Having trouble choosing robo-advisors? Need help in learning what to look out for in a good robo-advisor?

The popularity of robo-advisors continues to grow with the advancement of technology, putting a spin on traditional means of choosing investments. After all, doesn’t it sound amazing to use AI and machine learning to make investment decisions instead?

In case you have been wondering, let’s start with: What is a robo-advisor? A robo-advisor is a digital platform that provides automated, algorithm-driven financial investment and planning services to investors. Upon joining, you will be asked a few questions about your financial situation and goals and the platform feeds this data into its machine algorithm to compute the appropriate investments you should look at in order to achieve those goals.

In Malaysia, there are four known robo-advisors, all licensed by the Securities Commissions Malaysia (SCM).

In this article, we look at all four and compare between them.

Contents

Table of Comparison for the Robo-Advisors

| Comparison | StashAway | MYTHEO | Wahed | Akru |

|---|---|---|---|---|

| Launch Date | 2018 Nov | 2019 June | 2019 Oct | 2020 Aug |

| Assets Under Management (USD) | $1b (including money market) | $650m | $39m | Undisclosed |

| Investment Philosophy | Invest based on data, not feelings. High returns doesn't mean high risk. | Freedom for client to choose his or her own portfolio allocation or let MYTHEO handle it. | Islamic, Halal, and ethical Investments. | Owning shares is best for long term. Diversify through businesses, country and other asset classes. |

| Investment Strategy | Allocate investment assets according to economic cycles. Protect against abnormal market behaviour. | Long-term investment. Diversification mainly through Exchange Traded Funds. | Diversify across sukuk and Islamic bonds also. Focus in Malaysia and US stocks, sukuk, and gold. | Allocate more equities for high risk portfolio, and more bonds for low risk portfolio. |

| Risk Profile | Protective to Aggressive | Very Low to Very High | Very Conservative to Very Aggressive | Low-Risk (Conservative) to High-Risk (Growth) |

| Portfolio Choice | 9 (Core) + 3 (Higher risk) | 228 + 3 (100% weightage) | 6 + 1 (Gold) | 10 |

| Investment Vehicles | ETFs | ETFs | ETFs + UTs | ETFs + UTs |

| Historical Returns (% p.a.) | -1.0% to 18.9% | -2.7% to 16.2% | 1.4% to 18.8% | 2.2% to 12.5% |

| Sharpe Ratio | 59% to 102% | Undisclosed | 34% to 54% | 55% to 87% |

| Annual Management Fee / Other Fees | 0.2% to 0.8% No hidden fees Free withdrawals and transfers. | 0.5% to 1.0% No hidden fees Free withdrawals and transfers. | 0.39% to 0.79% No hidden fees Free withdrawals RM1 for direct debit transactions | 0.2% to 0.7% No hidden fees Free withdrawals and deposits. |

| Suitable for Who? | While beginner friendly, it is suitable for even seasoned investors who believe in economic cycle-based asset allocation | Investors who want to have more customisation on portfolio allocation and/or higher exposure to Asian market | Beginner friendly especially for Muslim investors looking for a halal investing platform | Investors who have smaller amounts to invest or desire higher exposure to US market |

| Minimum Investment / Balance | RM0 | RM100 | RM100 | RM0 |

Note: Historical returns are annualized from launch date and based on data as of end of Feb 2021.

![]()

StashAway

StashAway was the first robo-advisor in the Malaysian market. Founded in 2017 in Singapore, and it then expanded to Malaysia in 2018. StashAway has recently hit its mark of managing $1bn (RM4.1bn) in assets.

StashAway was founded by Michele Ferrario, Nino Ulsamer, and Freddy Lim. Michele believed there was a way for investments to be personalized and cost-efficient. Nino brought in his experience with robo-advisory. Freddy, with 20 years of experience managing funds worldwide, manages the data-driven investment framework.

Investment Philosophy/Strategy

StashAway commits to data-driven investment decision-making. It uses Artificial Intelligence (AI) algorithms to decide on its investments and asset allocations (how much to put into stocks, bonds, etc). This takes away most of the human element in the investment decisions, believing that this is the best way for minimising your risk while maximising your returns.

Daily, StashAway verifies whether your portfolio needs rebalancing and will carry out rebalancing work for you.

StashAway is big on diversification, and as such it diversifies according to economic cycles. For new investors, what this means may be difficult to grasp fully.

Management

Freddy Lim as the Chief Investment Officer (CIO) is key. He has an established track record in the investment industry working with big names such as Nomura (as Managing Director, Global Head of Derivatives Strategy), Millennium Capital Management, CitiGroup, Morgan Stanley, Merrill Lynch, and Lehman Brothers.

Returns and Risk

Depending on the risk profile and portfolio that you choose, historical returns range from -1.0% to 18.9% p.a..

Ease of Use

Accessibility: Has both a website and a mobile application. Can set standing instructions.

Signing Up: The sign-up process is fast (under 5 minutes) and pretty painless. By answering their questions, you will be providing your basic details and identifying your risk level. From there, StashAway recommends a suitable investment portfolio for you. You will also need to provide your scanned IC for identity verification purposes.

Interface: The interface is very user-friendly. It is easy to access new portfolios that you want by just clicking on “+ New Portfolio”. Once you have done so, you can check out the asset allocation of the portfolio by asset category, country, and even individual investments.

Amount of Portfolios/Goals: No Limit

Learning Curve: The learning curve is ideal for those new to robo-advisors.

There are generally two broad categories of investment, General and Goal-based investments.

- General: Adjust your risk levels and StashAway will recommend portfolios that suit it.

- Goal-based: Select intuitive financial goals (e.g. Retirement, Education). Then, you either opt to answer questions for StashAway to compute how much you need, or you can head directly to recommended portfolios. StashAway will compute monthly what you need in order to stay on track to achieve your selected Goal.

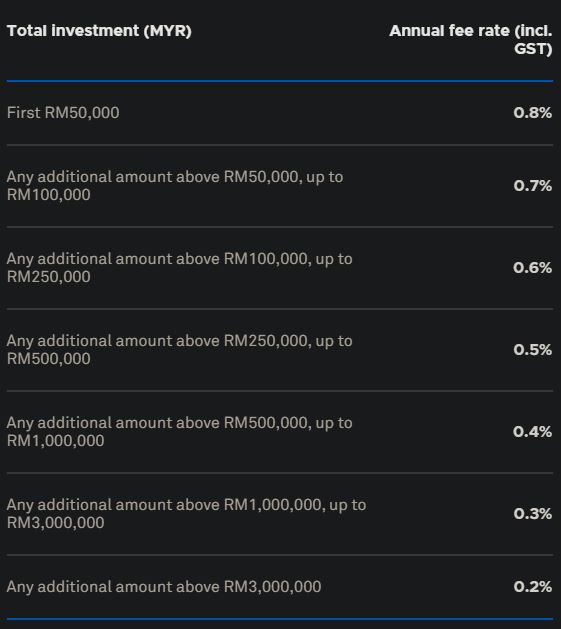

Pricing Structure

Cost and fees of using StashAway are quite competitive to other robo-advisors in the market. There are no hidden fees, and they charge 0.2% to 0.8% depending on the investments that you put in. Additionally, they also offer StashAway Simple, a money market fund which charges no management fee.

Below is the tier pricing for StashAway:

(Image courtesy of StashAway)

Verdict

StashAway is a solid choice all the way from new investors who are looking to start on their investment journey to investors who want a hassle-free way to invest globally into ETFs while being guided by an investment framework based on economic conditions. It is user-friendly and provides you with information that most investors will need. Its cost is competitive in the industry with no hidden fees. However, its investment process and strategy is more technical to the layman out there, and lacks the level of customization that some investors want to have.

![]()

MYTHEO

MYTHEO is the Malaysian robo-advisor of the Japanese robo-advisor THEO. THEO launched in Japan in 2016, making it the most established among all the robo-advisors in this list. Together, MYTHEO and THEO currently manages USD$650m in assets.

After its success in Japan, MYTHEO partnered with Silverlake Group, who has over 30 years experience in the financial markets in Malaysia and Asia, to cater to Malaysian investors.

Investment Philosophy/Strategy

MYTHEO utilises Artificial Intelligence in its investment processes and has even won the 2019 awards on Fintech Robo-Advisory and Artificial Intelligence for Asia Pacific ICT Alliance and Selangor Information Technology and Digital Economy Awards.

In terms of rebalancing, MYTHEO does this monthly and according to the target allocation set by you. It will also rebalance whenever you change your target allocation.

MYTHEO focuses on long-term investments for its investors, and diversifies mainly through Exchange Traded Funds (ETF). It believes in providing freedom for its clients where MYTHEO will tailor and recommend portfolios (Omakase i.e. leave it to MYTHEO) or let its clients adjust their portfolio accordingly.

MYTHEO has the largest number of ETFs and portfolios which are divided into 3 functional portfolios: growth, income and inflation respectively which you can have anywhere from 0% to 100% weightage in each functional portfolio. This allows for up to 231 possible portfolios. The inflation portfolio as well is the most diversified going beyond just gold but into other commodities, inflation hedge bonds and REITs.

Management

In terms of management for the Malaysian operations, their Chief Investment Officer, Malcolm Schreiber, is key. Malcolm is responsible for the development of all investment algorithms and portfolio management. He has held portfolio management and risk management positions at Mitsubishi-UFJ Investments, Asuka Asset Management, and Nomura Securities International. Another key person is Malaysian portfolio manager Amirudin Hamid who has fund management background including with Amundi Asset Management and Permodalan Nasional Bhd (PNB).

Returns and Risks

Historical returns for MYTHEO range from -2.7% to 16.2% p.a..

Ease of Use

Accessibility: Has both a website and a mobile application. Can set standing instructions.

Signing up: The registration process is very smooth and straightforward. MYTHEO recommends you a portfolio while asking you only for basic details.

There is a minimum RM100 deposit which takes about 1 business day to process.

Interface: MYTHEO has a simple interface that is very user-friendly. You can easily invest in new funds by creating new portfolios and viewing the individual asset holdings

Amount of Portfolios/Goals: Maximum 6 selecting out of 228 + 3 (100% weightage) Growth, Income and Inflation portfolios

Learning Curve: The learning curve here is just nice whether you are new or experienced. Either you let MYTHEO recommend a portfolio for you (perfect for new investors) or you create your own portfolio and adjust the asset allocation of your portfolios (experienced investors).

Pricing Structure

MYTHEO charges annual management fees of 0.5% to 1.0% depending on the amount of investment, which is higher than the other 3 robo-advisors in this list. It also requires a minimum balance of RM100.

MYTHEO’s pricing structure favours high net worth individuals more with their high cost and even then, 0.5% rate for investments over RM1,000,000 is the highest among the other robo-advisors here too.

(Image courtesy of MYTHEO)

Verdict

MYTHEO is backed by established robo-advisor THEO which has been operating in Japan since 2016 although it Malaysian operations retains independence. You have the freedom to let MYTHEO recommend you portfolios or do it your own so it suits both new and experienced investors and has the largest choice of portfolios and customization. However, its pricing structure is on the higher side.

![]()

Wahed

Wahed started in 2017 in the US as the world’s first Islamic robo-advisor. It then expanded to the UK in 2018. Its US fund currently manages around $38.6m in funds, which is much smaller comparatively to other robo-advisors in this list.

Wahed launched its Malaysian operations in 2019, with plans to use Malaysia as its Southeast Asian regional base, which is a smart move since Malaysia is the biggest Islamic finance market in Southeast Asia.

Investment Philosophy/Strategy

Wahed invests in Islamic assets around the world. It focuses on providing investments that are halal for Muslims. Wahed diversifies in Malaysia and US stocks, sukuk, and also gold. The higher risk you take, the higher the allocation for US stocks and lower for sukuk.

It is uncertain whether Wahed utilises Artificial Intelligence in its investment processes. It mainly uses Modern Portfolio Theory to optimise and manage your portfolios.

In terms of rebalancing, it is unclear how frequent this is. Wahed will rebalance when there is a significant change in your risk profile that impacts your investment goals and major movements in market volatility. There is some amount of subjectivity to movements in market volatility here as it ultimately depends on the fund manager’s judgement.

Management

The people behind Wahed do appear to carry credibility. The board consists of many notable figures that have worked for Goldman Sachs, McKinsey, PWC, and Ernst and Young. Its investment committee consists of investment professionals who have worked for JP Morgan, Google, HSBC, and NBK Capital.

Returns and Risk

Wahed has generated 1.4% to 18.8% p.a. in returns depending on your risk profile. You can adjust the risk preference by choosing the type of portfolios ranging from Very Conservative to Very Aggressive.

Ease of Use

Accessibility: Only mobile application. No website. Can set standing instructions.

Signing up: The registration process is straightforward. You will be asked for your basic details and your risk preferences.

You may encounter slow processing speed as you move through stages in the signup process. Also, be sure to do this in a well-lit area as you will be asked to take clear photos of the front and back of your IC with your phone.

After you initiate a deposit (minimum of RM100) into your Wahed account, you need to wait 1 to 2 business days for the transfer to complete before you can begin investing.

Interface: You can view portfolios’ details through the “My investment account” section in the “Account details” from the main menu. It was not that user friendly to view the assets breakdown as you need to go through multiple clicks before finding it.

Amount of Portfolios/Goals: Multiple (but with RM2.50 min fee/annual fee whichever higher for more than 1 account) selecting out of 6 (very conservative – very aggressive) + 1 (gold) portfolio choices.

Learning Curve: The learning curve is rather level. Set a financial goal in the app and answer a series of questions for Wahed to recommend a portfolio for you. To change your portfolio risk, you will need to submit an application.

Wahed is goal-based and provides users with 4 options: Retirement, Long-term Savings, Short-term Savings, and Major Purchases. While you can later specify what the portfolio is for (e.g. education, wealth-building), Wahed does not ask you any specific questions regarding those goals.

Pricing Structure

Wahed sets annual management fee ranging from 0.39% to 0.79%. 0.79% charged for investments between RM100 to RM499,999 and 0.39% is charged for investments more than RM500,000.

While Wahed is the only Islamic robo-advisor in the market so it has no direct competitors to compare with, Wahed stands out from among the other robo-advisors in this list for pricing that is less competitive, especially for investors with smaller capital.

Verdict

Wahed is the only Islamic robo-advisor for Malaysians wanting to invest in Islamic assets while adhering to Islamic investing principles.

However, Wahed a more expensive pricing structure, a minimum deposit requirement of RM100, and a mobile application platform which while straightforward does lag.

![]()

Akru

Akru is Malaysia’s first home-grown robo-advisor. Founded by Tan Chong Liong and Julian Ng, it currently only operates in Malaysia. The total funds it is managing now is unknown.

Akru began with Julian wanting to create cost-effective and accessible investing for retail investors. He teamed up with Tan Chong Liong and formally established Akru’s portfolios in 2020.

Investment Philosophy/Strategy

Akru has a stronger focus on long-term investments, and believes in diversifying across businesses, regions, and other types of investments. It identifies equities as the key driver for returns in the long term., but advises a combination of both equities and bonds in your portfolio. The higher the risk you take, the higher the allocation it is for equities.

It is to be seen how much Akru utilises Artificial Intelligence in its investment processes as its white paper mainly talks about applying modern finance theory and practice to produce standard portfolios for different risk levels.

Akru has two types of rebalancing – soft and hard. Soft rebalancing involves allocating new deposits accordingly to balance your portfolio. For hard rebalancing, Akru will buy and sell your assets in your portfolio to get your target allocations back on track.

Management

Akru’s pivotal figures are Julian Ng as Chief Advisor and Tan Hui Koon as Chief Investment Officer.

Both have very rich experience in the Malaysian financial industry. Julian has worked for CIMB, JP Morgan, and Public Mutual. Hui Koon has over 20 years of experience in the financial advisory and the investment management fields.

Returns and Risk

Historical returns range between 2.2% to 12.5% p.a. from Akru depending on your risk preferences. Risk preferences are determined by 5 sample portfolio’s risk and returns, your selected financial goal, and your answers to questions posed by Akru.

Ease of Use

Accessibility: Only available through the website. No mobile application. Can set standing instructions.

Signing Up: Sign up for Akru using your Google account and it immediately takes you to your Akru dashboard. You will need to supply your personal details and verify your IC.

One frustrating point to note is your date of birth cannot be keyed in. Instead, you will have to scroll through month by month. This process added at least 2 minutes to an otherwise smooth process that should ideally only take 3 minutes.

Interface: The interface is very user-friendly. To invest, select “Goals” and answer the prompted questions for Akru to recommend a suitable portfolio for you. It shows what are the equities and bond investments allocations that each will have.

Amount of Portfolios/Goals: No limit selecting out of 10 portfolio choices grouped into (Low-Risk Larry, Moderate Mary and High-Risk Harry).

Learning Curve: The learning curve is good for those new to robo-advisors.

Akru is goal-based and you can select 3 Goals and 1 general. Akru does not explicitly allow you to choose portfolios but rather allows you to choose portfolio risks. After selecting your Goal (e.g. Retirement, Education) and choosing your portfolio risk, Akru will calculate how much you need and recommend a suitable portfolio. The process is driven by you answering questions.

Bear in mind that some of Akru’s questions are “deep”, such as the cost of inflation for education or the projected increase in your salary. There are recommended numbers suggested, but it would be better if you can set aside time to do your own research first.

Pricing Structure

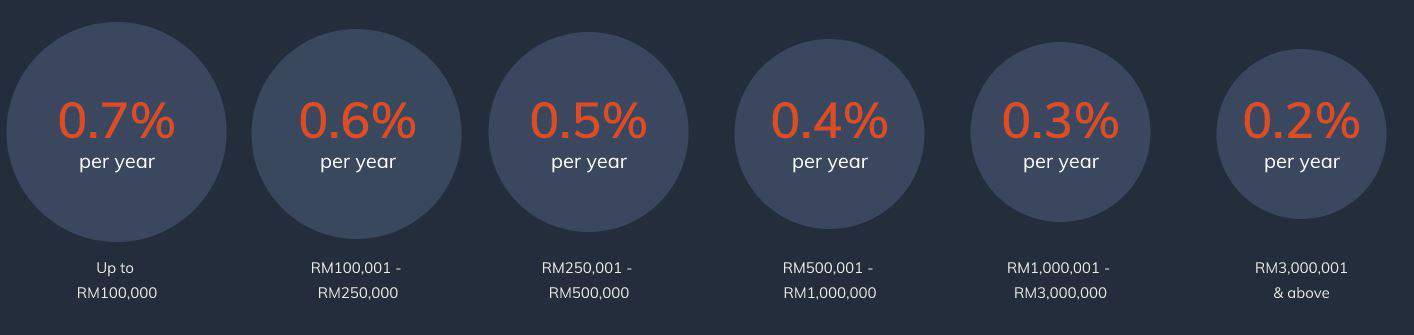

Akru charges no hidden fees and an annual management fee of 0.2% to 0.7% depending on the amount of investment.

It does have a competitive edge in the market for lower income investors as it charges the lowest rate of 0.7% for capital below RM100,000. Withdrawals and deposits are free, and there are no sales charges.

Below is how Akru prices for its services:

(Image courtesy of Akru)

Verdict

Akru is a decent robo-advisor choice for first-time robo-advisor investors and for those who have lower amounts of initial capital.

Its 0.7% annual fee is the lowest for people who have funds less than RM100,000 and will benefit many retail investors. However, there is less flexibility in the number of financial goals one can set and some questions during the sign-up process would need some form of prior research to answer. Also the wait for an app version of Akru may discourage some investors.

Conclusion

There are several things that you have to consider when choosing an appropriate robo-advisor. If you want simplicity, a well-designed app and asset allocation based on economic regimes, StashAway may be suitable for you. If you are looking for the lower starting fees while remaining relatively simple, one can consider Akru. If you are looking to have more control and portfolio customisation, MYTHEO might be a better choice for you. For investors prioritizing ethical and halal investing, look no further than Wahed.

Past performance is not indicative of future performance. Remember, its not just returns that you are concerned about, it is also the quality of the management team behind the robo-advisors. This aspect of it is more subjective and requires experience and sound judgement.

Which robo-advisor(s) are you using and why? Let us know in the comments below!

You May Also Like

- Personal Finance Promotions (including Exclusive Robo Advisory Signup Links)

- Introducing Malaysia’s First Robo Advisory, StashAway

- Wahed Invest Review: Malaysia’s 1st Islamic Robo Advisory

- Harnessing Calmer Times to Make Good Investments

- How to Diversify Your Investments

- StashAway Assets Under Management Surpasses US$1b

{kind=link}

{kind=link}

Leave A Comment