Harness the power of compounding to plot your way to a million (or more!) Ringgit. The original version of this article was published on StashAway.my.

Short of winning the lottery, retiring with RM100,000, RM1 million, or RM10 million in the bank doesn’t just happen magically. Yet, lotteries still exist and thrive because so many people want to wake up as a millionaire with as little effort as possible.

But what if I told you having a lot of money for your retirement isn’t as hard as you think?

Achieving any financial goal takes specifying the goal, then developing and sticking to the right financial habits as early as possible, and then staying the course. We’ll get into all of this as we guide you to that RM1 million amount by the time you’re 65. The same math and logic works whether your goal is to have RM5 million, RM10 million or RM50 million.

Contents

Set your goal

When specifying a financial goal, you need to decide on two critical pieces of information: 1) the amount you want and 2) the time at which you want it. Here, we already have that: RM1 million by age 65. With this, we’ll be able to determine how much we need to save each month, what to do with that savings, and how to make sure we stick to the plan.

Start saving as early as you can

To reach any financial goal as easily as possible, it’s important to start saving part of your paycheck each month as early as you can. Saving early allows you to take advantage of the power of compound interest, and that means you won’t have to save as much in the long term to reach your financial goals.

Take advantage of the power of compound interest

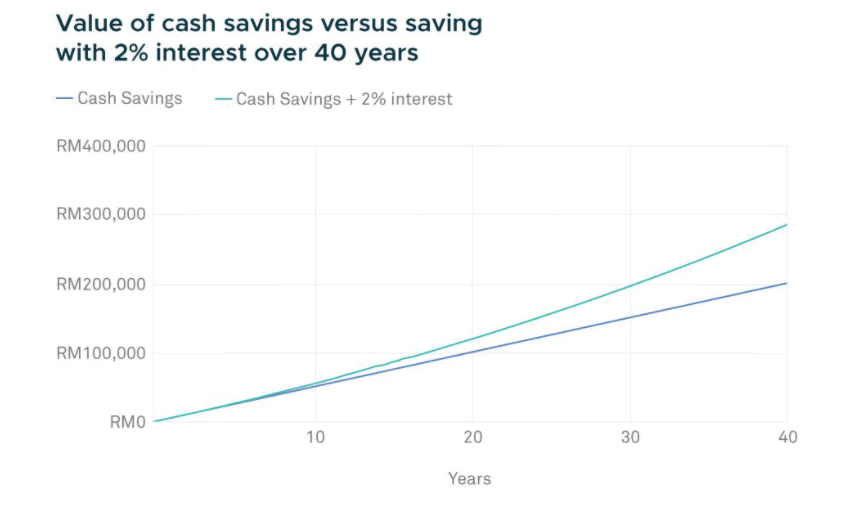

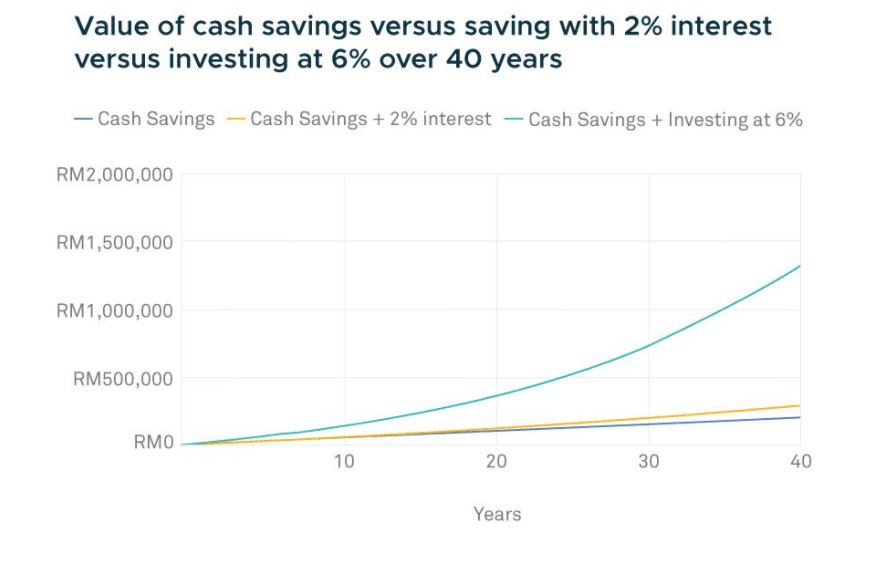

Below, you can see how much more you can have over time just as a result of taking advantage of compound interest. Let’s say that you decide to put a constant amount of money, every month, in a savings account yielding 2% per annum. The graph shows that if you were to save RM6,000 in a year (RM500 per month), and earn 2.0% interest in your savings account, at the end of one year you would have RM6,055. The next year, you would earn interest, not on the RM6,000 you saved, but on RM6,055; this takes your asset value to RM12,233 (not RM12,000) at the end of year 2, thanks to the compound interest. That means that in year one, you earn RM55 in interest, in year two, you would have earned RM233 total in interest, in year three, you would have earned RM535 total in interest, and the earnings just from interest would continue to increase each year.

(Source: stashaway.my)

If you started saving RM500 per month when you were 25, and you want to retire when you’re 65: what would those savings get you in 40 years? If you were to leave RM500 in cash after 40 years, that would leave you with RM240,000 (not considering inflation). If you were able to earn 2% from a savings account, you’d have RM367,218. That’s an additional RM127,218 in your retirement stash just from 2% interest. Not bad. As you can see, the earlier you start saving, the less money you have to put aside to reach any of your financial goals.

But here, we’re talking about how to have RM1 million by the time you’re 65 years old. So how do we bridge the huge gap of RM632,782 to reach RM1 million when we’ve only saved RM367,782?

Not by playing the lottery.

Invest your savings

The way to make that RM500 per month work for you is to invest it to amplify the power of compound interest. For a long-term goal, such as retirement, the 2% savings account is not the right investment vehicle. When you have time, you can afford to take a little bit more risk; again, we’re not talking about the lottery. If you were to invest that RM500 each month in a balanced portfolio that generates 6% interest, your money will grow to RM1 million by 65 as a result of the interest you can generate by investing your savings.

(Source: stashaway.my)

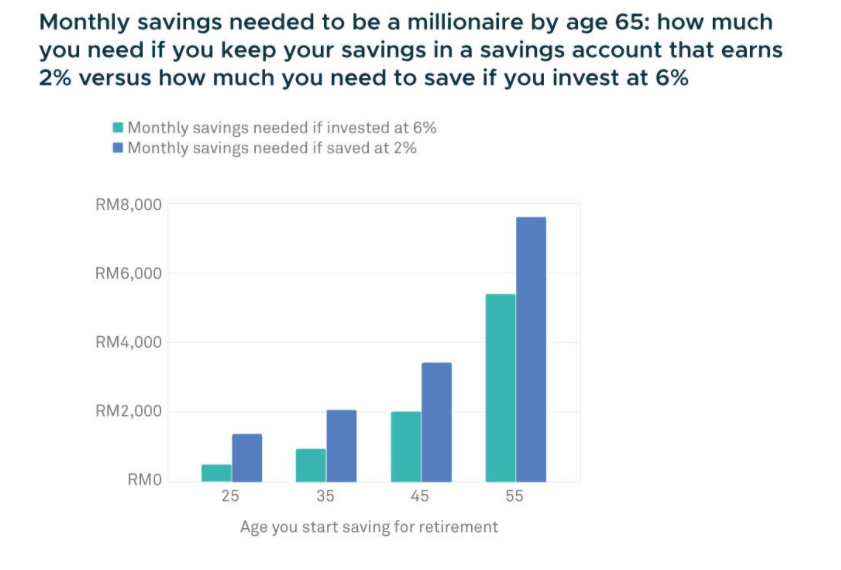

Another way to look at it is that if, at 25 years old, you insisted on keeping your monthly savings in a savings account and still wanted to have RM1 million by age 65, you’d have to save about RM1,380 per month instead of investing that RM500 per month in a balanced, growth-oriented investment account.

If you start investing in a portfolio returning 6% per annum at 25 years old, you will need to invest only RM490 per month to get to RM1 million by age 65. If you wait until you’re 35 to start saving monthly, you will need to save more than double that amount. If you want until you’re 45, you’re looking at saving more than RM2,000 per month.

(Source: stashaway.my)

By saving and investing early, you can put less towards your retirement in the long term. By saving RM490 every month for 40 years, you only have to invest RM235,200 over that 40-year period, whereas if you waited until you were 55 to start saving for retirement, and you invest RM5,404 each month for 10 years, you are putting in RM648,480. In short, saving earlier even saves you money in the long term.

Compound interest really is that powerful.

The takeaways here are 1) you need to save as early as possible and as consistently as possible, and 2) you need to invest those savings. The longer you put off saving and investing, the less time compound interest can do the work for you to get to RM1 million, and your retirement will be that much more expensive for you.

So how do we make sure we save and invest consistently?

You can always save

Do you really prioritise saving for your retirement? The only way to prove that is how consistently you save enough each month. Making sure you consistently save each month comes down to having control over your budget. Having specific goals in mind can motivate you to stick to a clear savings plan that fits seamlessly into your budget.

Whether you make RM50,000, RM200,000 or RM1 million a year, you should budget how much you save and invest each month. Assessing how you spend your money and allocate your budget can illuminate pockets where you can stop spending and start saving. You’re never too rich or too poor to save each month. So look for ways to cut back: RM1,000 less in rent each year, or an RM70,000 car instead of an RM200,000 car. It’s money you could be putting towards your future, and it all adds up over time. Even your latte addiction could be costing you.

And if you’re just getting by these days with a monthly paycheck, how will you get by in retirement when you’ll have no income and minimal savings on which you can rely? Make sure you’re saving enough now.

Make sure you invest consistently

Anyone can always find an excuse not to invest money this month: vacation this month, car repairs, or unexpected visits to the doctor. Those excuses aren’t valid. You should have an emergency fund set up so that nothing comes in the way of investing each month. Otherwise, you’re pushing off your retirement, or at least making it less comfortable. Each month you don’t invest towards your retirement, future you isn’t happy with current you.

With an emergency fund and effective budget in place, you don’t have an excuse not to retire comfortably. So how do you make sure you actually invest those savings each month?

Set up a standing instruction

It can be a pain to remember to invest each month. Forget the calendar reminders or Post-it notes on your desk. Investing consistently can be as easy as setting up automatic contributions. So, set up standing instruction so you don’t have an excuse to miss a month.

Stay the course

It can feel discouraging to want to invest when the markets seem volatile. However, when it comes to investing, there will be many ups and downs in the market along the way. Staying the course and dollar-cost-averaging into the portfolio every month no matter the market conditions, will get you to reach any monetary goal you have.

Saving now means paying for a better future.

Will you retire as a millionaire?

StashAway x MyPF exclusive signup privileges!

- StashAway Malaysia promo code 0% fees for RM100k invested for 6 months: signup link

- StashAway Singapore promo code 50% fees for SGD50k invested for 6 months: signup link

You May Also Like

- Why You Should Track Your Net Worth

- 4 Ways to Invest in Yourself (and Your Financial Future)

- MyPF Compounding Interest Calculator

- 6 Steps for Setting Your Financial Goals

What other methods are you employing to reach your millions of Ringgit?

{kind=link}

{kind=link}

Leave A Comment