In the latest BNM report, the equivalent value of 70% of pre-moratorium loan repayments have been made since the full moratorium ended in 2020 September.

Contents

Latest Post-Moratorium Stats

Since the end of the blanket loan moratorium period on 2020 September, the latest data has been released by Bank Negara Malaysia (BNM).

- Total value of loan repayments: 70% of pre-moratorium numbers

- 2 million borrowers contacted by respective banks and financial institutions

- 514,000 borrowers in process of rescheduling and restructuring (R&R) application

- 98% approval rate for R&R

- 15% or less of total borrowers estimated to be experiencing negative financial margins

- 1% of total borrowers are estimated to default

“The targeted repayment assistance measure is needed for individuals or businesses who may still face challenges for them to have temporary relief. This can help to improve the visibility of loan performance of banks to encourage economic recovery.” ~Jessica Chew, BNM deputy governor

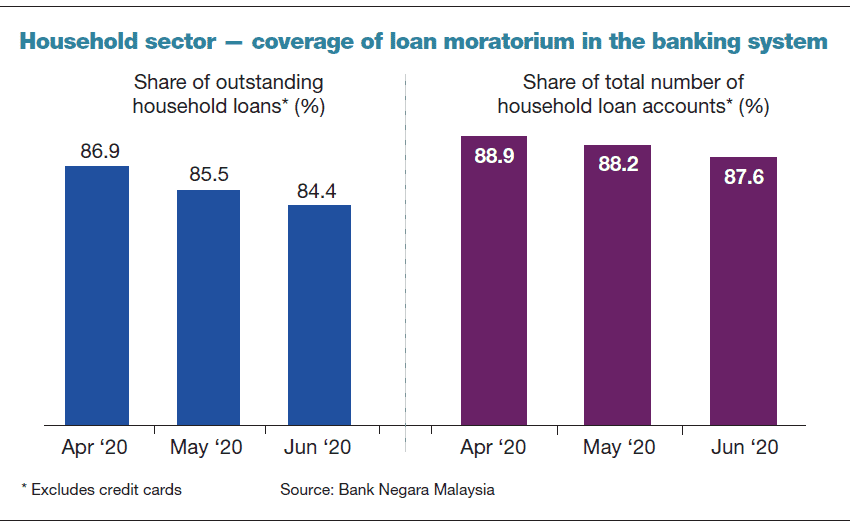

Household Sector – Coverage of Loan Moratorium in the Banking System (Source: BNM)

Post-Moratorium Recovery

BNM in their 1H 2020 report emphasized that many borrowers who opted out from the loan moratorium are those with an income of above RM5,000 per month with larger loan sizes. While household debt including floating rates hovering around 70%, debt serviceability is supported by lower monthly debt obligations following the overnight policy rate (OPR) cuts to the lowest levels this year.

“With the automatic moratorium in place, aggregate impairment and delinquency ratios remained low at 1% and 0.9% of total outstanding household debt respectively (2019: 1.2% and 1.1%). Household asset quality is expected to see some deterioration in 2H20 and throughout 2021 with the automatic moratorium ended, but banks are well-positioned to absorb higher credit losses.” ~BNM 1H 2020 Report

The moratorium has helped Malaysian households to survive the first and second waves of the pandemic especially for those who lose their jobs and faced declining income. Many borrowers are starting to pay their loans as their source income are starting to recover.

Impairment Expected to Rise in 2021

According to BNM in its latest Financial Stability Review, higher household impairments in the second half of 2021 are predicted due to extended repayment assistance programs for individuals with income affected in the first quarter of 2021. The stress test counted the effect from the loan moratorium in April and repayment assistance for targeted individuals.

The impairments can increase to more than 4% by end of next year due to drastic economic and financial changes caused by the pandemic, based on a macro stress test done by BNM.

Businesses are also affected by the impairments due to the defaults of maturing bullet repayments of firms operating in vulnerable sectors especially in the services industry that might recover slower compared to others and exposure to several large borrower groups that have weak financials.

Conclusion

Many borrowers are starting to pay back their loans after the full loan moratorium ended in September while those who have income significantly affected have already applied for extensions. However, as the government is enforcing another Conditional Movement Control Order (CMCO) in parts of our country, there are more people considering looking for targeted moratorium or other relief to help with their finances during these difficult times.

You May Also Like

- Malaysia’s Government Announces Targeted Loan Moratorium Extension

- Additional Charges Waived for Hire Purchase Loans Moratorium

- 5 Tips on Giving Personal Loans to Family or Friends

- Will the Malaysian Property Market Drop after the Loan Moratorium Ends?

Is the targeted loan moratorium assistance helpful? Share with us in the comments section below.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment