Insightful perspectives on this month’s market events. The original version of this article was published on ifastcapital.com.my.

Contents

US Corporates Rebound as Earnings Points to Recovery

Event

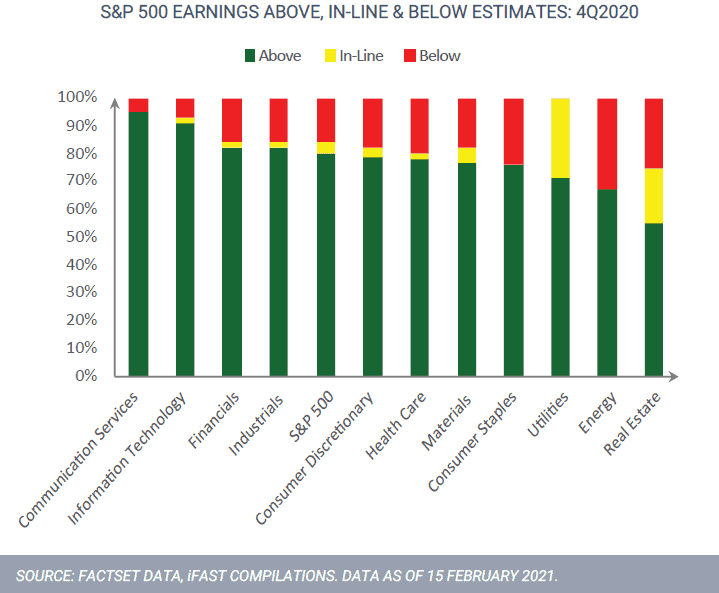

According to Factset, 74% of the companies in the S&P 500 index have reported their earnings results for 4Q2020 as of 12 February 2021. Of these companies, 80% have reported actual earnings per share (EPS) above estimates, which beats the five-year average of 74%, on its way to mark for the third-highest percentage of S&P 500 companies reporting a positive EPS surprise since 2008. The overall increase in earnings for the index within 4Q2020 was attributable to the companies in the Financials, Information Technology, and Communication Services sectors.

Impact

The stronger-than-expected corporates earnings came in as a positive surprise for the market participants, indicating that US companies have started to turn the tides on the pandemic-induced recession in the last quarter of 2020. As sales and earnings growth trending back to positive territory, following three consecutive quarters of contraction in 2020, has come sooner than many analysts had expected, boosted by the US government’s historic fiscal stimulus and looser monetary policy from the Federal Reserve.

Opportunities/Risks

While US will be supported by further fiscal stimulus from the Biden administration, a potential rebound in relative earnings within the global equities are well-positioned from the market rotation into value stocks and traditional global cycle play. To remove the hassle within asset allocation decisions as well as fund selection for our investors, one should consider the in-house managed iFAST Managed Portfolio to invest globally as we foresee greater market volatility ahead in 2021.

Bank Negara Malaysia (BNM) Maintains OPR at 1.75%, Considers Policy to be Appropriate and Accommodative

Event

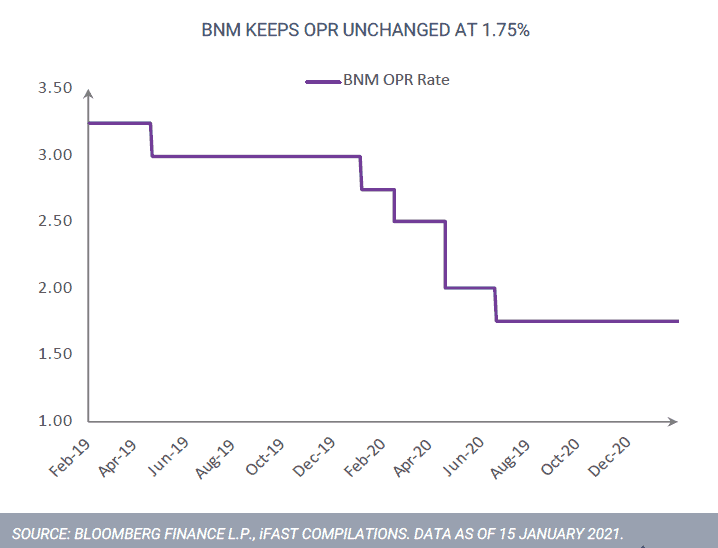

In its latest policy meeting on 20 January 2021, Bank Negara Malaysia has announced to maintain the OPR rate at 1.75%. The central bank has cited improving manufacturing and export activity, rolling out of COVID-19 vaccines alongside ongoing policy support is expected to bolster economic recovery going ahead. BNM, however, cautioned that downside risks to the near-term growth remain, stemming from MCO 2.0 as well as uncertainties of the pandemic, but will be less severe compared to what was experienced in early 2020.

Impact

At iFAST, we deem the interest rate decision as keeping additional bullets available should it be needed. In light of the uncertainties surrounding the local economic recovery path amidst spiking local virus cases, we believe that a lower interest rate environment will be here to stay in 2021. We see higher possibilities for BNM to announce a cut to the OPR on March 4 as renewed movement restrictions are putting the 2021 6.5-7.5% economic growth forecast at risk.

Opportunities/Risks

We are of the view that low interest rate environment is likely to keep the demand for fixed income to be robust compared, supporting bond prices from investors’ appetite for yields. Looking towards the Ringgit, we are holding a slightly positive view of the local currency. Improving oil prices and a recovery in the global economy would also bode well for emerging market currencies such as the Ringgit. For investors who are seeking shelter from currency translation risk in foreign investments, we recommend MYR-hedged class when the share class is available.

China Posted 2.3% GDP Growth in 2020, Grew 6.5% in 4Q2020 While Developed Economies Struggle

Event

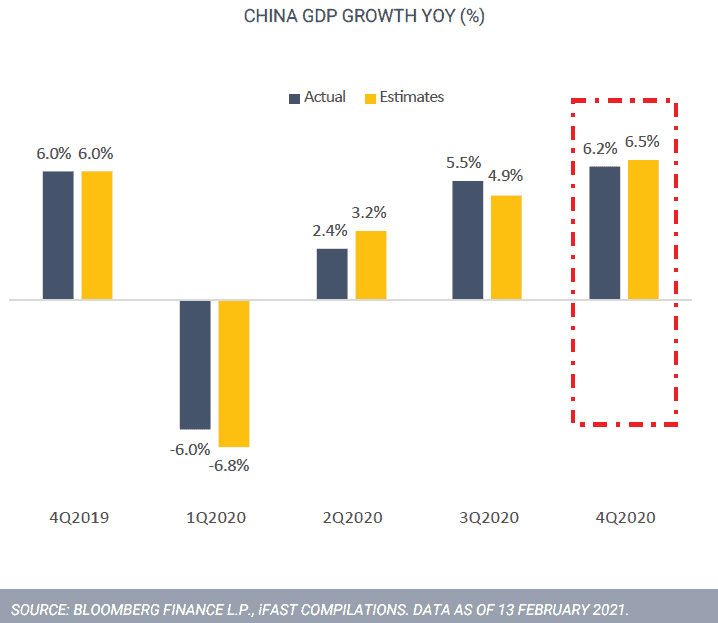

China announced that its economy grew by 2.3% GDP growth for 2020, a stronger-than-expected number that showed a V-shaped recovery from a pandemic-induced economic slump that is still devastating most economies globally. In 4Q2020, the Chinese economy expanded 6.5% y/y, beating the analysts’ expectation of 6.2%. The robust growth data was supported by robust industrial production, investment, and exports, especially toward the final months of 2020. Retail sales, an indicator of consumer sentiment, remain sluggish due to a slow recovery in the catering and restaurant industries.

Impact

In contrast, the latest US GDP figures show a -2.3% decline in 2020 where the divergence means China will likely overtake the US as the world’s largest economy earlier than expected. That puts China’s economy at only USD 6.2 trillion behind the US in 2020, down from USD 7.1 trillion in 2019, which echoes with our view that the pandemic has been a larger blow to the US economy than the Chinese economy. Looking ahead to 2021, we foresee domestic consumption and corporate investment to continue as the growth engines for China’s economic growth.

Opportunities/Risks

We expect China’s robust demand recovery to continue in 2021 for reasons laid out in our recent update on China equities. In a nutshell, investors should add Greater China and/or China A-share funds into their portfolio with an allocation of not more than 10% of their portfolio to capitalise on this attractive investment opportunity.

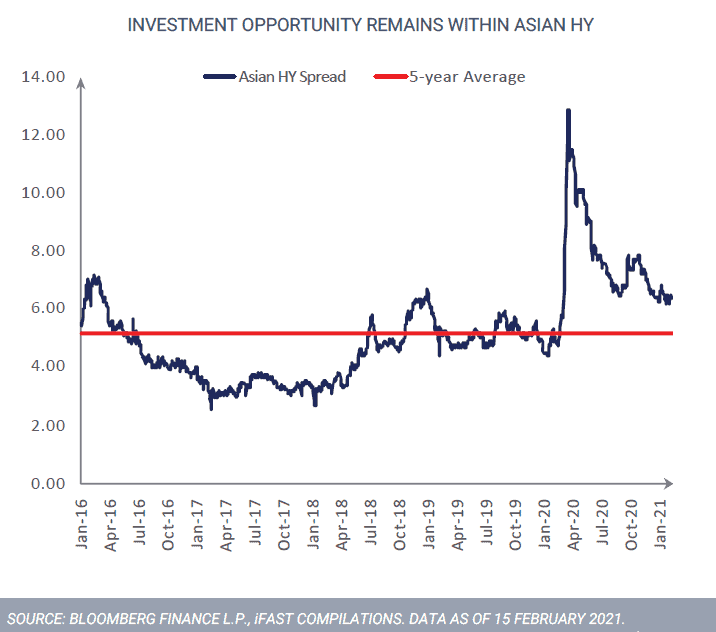

Asia High Yield: A Gem Within The High Yield Universe

Event

Persistently low policy rates, reinforced by improving risk sentiment have emboldened investors to venture beyond traditional safe havens and down the credit spectrum. Amongst the riskier debt segments, Asian high-yield offers the most attractive credit opportunity and is our top pick for 2021. Based on our Asia macro and earnings outlook, we expect lower stress and healthy fundamentals for Asia high yield issuers this year.

Impact

Asia high yield provides strong coupon return, offering handsome yield pick-ups over peer segments. Valuation for the asset class remains cheap, with a spread close to one standard deviation above the historical average. We expect ample room for tightening, back to near pre-Covid levels, driving upside for price return. Interest rate risk remains muted given lower duration and high yield per unit duration. Default risk is subsiding and will be manageable with the current spread compensating well for undertaking such risk. We view risk premia offered by Asian high yield to be very attractive.

Opportunities/Risks

From a reward perspective, Asia HY offers the combination of attractive yield pickup, value capture, and spread compression while backed by healthy fundamentals. All things considered, Asia HY is one of our top fixed income picks for 2021 and the current yield/ spread offers a good entry opportunity.

Invest in unit trusts, PRS, EPF i-Invest funds & managed portfolios from as low as 0% sales charge with iFAST Capital by talking to your financial planner.

{kind=link}

{kind=link}

Leave A Comment