Insightful perspectives on this month’s market events. The original version of this article was published on ifastcapital.com.my.

Contents

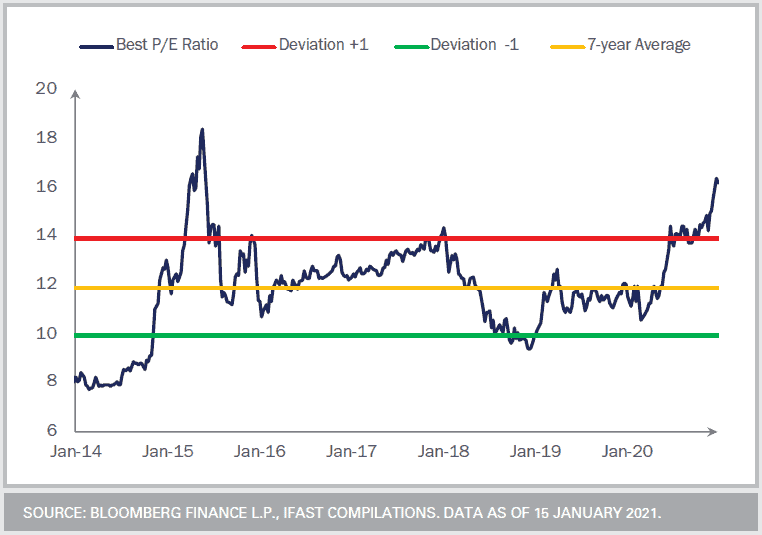

Wall Street Wraps 2020 and Kickstarts 2021 at All-Time High on Stimulus Hopes Despite Surging Virus Cases

Event

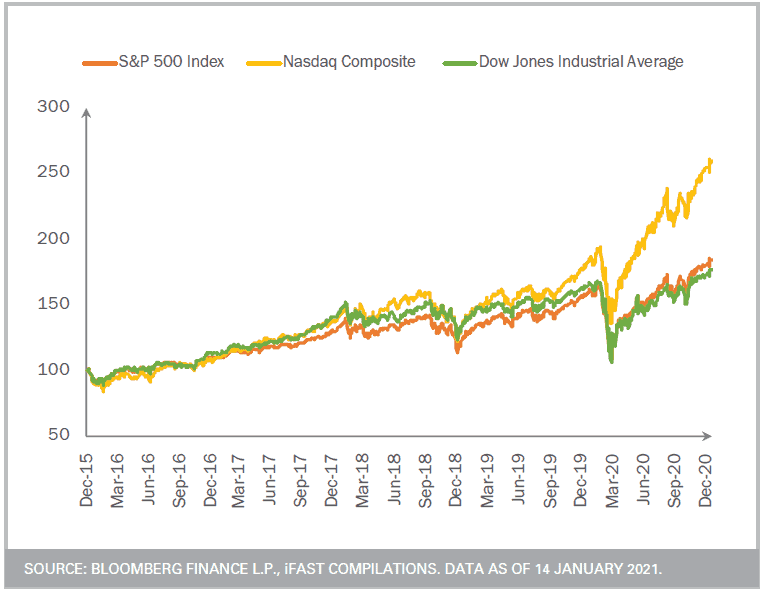

As we wrap 2020 into conclusion, US equities, represented by S&P 500 index clocked a positive return of 16.3% while the tech-heavy Nasdaq Composite gained 47.6% of calendar year return, capping off one of the greatest comebacks despite rising coronavirus cases and pronounced unemployment. The stellar performance was fuelled by historic government fiscal stimulus, ultra-easy monetary policy supports, and optimism over potential global economic recovery as vaccines are expected to be widely distributed by 2H2021. Furthermore, market participants are expecting corporate earnings to balloon in 2H2021, boosted by President-elect Biden’s bigger stimulus proposal.

Impact

In 2021, we opine that the policy rates in the US will remain lower for longer with the Fed’s new average inflation targeting framework, the central bank will not increase rates even if fiscal stimulus is much larger than the market’s expectations. Quantitative easings and muted inflation will keep short-term interest rates at the bay, painting a positive economic backdrop to witness recovery from lockdown recessions. Nevertheless, the restless bulls within US equities have made the markets vulnerable due to its premium valuation where any deviation from the positive scenarios (higher treasury yield, US-China tension, or later-than-expected vaccine distribution) could trigger a rapid correction within the global equity markets.

Opportunities/Risks

Given its premium valuation, those who have invested (or looking to invest) into US market may find their nerves often rattled by volatile movements within technology names and political uncertainties. For Asian and EM equities, we are positive about the regions amid improving risk appetite and global economic recovery prospects ahead, we expect global growth to continue recovering at a meaningful pace thus consolidating our overweight view on equity vis-à-vis fixed income by 2.5%. To remove the hassle within asset allocation decisions as well as fund selection for our investors, one should consider the in-house managed iFAST Managed Portfolio to invest globally as we foresee greater market volatility ahead in 2021.

Malaysia Enters MCO 2.0 and State of Emergency Amid Spiking Virus Cases; Local Small Caps Outshone the Big Boys

Event

In the backdrop of the worsening Covid-19 pandemic with the daily local new cases reaching a new high of more than 3,000 cases, Malaysia has reimposed Movement Control Order (MCO) for 2 weeks from 12th January 2021 onwards alongside the King’s declaration of State of Emergency to curb the pandemic. With that, Parliament and State Legislative Assemblies will be suspended which was a move widely seen to keep a lid on the rumors of political uncertainty at least for the next 8 months. Constructively, the state of emergency will not affect business activities while no curfews will be implemented.

Impact

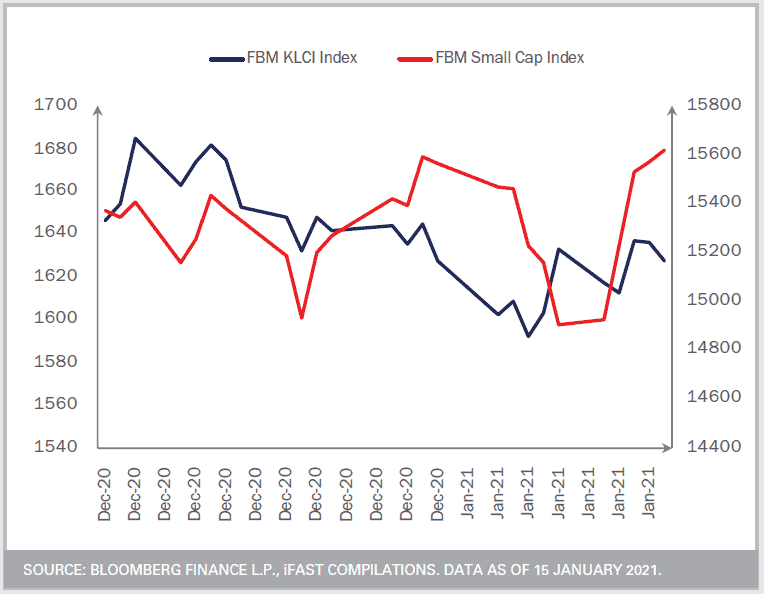

Right after the announcement, the FBM KLCI index dipped as much as -1.0% to hover around 1600 currently, also tracking the drop in US markets overnight and overall Asian markets on Monday. The local bourse erased its earlier losses and closed by only 5.21 points lower (-0.3%) as investors flocked into glove counters. Meanwhile, Malaysia’s small-cap segment, represented by FBM Small Cap Index, gained 2.0% as investors speculate stronger buying interest in smaller players amid a potential higher retail participation rate.

Opportunities/Risks

We are of the view that any sell-offs will be an appealing opportunity for long-term investors to accumulate local equities, particularly the local small-cap segment. Considering the fact that the majority of the local small-cap players are from the manufacturing and exports sector, recovery in external demand and easing trade tensions will benefit small-cap stocks moving forward. Both equities and bonds are set to deliver positive returns as they will benefit from the reopening of the country’s economy and borders provided with an adequate dispensation of Covid-19 vaccines by 2H2021.

Global Financial Sector Underperformed in 2020, Weighed Down by Earnings and Suspensions on Dividends and Share Buybacks

Event

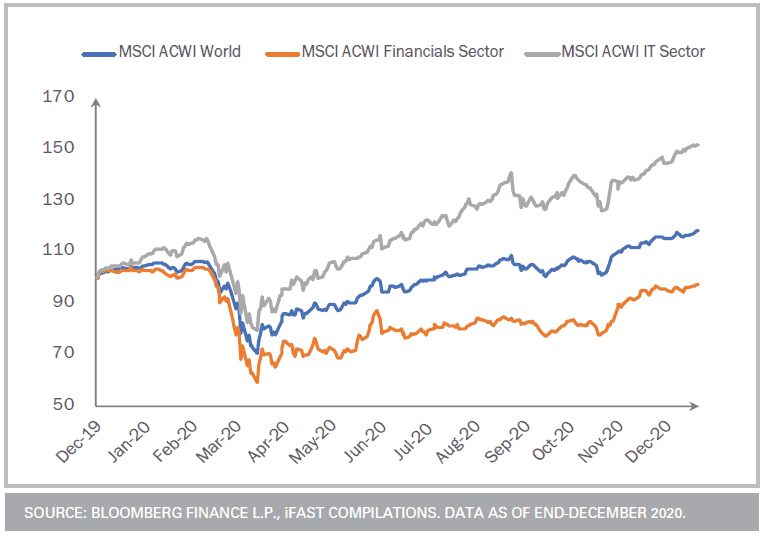

As global equities ended 2020 on a higher note, with markets closing the year in the positive territory after an impressive rebound. However, the global financial sector has underperformed its growth peers amid lower interest rates that have negatively impacted the Net Interest Margins (NIMs) of banks. To make things worse, the severity of the lockdown has led to a significant increase in loan loss provisions, resulting in a sharp drop in banks’ earnings.

Impact

Moving into 2021, the positive vaccine news is a bright spot on the horizon. Vaccine deployment should help to accelerate global recovery, and banks have a key role to play. Loan loss provisions, the key reason for weak earnings in 2020, should also ease, which will help in earnings recovery and earnings growth. We also expect governments to ease restrictions on share buybacks and dividends, which will be a great share price catalyst for the banking industry.

Opportunities/Risks

Earnings this year is expected to register a decline by 18.4%, before jumping by 20.4% and 15.1% to reach USD112.7 and USD129.7 in FY2021 and FY2022 respectively. We maintain our star ratings for the Global Financial sector at ‘3.5 stars’ Attractive.

Chinese Equities Back to 2015 Peak on the Back of Strong Economic Rebound and Renminbi Bull

Event

China onshore equities, represented by CSI 300 index has ended above their 2015 high, officially marking its recovery from the -43.0% bloodbath 5 years ago. The benchmark index clocked a stellar return of 50.4% from its low in March 2020, a rally that was fueled after Chinese lawmakers allow investors to buy stocks using margin accounts as well as stronger economic recovery underpinned by solid domestic demand. The bulls in the marker were also charged by stronger currency alongside improving economic data. Having that said, China A-shares representing by the CSI 300 index is currently trading at its highest P/E ratio in 5-years, suggesting that the stock market might be trading at its peak.

Impact

While we are cautious on the rapid rallies within Chinese equities, Chinese stock market remains relatively cheaper than the valuation in 2015 where the CSI 300 index is now trading at a PE of 16 times on its estimated forward earnings, compared to a multiple of more than 19 times back then. On economic data front, China’s inflation rate has finally returned to positive in December 2020, up 0.2% y/y from -0.5% in November and projected to remain solid in coming months with economic activity set to remain strong in 2021. Meanwhile, China export grew 18.1% y/y in December 2020 as global demand towards Chinese goods remains robust, slows in December but beats analysts’ forecast of 15.0%.

Opportunities/Risks

Our base case for a strong recovery within China is setting on our view that China’s demand is an integral driver of i) the global industrial cycle (influences commodity demand) and ii) EM exports. We expect China’s robust demand recovery to continue in 2021 for reasons laid out in our recent update on China equities. Having that said, the local demand has been the main driver for the improvement in the manufacturing and service sector, China still needs external demands for further growth. In a nutshell, investors who share positive views on China with us could consider adding Greater China and/or China equity funds into their portfolio with an allocation not more than 10% of their portfolio.

You May Also Like

- Market Overview December 2020

- Market Overview November 2020

- Market Overview October 2020

- Market Overview September 2020

- Market Overview August 2020

Invest in unit trusts, PRS, EPF i-Invest funds & managed portfolios from as low as 0% sales charge with iFAST Capital by talking to your financial planner.

{kind=link}

{kind=link}

Leave A Comment