What car does a financial planner drive? Wealth Vantage Advisory is pleased to launch our “Have a Plan: How I Ride” series. Our first financial planner is our Chief Knowledge Officer Stev Yong who is also the founder of MyPF. This is the story of how he rides – both literally and financially.

Hey y’all. Stev here and this is how I ride – be it my finances or my literal ride.

View this post on Instagram

Contents

Q1. What Car Do You Drive?

I drive a second-hand Honda City which I bought in cash, therefore avoiding paying loan interest. This is my third car after a second-hand Proton Iswara, which previously belonged to my parents (thanks, mom and dad!), and a second-hand Proton Wira that I also bought with cash.

Stev’s second-hand Honda City, bought in cash.

Q2. What Influenced Your Car Choice?

I am reminded of advice from Dato’ Boonler Somchit (retired CEO of Penang Skills Development Centre) that a car is just to get you from point A to point B. And, advice from Dato’ Seri Cheah Cheng Hye (Co-Chairman & Co-Chief Investment Officer of Value Partners Group) to get a reliable quality car (i.e. Japanese make) that will serve you well and depreciate slower in value.

With that in mind, I figured I could do with a car that is reliable, not necessarily brand new, easy maintenance, and of a make whereby spare parts are easy to find.

I started by narrowing my search to Japanese cars, and from there checked what second-hand options were available. I read reviews and asked around about spare parts availability. In other words, I looked for one that is most cost-effective of all the choices available to me at the time.

Recently, we were blessed with a new addition to our family so I may yet change cars with a stronger focus on safety. Ideally, our next choice should be something that can be paid for fully in cash from our passive investments.

Despite additional maintenance plus wear-and-tear costs, I estimate to have saved at least 50% in vehicle costs overall compared to if I had bought a new car of similar type.

Q3. What are the Car Maintenance Expenses?

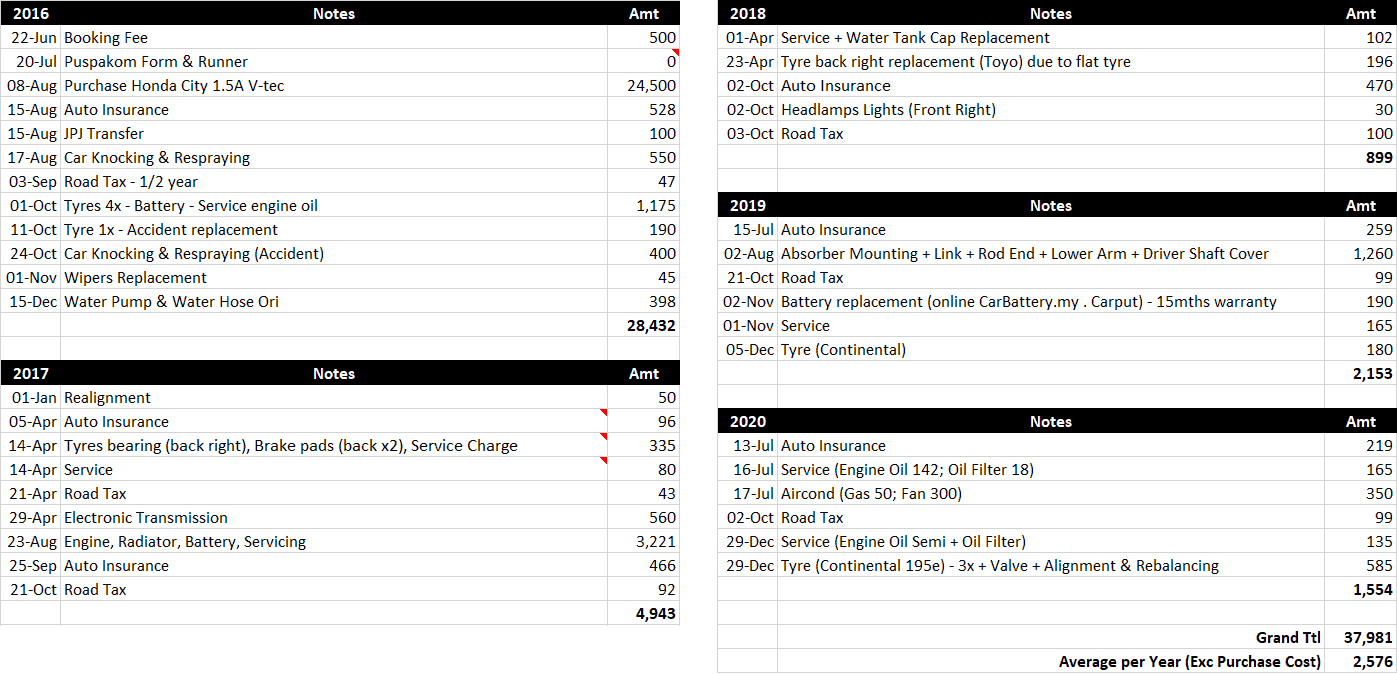

From the time I bought this car in 2016, I started to list down all the expected expenses coming with the car such as petrol, maintenance, road tax, etc. The detailed breakdown can be seen from the screenshot of my allocated expenses until 2020.

Stephen’s maintenance costs records.

Stephen’s maintenance costs records.

As you can see in 2016, my expenses for the car totaled more than RM28,000, with RM24,500 from it being the price of the car. The rest of the expenses were to cover the Puspakom fee, refurbishing, and replacing several parts of the car.

In 2017, majority of the expenses were due to servicing the inner part of the engine like the battery and radiator with total cost amounting to RM3,000.

In contrast, in 2018 my car’s expenses only cost around RM900 compared to previous two years. Here, instead of forking my income to pay for a car loan monthly, I was able to save more money for my other expenses and investment.

Meanwhile in 2019, my car expenses increased again to more than RM2,000 with majority of it for car maintenance as my absorber and other parts needed replacement.

In the last year, I spent around RM1,500 with most of it for my engine oil maintenance and replacing the tyres.

Most of my car expenses has been for car maintenance and replacing several parts, which is understandable as it is a second-hand car. But, I managed to save a good amount of money with total of all the expenses amount to RM30,000 and average of RM2,000 per year.

If I had chosen to buy a brand new car, let say a Honda City new edition, it would be costing me around RM700-RM800 a month and around RM9,000 a year. When you add maintenance expenses into that, it will definitely cost more than what I paid for in my 5 years.

In short, buying a 2nd hand car doesn’t cost too much in maintenance provided you didn’t buy a lemon.

Let’s switch gears.

Q4. How Do You Approach Your Personal Finances?

I plan my finances by following these following these 10 golden rules:

- Set your personal finances goals

- Review personal finances monthly

- Say no to (bad) debt

- Fund your emergency savings

- Pay yourself first

- Invest intelligently

- Protect against risks

- Get the right property

- Live life with love

- Reward yourself occasionally

Q5. How About Your Investing Approach?

I look at many things from a value perspective ranging from buying something to investing. Investing is also one of my key priorities. Investing needs to be a well thought out process and planned in advance. I invest regularly in a mostly automated way to pay myself first. And then i regular rebalance and reoptimise to improve my portfolio performance.

I am also a strong believer of asset allocation as all weather portfolio strategy to optimise returns while reducing investment risk no matter what economic condition we are in. Proper investment asset allocation helps reduce volatility by 90% while accounting for 40% of investment returns. Asset allocation is an ongoing process to set how your investment goes into various asset classes.

Any Final Tips?

“Simplicity is life’s greatest sophistication” ~ (adapted from Leonardo DaVinci).

Your financial plan doesn’t have to be complicated. In fact having a simple plan will likely work out even better! It’s not easy though as it require focus, discipline and perseverance.

I believe that each and everyone can not only survive but thrive!

Follow @StevYong: Facebook, Instagram, Twitter, Linkedin, TikTok.

Do you have any stories on how you ride? Share with us in the comments section below.

“How I Plan” is a series focusing on personal stories by licensed financial planners and Malaysians. If you have a story you would like to share, get in touch with us so we can document it.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment