What car does a financial planner drive? Wealth Vantage Advisory (WVA) is pleased to launch our “Have a Plan: How I Ride” series. Our financial planner for this edition is our Managing Director, Rafiq Hidayat Mohd Ramli. This is the story of how he rides – both literally and financially.

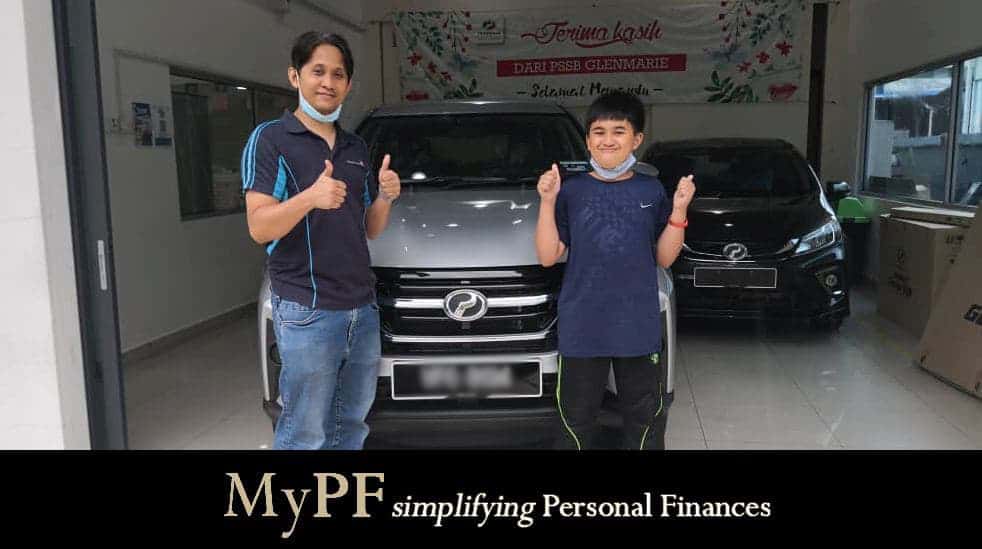

Hi everyone, I’m Rafiq Hidayat (and that is my son, Amir), and this is how I ride, financially and realistically

View this post on Instagram

Contents

Q1. What Car Do You Drive?

I bought a new Perodua Aruz October last year after 16 years using a Perodua Kelisa, which I owned from the time I started working in 2004. You can read more about the process I went through in purchasing my new car here.

As outlined in the article, the main reason I bought the new car is because the Kelisa was already at a state where I was spending more on repairing the car (compared to the monthly payments for the new car) plus my children were growing bigger. The newer and bigger car become a need instead of a want.

However, I still subscribe to the principle that a car is necessary only to get me from point A to point B, and most of the time, the car would be parked (either at home or at office), so an expensive car wasn’t a necessity. Hence the reason why I chose the Perodua Aruz instead of buying a more expensive model.

Q2: How Do You Plan Your Finances?

Every year, I identify my annual budget which includes my commitments, savings and wants, and try to be as disciplined as possible in terms of following it.

I don’t earn a fixed income as my main income is from the fees or commission I receive from managing my clients’ finances. For those months where I do happen to have excess in terms of income, I generally would allocate most of the excess to my savings / investments (just in case I don’t make enough in the following month).

I do spend quite a bit on two things in general:

- Food (my late father’s advice to me – don’t be calculative with your family in terms of what they want to eat – provided you can afford it). This includes the occasional Wagyu Yakiniku meals for the whole family.

- Travelling (with the exception of last year due to Covid) – we do travel abroad quite a bit, but we don’t spend as much as people think on our overseas travel. I’ve shared some of my travel tips to some of clients who can vouch for them (if you know who they are)

One of the main reasons I can afford to spend on the two items above is due to the choices I make on my transportation.

Instead of paying RM 3,000 per month for a luxury car, I personally feel that it is more important for my family and me to spend the extra money on the things we really appreciate.

Q3: How Do You Save and Invest?

Apart from my emergency savings, I generally do regular savings in different investment instruments such as Unit Trust, Exchange Traded Funds, etc.

However, instead of managing my investments myself, I generally leave it to professional fund managers as I don’t have the time to manage it on my own. I trust the fund managers will do a great job. Likewise, I also choose these professional fund managers to manage my own client’s investments as well.

Q4: What is Your Financial Tip for All Malaysians?

Personal finance is not as complicated as you think. Basic concept is spending less than what you earn; do that and you should be on the right track moving forward.

I have survived when I was earning less than RM 2,000 per year, and my habits helped me to push through when I had to start back from RM 0 when I decided to change my career into the financial services sector back in 2015.

By making the right decision, you can slowly and surely get your financials on the right track.

Follow @RafiqHidayat: Facebook, Twitter, Linkedin

Do you have any stories on how you ride? Share with us in the comments section below.

“How I Plan” is a series focusing on personal stories by licensed financial planners and Malaysians. If you have a story you would like to share, get in touch with us so we can document it.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment