Want to know a cheaper and easier way to invest in bonds?

Bonds have traditionally been an asset class that is taken up mostly by institutional and more sophisticated investors in the market. Retail investors are typically unable to invest in bonds due to the lack of accessibility and the high amount of capital needed. After all, bonds are normally traded in denominations of US$200,000 per bond, which is out of reach for most retail investors.

Simply put, a bond is an investment that generates consistent coupon returns to you. Think of it as an IOU that you buy from the government or companies. When the bond matures, you get back the principal amount, along with whatever coupons you have earned throughout the bond duration. We explained more about what exactly bonds are in a previous article. Be sure to check it out!

Contents

Lack of Access to Bonds in Malaysia

In Malaysia, most corporate and government bonds are catered towards the ultra-rich or the institutional investors who have deeper pockets and greater sophistication. In fact, retail participation in the Malaysian bonds market has been lackluster and regular investors face significant roadblocks and high fees due to the dominance of institutional investors. Bond issuer’s incentives tend to be focused on serving institutional investors, where they get preferential rates to incur lower costs if bond lot sizes are larger at RM10m.

As a matter of fact, most banks in Malaysia don’t offer direct access to individual bonds to regular investors. This is because a lot of money is required to even meet the minimum transaction amount of individual bonds, which is typically around RM250,000 or RM500,000 per transaction. Hence, most investors can only invest in bonds through alternative structured products where the amount of capital needed is much lower.

An example of such a structured product marketed by banks is bond funds. With bond funds, you do not have any say on the specific bonds you want to invest in. The bank will invest on your behalf in the bond market according to the fund’s investment philosophy and objectives. While this may sound like a good idea for the uninitiated, bond funds typically incur hefty fees for the investor. Most of the time, you would not even be aware of how these fees are charged, as they can be complex to understand. Such fees and charges include:

- Sales Charge

- Redemption Charge

- Switching Fee

- Annual Management Fee

- Annual Trustee Fee

In today’s highly digitized society, does it make sense to still be paying such fees? These fees can potentially add up to 1-2% of your investment. It may not sound like a lot, but if your bond yield is between 3-4%, that’s almost 50% of your returns paid towards fees!

What if you just want to purchase individual bonds? There are options, but first, you must have at least RM250,000 or RM500,000 available for each bond you want to purchase. A typical Malaysian household earns RM62,508 a year (median monthly income: RM5,209). Assuming that you save 30% of your income, it will take 13 years for you to save up just to even afford a bond at the minimum transaction amount of RM250,000. For ordinary Malaysians, this is a significant portion of their income and is simply unfeasible to build a properly diversified portfolio.

So, Where Can You Buy Bonds?

For investors in Malaysia, you can purchase individual bonds through a few platforms such as Bursa Malaysia’s Exchange Traded Bonds and Sukuk Platform and iFAST Capital’s FSMOne Bond Express. However, investors should be aware of the significant fees and charges that are charged by some platforms on top of the USD200,000 high investment minimum required.

For example, a bond platform charges mainly two types of fees – Processing fee and Platform fee. The processing fee ranges from 0.1% to 0.5% of the nominal value with a minimum of RM35 or in equivalent currency (USD35, SGD35, AUD35, etc.), while the bond platform fee per quarter ranges from 0.02% to 0.045%. Typically, the lower fees tiers are offered only to investors purchasing at least RM10million and above. In addition, bonds offered on may also have a spread of 1% to 2% built into the selling price of the bond, further increasing the cost of ownership. All these fees add up to quite a significant amount.

CapBridge, a Singapore Exchange-backed digital wealth management platform is aiming to change that. With lower fees and a lower investment minimum of just $1,000, investors can now access institutional-grade bonds at the convenience of their home. Keep reading to find out how this is done!

Improving Access to Bonds through Fractionalization

One way to improve access to asset classes that have traditionally had high minimums is through fractionalization. Fractionalization refers to portions, livers, or slices of asset classes that are smaller than a whole share. This means that if an investment costs RM10,000 per share, you can actually purchase it from as little as RM100 when the share is fractionalised. You don’t have to buy the entire share.

This has revolutionised the way assets are being bought and sold in the market, improving access to retail investors who may not have the capital required to invest in certain investments. This is particularly useful for portfolio diversification, since investors can now purchase multiple shares for the same amount of money. This is already available in equities, where retail investors are buying fractionalised shares of multiple companies at an affordable cost to diversify.

In that context, what if bonds can be fractionalised too? Won’t that be great for you?

![]()

Lower Fees, Lower Minimums

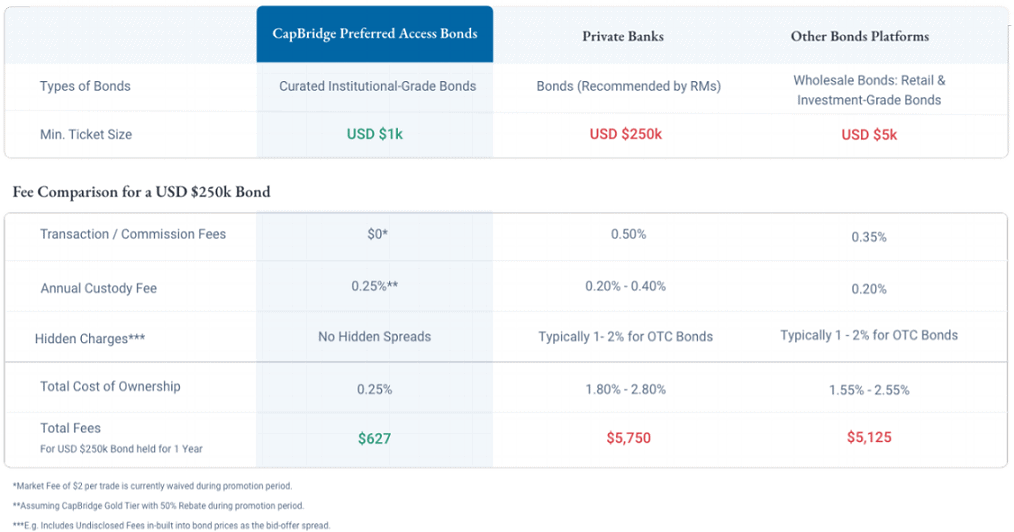

This is exactly what CapBridge, a digital wealth management platform headquartered in Singapore is doing. Their fractionalized Preferred Access bonds allow investors to invest in bonds from as low as $1,000. That is 200 times lower than typical bond investment minimums! For an asset class like bonds, this is one of the lowest minimums currently available in the market. By making bond ticket sizes smaller, CapBridge significantly lowers the barrier of entry, making bonds more affordable for more people and increasing the ability for regular investors to access this asset class to diversify their portfolio.

CapBridge’s fractionalized Preferred Access bonds work exactly like regular bonds. After purchasing a bond, investors will receive their coupon payouts as usual. Upon maturity, the principal amount will also be returned directly to an investor’s account. In fact, with a fully digital platform, the process is even faster and more hassle-free than traditional banks.

The fee structure at CapBridge is fully transparent and easy to understand. With an annual fee of just 0.25 – 0.5% and trading fees waived until further notice, CapBridge is definitely one of the cheapest ways to purchase bonds in the market right now.

Experience a fully digital end-to-end platform, with transparent bond prices and no additional fees or hidden 1% to 2% spreads typically found in private banks and other bond platforms. Have full control of your investments anytime, anywhere. Access to CapBridge is absolutely free. All you have to do is to sign up and complete a simple investor verification – that’s it. Now, everyone can invest in bonds.

Interested to start? To find out more about CapBridge’s Preferred Access Bonds, visit their website here.

From now till 31 December 2021, investors get to enjoy up to 50% rebate off fees when you invest in bonds through CapBridge. Invest from as low as $1,000.

CapBridge is licensed by the Monetary Authority of Singapore and holds a Capital Markets Services license. Strategic shareholders include the Singapore Exchange, SGInnovate, and Hong Kong government-linked Cyberport Macro Fund.

{kind=link}

{kind=link}

Leave A Comment