Gain insight on how Malaysians can maximise your tax relief and tax rebates for year of assessment 2020 for filing in 2021. Don’t risk losing out on your tax ringgit savings!

Contents

2020 Income for Malaysian Resident Individuals

Gains from Business

- Gains or profits from carrying on a business, trade, vocation, or profession including sole proprietorship/self employed, partnership, and any business venture of two or more individuals combining ownership, authority, work force or skill in running a business.

- Cash receipts from sale of goods or from services provided.

- All debts incurred from sale of goods and services provided.

- Receipts in kind.

- Recovery of bad debts.

- Insurance compensation received for business loss.

- Withdrawal of business stock or stock taken for personal use.

Gains from Employment

- Employee salary, remuneration, fixed allowances, benefits-in-kind, perquisites, tips, compensation for loss of employment.

- Share option scheme: income calculated based on difference between option price and lower of option granted/option exercise price.

- Asset sold at discounted price/given free: income calculated based on difference between asset market value and amount paid by employee.

- Benefits-in-kind: car, household furniture, apparatus, and appliances, gardener, domestic help, driver, houses sold to employee at discount.

- Note: retirement gratuity is taxable except exemption for ill-health, or retirement age (ie 55) with minimum 10 years employment.

Other Income

- Dividends, interest and discounts

- Royalties, premiums and rents

- Pensions, annuities or other periodical payments

- Gains or profits not falling under any of the earlier

Business Expenses Allowable

- Allowable business expenses

- Payment for wages/ salary

- EPF payment

- Rental of business premise

- Interest on business loan

- Expenses for repair of premise and vehicles used for business purpose

- Allowable specific expenses

- Expenditure incurred in providing equipment for disabled employee (OKU)

- Expenditure incurred in respect of publication in National Language.

- Donation to libraries

- Expenditure incurred in providing services, public amenities and contribution to a charity or community project.

- Expenditure incurred in providing and maintenance of a child care center for the benefit of employees.

- Expenditure incurred in establishing and managing a musical or cultural group.

- Expenditure incurred in sponsoring any art or cultural event.

- Capital allowance

- Given as deduction from business income in place of depreciation expenses incurred in purchase of business assets. For example motor vehicles, machines, office equipment, furniture and computers.

- Double deduction expenses allowable under Income Tax Act 1967

- Export Allowances

(Click to enlarge)

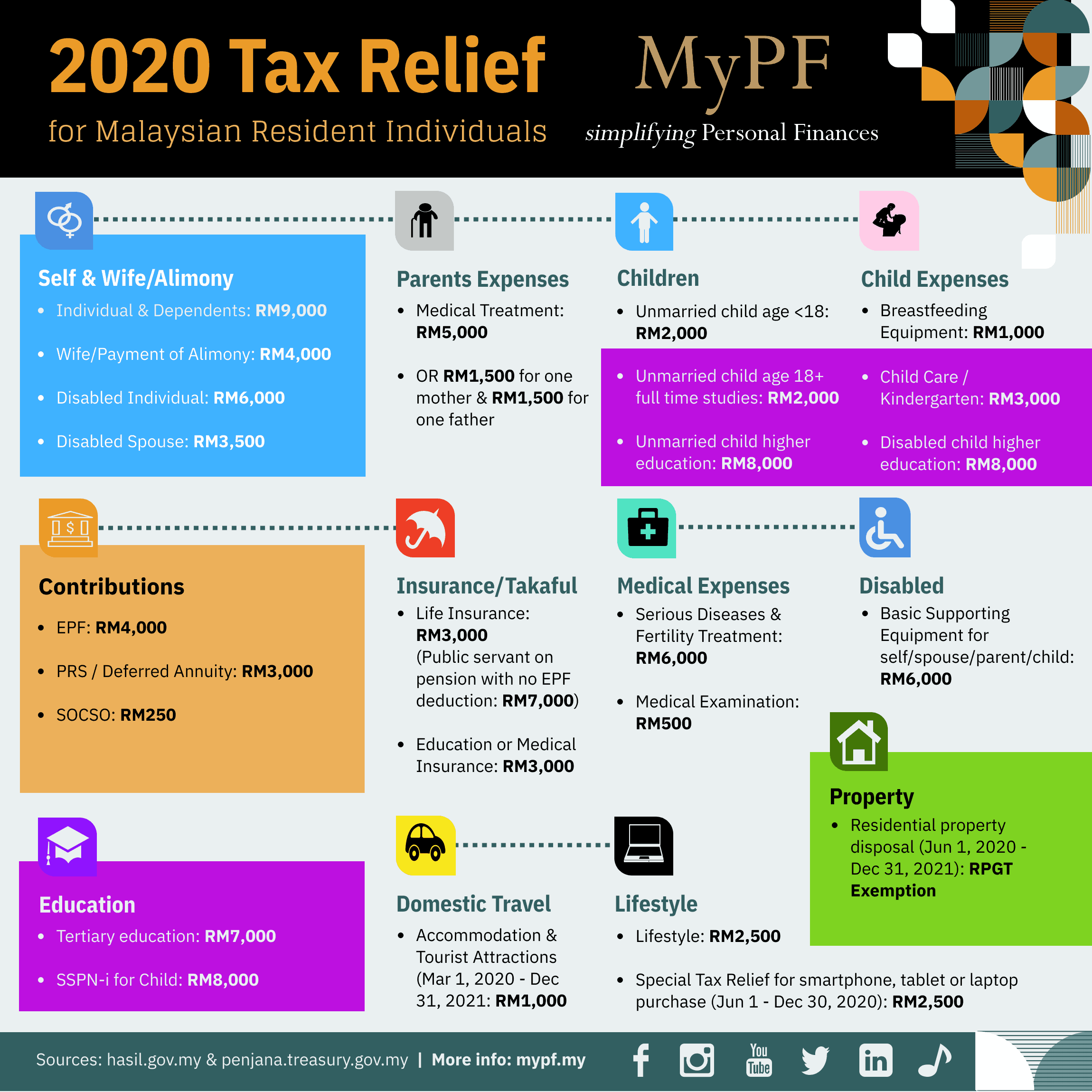

Tax Reliefs for Malaysian Resident Individuals

1. Self, Wife/Alimony & Parents Tax Relief

Individual and Dependent Relatives Tax Relief: RM9,000

Criteria: Allowed to every individual who has total income and is assessed in own name.

Wife/Payment of Alimony Tax Relief: RM4,000

Criteria: Individual entitled to claim deduction for wife if wife has no total income and wife is assessed jointly. If wife has income from sources outside Malaysia and her gross income is more than amount of deduction allowable, husband is not eligible to claim deduction for wife. Payment of alimony requires a formal agreement to qualify for tax relief.

Parents: RM3,000

Criteria: Restricted to RM1,500 for only one mother and RM1,500 for only one father. Provided did not claim for parents medical expenses RM5,000.

2. Contribution to EPF/Approved Provident Fund Tax Relief

Tax Relief: RM4,000

Maximum Tax Relief: RM4,000

Criteria: Total employee or self-employed contribution to EPF or approved provident fund (other than PRS) capped at RM4,000.

3. Life Insurance Premium Tax Relief

Maximum Tax Relief: RM3,000 or RM7,000 (for public servant)

Criteria: Payment of life insurance premiums in the year of assessment on individual’s life or life of the spouse. For pensionable officers with no deduction to EPF, eligible to RM7,000 tax relief for life insurance premiums.

- For Life, 100% of premiums paid eligible for tax relief as life policy.

- For Education/Life, 100% of premiums paid eligible for tax relief as education policy OR life policy.

- For Medical/Life, 60% of premiums paid eligible for tax relief as medical policy OR 100% of premiums paid eligible for tax relief as life policy.

- Accidental/ waiver riders premiums paid are not eligible for tax relief.

- Automation premium loans are not eligible for the tax relief.

- Insurance tax relief calculator

4. Insurance Premium for Education or Medical Benefits Tax Relief

Maximum Tax Relief: RM3,000

Criteria: Payment of education insurance premiums in the year of assessment for self, spouse or child where beneficiary should be the child. Payment of medical insurance premiums for coverage period of 12 months or more.

- For Education/Life, 100% of premiums paid eligible for tax relief as education policy OR life policy.

- For Medical/Life, 60% of premiums paid eligible for tax relief as medical policy OR 100% of premiums paid eligible for tax relief as life policy.

- Accidental/ waiver riders premiums paid are not eligible for tax relief.

- Insurance tax relief calculator

5. Lifestyle Expenses Tax Relief

Maximum Tax Relief: RM5,000 (Lifestyle Tax Relief: RM2,500 + Special Tax Relief: RM2,500)

Criteria: Lifestyle expenses total tax relief is increased with a special tax relief of RM2,500 for smartphone, tablet or laptop purchase from Jun 1, 2020 – Dec 31, 2020. The RM2,500 lifestyle tax relief as follows:-

- Purchase of books journals, magazines, printed newspaper and other similar publications (except banned reading materials).

- Purchase of a personal computer, smartphone or tablet.

- Purchase of sports equipment for any sports activity as defined under the Sports Development Act 1997 (including diving and gym membership but excluding motorized two-wheel bicycles, clothes and shoes).

- Payment of monthly bill for internet subscription.

6. PRS / Annuity Tax Relief

Maximum Tax Relief: RM3,000

Criteria: Deferred Annuity and Private Retirement Scheme (PRS) investment of up to RM3,000. This tax relief is in effect from year assessment 2012 has been extended until year assessment 2025.

7. Contribution to SOCSO Tax Relief

Maximum Tax Relief: RM250

Criteria: Total employee contribution to Social Security Organisation (aka PERKESO). Do note that for employees, the maximum employee contribution is RM19.75 per month for monthly wages of RM4000 and above which means the maximum contribution for tax relief is RM237.

Rate of Contribution for SOCSO (perkeso.gov.my)

8. Child Expenses Tax Relief

Unmarried Child Age Below 18: RM2,000

Criteria: Resident in Malaysia, paying wholly or in part for maintenance of child and child must be unmarried.

Unmarried Child Age 18 above: RM2,000

Criteria: Full-time studies e.g. A-Level, matriculation or pre degree.

Unmarried Child Higher Education: RM8,000

Criteria: Full-time studies at university, college or similar educational establishment in Malaysia.

Breastfeeding equipment: RM1,000

Criteria: Child age 2 or below claimable once every 2 years on breast pump kit, ice pack, breast milk collection, storage equipment, cooler set / bag.

SSPN-i for Child: RM8,000

Criteria: SSPN (National Education Savings Scheme) is a savings scheme for higher education launched in 2004 and eligible for tax relief until 2022. While anyone can contribute to SSPN, only parents are eligible for the tax relief of up to RM8,000 for each parent. The calculation for SSPN-i contribution is based on total investment less withdrawals within the year.

More info on SSPN-i

Child Care / Kindergarten: RM3,000

Criteria: A relatively new tax relief introduced in YA 2019 for child care fees for children age 6 or below at a registered licensed Child Care Centre or Kindergarten. Costs for private nannies or caretakers are not eligible. If both parents are filing taxes, only one parent can qualify for this tax relief. The tax relief has been increased to RM3,000 for YA 2020 – YA 2021.

9. Medical Expenses Tax Relief

Medical expenses for parents: RM5,000

Criteria: Medical expenses includes medical treatment for parents who are diagnosed with illness or physical/mental disabilities, medical care for parents in a nursing home, dental treatment (excluding cosmetic), and special needs expenditure such as nutritional food and disposable diapers. This claim for tax relief must include prescription/written evidence/endorsement from a certified medical practitioner. In addition, the parent must both be living and treated in Malaysia.

Medical expenses for serious diseases and fertility treatment: RM6,000

Criteria: Serious diseases means acquired immunity deficiency syndrome (AIDS), Parkinson’s disease, cancer, renal failure, leukaemia or other similar diseases. From YA 2020 fertility treatment including intrauterine insemination or in vitro fertilization (IVF) treatment consultation fees and medicine for married couples to have a baby.

Medical examination: RM500

Criteria: Complete medical examination for self, spouse or child. A full medical checkup would be as defined by the Malaysian Medical Council (MMC). Medical lab test results are not a full medical checkup thus ineligible.

10. Further Education Tax Relief

Maximum Tax Relief: RM7,000

Criteria: Fees for tertiary education courses undertaken to obtain law, accounting, Islamic financing, technical, vocational, industrial, scientific or technological skills or qualifications. For Masters or Doctorate level, fees on any course of study undertaken for the purpose of acquiring any skill or qualification is allowed.

11. Domestic Travel Tax Relief

Maximum Tax Relief: RM1,000

Criteria: A new tax relief as part of the PENJANA initiative. Domestic travel tax relief for staying at registered accommodation and entrance fees to tourist attractions from Mar 1, 2020 – Dec 31, 2021.

12. Disabled Tax Relief

Disabled Individual: RM6,000

Criteria: Certified in writing by the Department of Social Welfare to be a disabled person.

Disabled Spouse: RM3,500

Criteria: Certified in writing by the Department of Social Welfare to be a disabled person.

Disabled Child: RM6,000

Criteria: Physically or mentally disabled regardless of age and whether child is receiving full-time education. Certified in writing by the Department of Social Welfare to be a disabled person.

Disabled Child Higher Education: RM8,000

Criteria: Unmarried child disabled receiving full-time education degree, Master or Doctorate level in or outside Malaysia at any institution approved by the government.

Basic Supporting Equipment for Disabled: RM6,000

Criteria: For self, spouse, child or parents and includes hemodialysis machine, wheelchair, artificial legs and hearing aids but exclude spectacles and optical lenses.

Tax Rebates, Tax Exemptions, and Tax Deductions

Tax Rebates for Malaysian Resident Individuals

- Individual chargeable income < RM35,000: RM400

- Husband and wife jointly assessed and joint chargeable income < RM35,000: RM800

- Zakat, Fitrah or other Islamic religious dues paid: amount in year

- Note: any excess payment is not refundable

Tax Exemption for Property-Related

- Real Property Gains Tax (RPGT) exemption for up to 3 residential property disposal (Jun 1, 2020 – Dec 31, 2021)

- Rental deduction equivalent to rental reduction amount for SME tenants running business with min 30% reduction of existing rental rate (Apr 1, 2020 – Sep 30, 2020)

Tax Exemption for Employment

- Retirement gratuity due to ill-health or retirement age (ie 55) with minimum 10 years employment

- Gratuity paid out of public funds or to a contract officer

- Compensation for loss of employment increased from RM10,000 to RM20,000 for each full year of service

- Medical and dental benefits including maternity expenses and traditional medicine

- Child care benefit

- Goods / services benefit given to all employees at a discount with value below RM1,000

- 3 local trips / RM3,000 per family for overseas trip

- Relocation package

- Gifts of handphones, notebooks & tablets RM5,000 for work from home arrangement (Jul 1, 2020 – Dec 31, 2020)

Tax Exemption for Other Income

- Scholarships

- Royalty income below exemption limit

- Publication of artistic works / recording discs / tapes exemption: RM10,000

- Translation of books / literary works exemption: RM12,000

- Publication of literary works /original paintings/musical compositions exemption: RM20,000

- Income for appearances in cultural performances

- Income from research findings

- Fees or honorarium for expert services

- Income remitted from outside Malaysia

- Interest from bank or financial institution or Lembaga Tabung Haji

- Dividends from exempt accounts of companies or co-operative societies

- Investment gains or dividends income from unit trust funds at unit holders level

- Investment gains or dividend income from investments (unless at high frequency that it is viewed as active income) except for disposal of real-property, P2P lending and equity crowd funding which is taxable income

- Overseas or foreign-based income including dividends and investment income

Tax Deductions

- Gifts of money, contributions in kind or art work to approved Government, State Government, Local Authorities, Approved Organisations , Libraries or National/State Art Gallery

- Gift of money or medical equipment to Covid-19 fund or cash donation to National Disaster Management Agency

Income Tax FAQ

Q: Can you please explain on the increase in tax exemption from 10k to 20k for each full year of service. How does this apply to those who has been redundant in YA 2020?

A: This would affect if you have loss employment & given compensation for Loss of Employment (e.g. VSS – voluntary or mutual separation scheme) for YA 2020 – 2021. For example, if you have been working with the same employer for 10 years , you would be exempted of up to RM20k x 10 = RM200k.

Q: If wife not working this year, can claim extra under dependent? Then next year she goes back to employment, then she submit back as normal?

A: Yes you can file as such jointly and then when she resumes work to file individually to reduce tax payable.

Q: Can explain more on the following relief ? How to claim this? Gifts of handphones, notebooks & tablets RM5,000 for work from home arrangement (Jul 1, 2020 – Dec 31, 2020). Companies give out equipment to work from home? Normally, it will belong to the company.

A: This would fall under a tax exemption. If company gifts you these equipment, normally it would be treated as part of your chargeable income (which is taxable!). But up to RM5k exempt for this duration. Note: Gift meaning you own it & doesn’t need to be returned to the company

Q: Is there tax relief on insurance for parents?

A: unfortunately there’s no tax relief for insurance premiums for parents. There is a RM5k relief for parents medical expenses.

Q: Does a printer falls under a Lifestyle/Special Tax Relief?

A: Unfortunately no.

Q: Can the RM2,500 lifestyle can be combined with the new RM2,500 laptop/tablet/smartphone category and allow a single claim of RM5,000 laptop?

A: Unofficial rumors is yes it can be combined. Have yet to see an official confirmation though. (If you see an official confirmation, please do let us know!)

Q: Isn’t the RM2,5000 lifestyle relief already around for years?

A: The new addition is the additional 2.5k for laptop/tablet/smartphone on top of the RM2,500. Also next year YA2021 onwards lifestyle increased to RM3,000.

You May Also Like

- Income Tax Relief Malaysia 2019

- Your Guide to Tax Planning in Malaysia

- Insurance Tax Relief Calculator

- PENJANA Tax Relief

- Budget 2021 Highlights: Tax Relief

{kind=link}

{kind=link}

{kind=link}

Don’t quite understand this clause below:

2. Contribution to EPF/Approved Provident Fund Tax Relief

Tax Relief: RM4,000

Maximum Tax Relief: RM4,000

Criteria: Total employee or self-employed contribution to EPF or approved provident fund (other than PRS) capped at RM4,000.

I am already an EPF contributor of 11%, so does that mean I am eligible for Max Tax Relief of RM4000 there?

Hi,

Does parents medical expenses has to rm2500 each or it does not matter as long as the total amount to be claimed is Rm 5000 for both. Example: Rm 1000 for dad, Rm 4000 for mum.

Hi if my tablet is bought before June 2020 (In May) , would I be entitled for the special tax relief still?

If I purchase a laptop of 4000 and handphone of 1000, can I claim 2500 on original lifestyle tax relief and balance 1500 laptop + 1000 handphone on 2nd lifestyle tax relief ?