Bonds: overall more funds placed into bond funds through various managed portfolios. A possibility is to consider direct bonds but am not quite convinced it’s worth the additional time and effort for my portfolio needs (even though I have access to bond research tools, insights and reports). A quick summary of Bond Funds vs Bonds:

- Bond funds allow for a diversified selection of bonds, reduces default risks and have overall better liquidity.

- Bonds allow for interest rates at the coupon rate if held to maturity thus (arguably) reducing the risk of interest rate changes.

- Equities: overall continued to increase exposure also via managed portfolios which have been reducing USD-backed asset exposure, increasing weightage to China, and asset allocation wise into sectors that are expected to do well in our new normal (e.g. technology, healthcare, staples). Have not been picking up much individual stocks (both locally and internationally) as finding the valuation price to actual earnings report increasingly widening.

- Properties: still having an overly high allocation to property due to previous legacy property and re-designation of a residential property to an investment property. Still not seriously considering any further disposals but will continue to reduce asset allocation by increasing investments in other asset allocations. (Side note: is pretty tempting to consider some REITs though while going through REITs analysis for clients).

- Alternate Investments: eagle-eyed readers will notice a sharp increase compared to the last portfolio update from end January. The key reason would be a decision to include private equity into the alternate investment asset allocation bucket. I also placed a small amount into crypto and will detail that below.

- Overall Asset Risk Allocation: a broad based high vs low risk allocation still falls within a +/- 5% tolerance level.

My Investment Performance

Investment Performance Review by Asset Class

- FD/Cash: 2.69% outperforming 2.00% goal despite the rate cuts due to the outperformance of income portfolio setup.

- Fixed Income: 4.75% slightly underperforming 5.00% goal due to endowments underperforming but pulled up bond funds.

- Equities: 13.82% outperforming 8.00% goal having recovered since the March 2020 pandemic lows.

- Properties: 8.80% outperforming 6.00% goal enjoying uninterrupted rental income (despite the pandemic) with REITs being a minor contributor.

- Alternate Investments: 14.04% outperforming 10.00% goal enjoying a recent bump with alternate investments gaining traction amidst heightened market uncertainties.

Investment Highlights/Selected Detailed Performance

- Income portfolio: 1.43% returns since funded in 2020 May. Annualised return of portfolio (XIRR) projected at 6.60% in line with my expectations of 4% to 6% returns.

- Managed portfolio: compounding annual growth rate (CAGR) of 8.89% slightly above expectations of 8% with a moderately aggressive investment risk profile.

- Robo advisory: CAGR of 7.15% slightly below expectations of 8% with a balanced (17% risk index) profile. (Money weighted return of 37%; Time weighted return of 25%)

- Shares (US and global): CAGR of 13.21% in line with expectations of 12%-15% returns with highest returns primarily from tech sector.

- Shares (Bursa): CAGR of 24.53% above expectations of 12%-15% returns primarily from selected stocks added to portfolio during the market downturn.

- Gold: CAGR of 18.45% with gold recently at an all time high in response to being perceived as a safe havens during times of economic uncertainty.

- Bitcoin: 16.13% with a recent investment in March (having previously exited major crypto positions in 2018 January) prior to the halving in 2020 May and also with the recent end July rally.

2020 Investment Performance Review Over Time

- In 2020 February, the portfolio saw a significant dip with the lowest point being in March primarily due to the dip in equities (affecting direct stocks, managed portfolios, and robo advisory). The crash was significantly cushioned by having weightage in bonds, properties and alternate asset classes.

- In 2020 April to May, the portfolio continued to recover taking advantage of regular investments into equities and bonds. By end May, the portfolio had already regained back its losses and making gains. Gold, crypto and P2P funding as alternate investment assets also contributed to overall portfolio performance growth.

- Overall the portfolio is generating 10.22% as of 2020 July end which is above the risk profile asset allocation adjusted return of 6.95% and my own personal investment portfolio returns goal of 10.00%.

2020 2H Investment Plan

There are 5 more months from August to December 2020 and a broad outline of plans as follows:

- Regular monthly investments into equities and bonds via managed portfolios and robo advisory will continue on as planned and form the bulk of investment cashflow allocation.

- Property rental income continue to pay for my property loans interest while will be looking for tenant for new properties completed.

- Although gold prices touched a high, the overall long-term trend appears intact and will continue dollar cost averaging into gold. May move gold out to a lower cost investment vehicle either in late 2020 or in 2021.

- Also in late 2020 and likely in 2021 will be looking to pickup more direct shares both locally and globally.

- Other annual investment goals pending include 3k into PRS and 8k into SSPN-i for tax relief.

Disclaimer and note: I am a licensed financial planner and the majority of these investments are done through my own financial advisory firm and/or partners we work with. The fees I am paying though are virtually the same as what my financial planning clients would be paying (which for a majority of investments e.g. income portfolio, managed portfolio, PRS are basically a 0% sales charge). This article is for financial education purposes only, is my own personal portfolio and opinions, and is not investment advice. Please talk to a licensed financial planner (and pay him/her for services rendered).

Other Financial Bloggers Investment Portfolios

Sorted according to how long have known them to share their investment portfolios publicly.

DividendMagic.com.my

(Source: dividendmagic.com.my)

Divvy’s Freedom Fund is like his namesake very focused on dividend stocks and REITs with ~RM500k market value. This CFP (cert tm) holder shares quite a few values (and stocks) in common when it comes to stock picking. As of 2020, he has also ventured beyond Bursa into US equities. (He also has a property portfolio).

Pending: We are still waiting for Divvy’s schedule to clear up for him to appear on our podcast as promised! Am still debating whether putting on Iron Man to hide his identity is safe enough for a live podcast recording or whether we should play it safe and record in private.

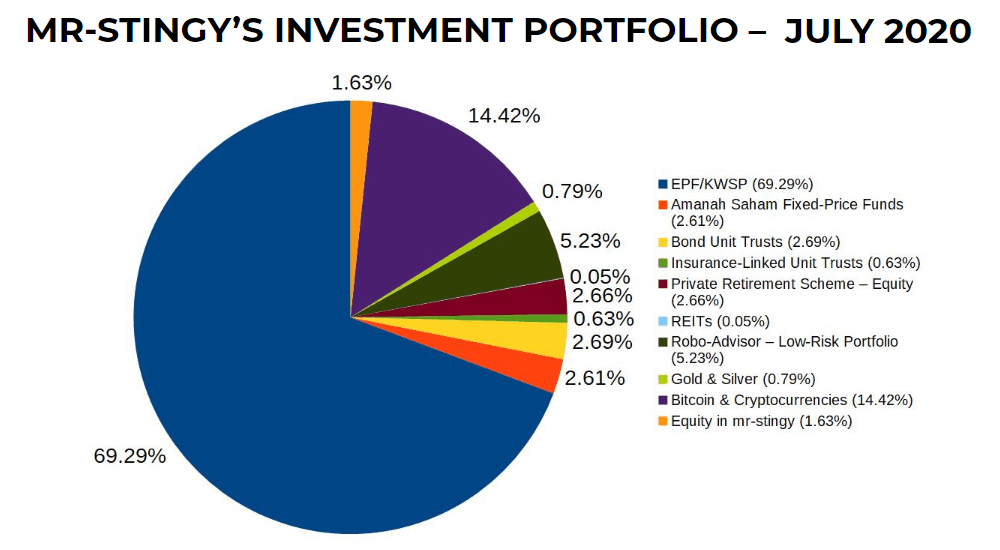

Aaron from www.mr-stingy.com

(Source: mr-stingy.com)

mr-stingy is big on the “safe stuff” as he puts it with 80% of his portfolio keeping him warm and fuzzy while the other 20% into “high risk-high return stuff” including a whopping 15% into crypto! (Disclaimer on his behalf: he works for a major crypto exchange). He expressed interest in engaging a financial planner so will we see upcoming changes to his investment portfolio ahead? I’m excited to find out!

Fun fact: One of the reasons I added private equity as part of my portfolio holdings is the reminder from his portfolio where he lists his equity in mr-stingy.

Bonus: We recently had a MyPF PodCat video podcast with mr-stingy where he talks about his investment portfolio too. Click here to watch and don’t forget to subscribe to our MyPF Digital YouTube channel!

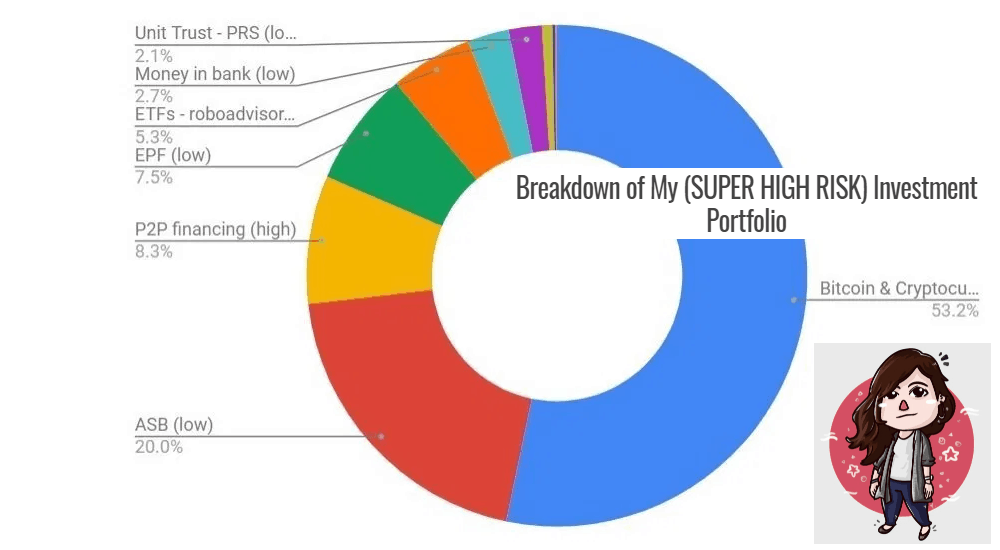

Suraya from RinggitOhRinggit.com

(Source: ringgitohringgit.com)

Suraya, WHY IS YOUR RISK SO DAMN HIGH? Well she answers that in her investment portfolio post on how crypto ends up being 50% of her portfolio. Well, she’s happy with her net worth and sleeps well at night which is more than many investors can say.

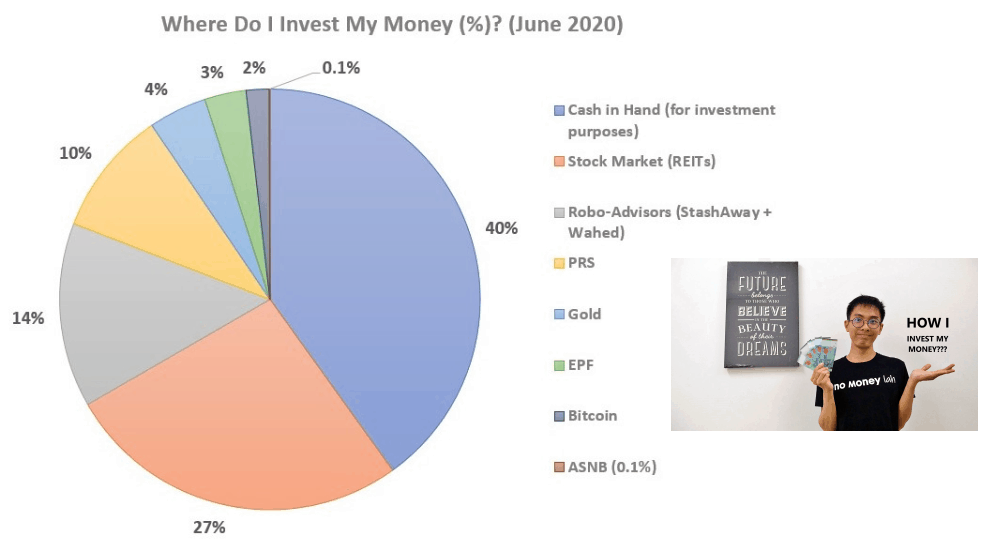

Yi Xuan from NoMoneyLah.com

(Source: nomoneylah.com)

Young, self-employed and a trader! Yi Xuan shares his thoughts on his investment portfolio including his large position (40%!) in cash and his love for REITs. Also good stuff as he shares his investment mindset approaches.

Notes: We have compared notes for REITs investing and our approaches are similar in many ways. Also do note his investment portfolio excludes his trading funds (trading != investing) and emergency savings.

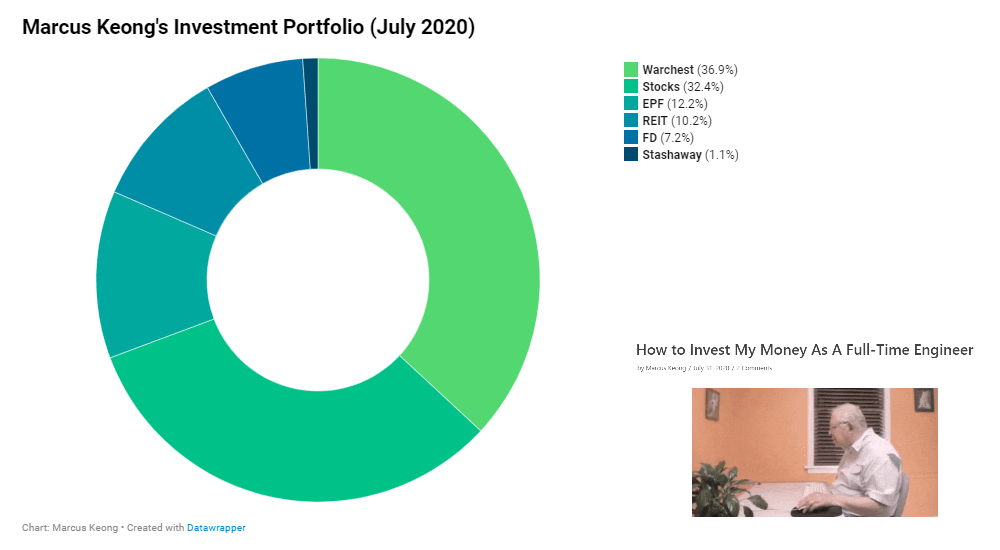

MarcusKeong.com

(Source: marcuskeong.com)

Marcus is a (30 years young and not an old man) engineer who loves donuts. Now whaddaheck is a warchest?! He’s holding close to 40% in cash for investments (hmm is this starting to sound familiar). As you can see, he’s very into stocks and REITs. He also shares his ideal portfolio and touches on why he is / isn’t investing in gold and crypto.

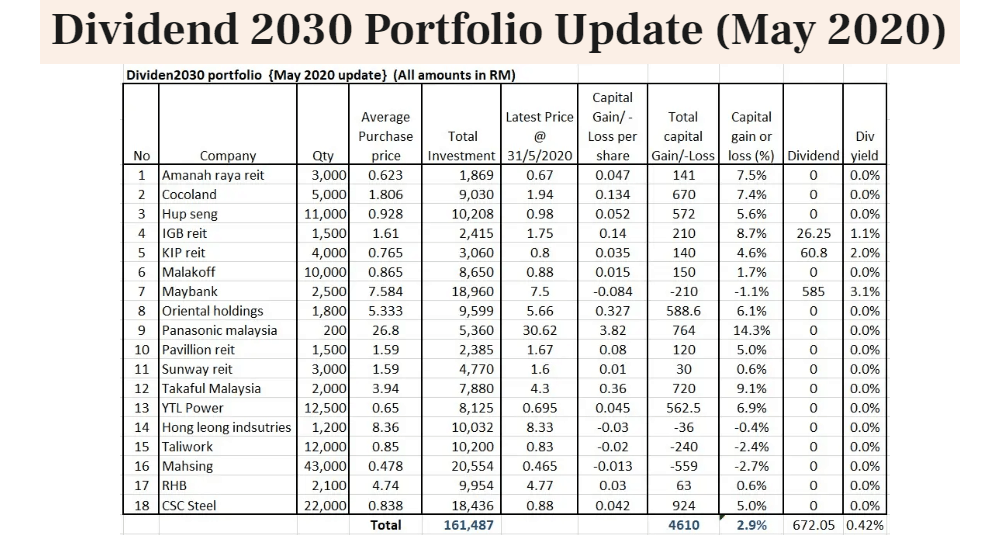

Sivasathish.com

(Source: sivasathish.com)

Siva is planning to update monthly on his investment portfolio with the portfolio above showing his stocks investments. He’s embarking on his 10 year investment journey (which explains the Dividend 2030 title) and sharing details of his journey with us. It’s a nice touch too that he shares about missed investment opportunities as well. (No FOMO!)

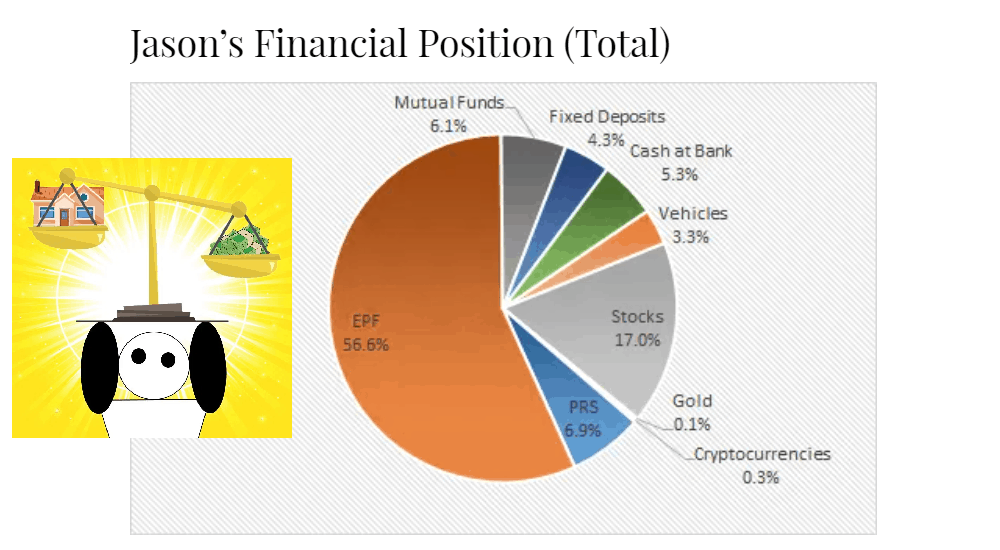

Jason from BetweenTheMoney.com

(Source: betweenthemoney.com)

Jason (who’s in his early 30s) starts right off the bat talking about rebalancing and having a plan. He’s the man!

Like many of us, he has a love of equities and it’s interesting to see him talk about the upcoming planned adjustments to his portfolio in the year ahead.

Ps. Aren’t the rounded stickmen adowable?

Bonus: Jason has nicely included a downloadable financial position template (investments, balance sheet).

Are there any other financial bloggers with public investment portfolios shared? Do let us know in a comment below so we can feature them (or you)!

FAQ

Q: How do I start building my investment portfolio?

A: You don’t need a lot of money to start building your investment portfolio. You can start with lower risk asset classes and/or investments that you are the most familiar with. Advancements in financial technology now allow you to start investing from as low as RM1,000 (and there are also options to start from as low as RM100). Start small and keep investing regularly.

Q: Should I record EPF as part of my investment portfolio? If yes how do I do so?

A: Yes, EPF is part of your investments for your old age so it should be recorded. EPF as its full name Employees’ Provident Fund suggests is a fund itself. Suggested you can break down EPF into its individual asset allocation which is as follows or show your EPF as a single asset class.

EPF latest Strategic Asset Allocation (SAA) as of 2020 Q1:

- Fixed Income Instruments: 54%

- Equities: 36%

- Real Estate and Infrastructure: 6%

- Money Market Instruments: 4%

Q: How do I rebalance my investment portfolio?

A: If you already have existing investments, you may want to look at what is your ideal investment portfolio. For many Malaysians, you end up having a rojak (mixed) “portfolio” consisting of various investments that you heard/read about or were recommended by an agent/friend/relative. A better approach would be to take some time to draw up your personal investment plan detailing your ideal investment portfolio. Once that is done, you can start taking immediate action to rebalance your portfolio by buying/selling any investments towards your ideal investment portfolio. Finally, you should look to allocate you future monthly cashflow/savings into investments following your personal investment plan.

Q: How do I diversify my investment portfolio?

A: Diversify between different asset classes, sectors, countries, companies/funds, and time! (Read more here.)

Q: What are managed portfolios in investing?

A: These managed portfolios are investment portfolios which can consist of multiple individual investments or funds which may include unit trusts, ETFs, index funds, shares, bonds, money market funds, etc. These are mostly discretionary portfolios which means investment decisions are made by the portfolio manager or investment manager. The portfolio manager may be digital (i.e. robo advisory) and/or human (i.e. portfolio management team).

Q: How do I learn more about building my investment portfolio, my ideal asset allocation, and investment options?

A: You are on to a good start with articles like this! MyPF has a wealth of free financial resources available including on asset allocation and investing. To build your investment portfolio you can take a DIY approach, work with a financial planner, or a blended approach using a mix of making your own investment decisions with the counsel of your own financial planner working in your best interests. Get a free 15-day MyPF Premier trial including the asset allocation spreadsheet seen above and a free consultation with a licensed financial planner using my link here.

You May Also Like

- Building a million ringgit portfolio (my portfolio snapshot from the start of the year in January 2020)

- How to build a diversified portfolio (diversify, diversify, diversify ad nauseam)

- 3 red flags in your investment portfolio (Tony Robbins, yes that Tony Robbins, chips in with some red flags to watch out for)

{kind=link}

{kind=link}

Very good article! Would like to share to my contacts as well.

HI just to clarify ,

When you describe Fixed Income/Bonds and Equities for your own portfolios. Are you dividing your own EPF into these categories ?.

For layman like me, what do u mean by fixed income and equities ? are you talking about your shares or you directly invest on bonds/equities or robo advisors ?

just need some clarification in this matter.

For general audience, asset categories are (cash, properties, share which includes REITS as well, unit trust/mutual funds (which they invest in bonds/equites/fixed income) , crypto , robo advisors.

So when you use terms like fixed income/bonds/equities individually, it makes me wonder which one are you talking about ?