Can bonds help secure a solid financial future for you and your family?

Many Malaysians do not think of bonds when it comes to growing their wealth, often due to a lack of knowledge on what bonds are, or simply lacking the ability to access bonds because their income or status do not qualify for it.

If you are one of them, fret not as we have recently published articles explaining what bonds are and how it’s now easier (and cheaper) to invest in bonds. Be sure to check them out!

In this article, we tackle the next question you will likely have after reading the first two articles, which is – why is it important to invest in bonds?

Contents

Making the Most Out of Your Money

When it comes to managing and growing your wealth, it boils down to two fundamental objectives:

- Making your money grow in value over time, and

- Making sure your money doesn’t lose its value over time.

The first objective is obvious – everyone wants to grow their money. The second objective though, is equally important and is one that may get overlooked by inexperienced investors. In general, money that is left idle loses its value over time. Not doing enough with your money also causes it to lose value over time. There are a couple of factors causing this. Let us explain.

In the world today, there is a relentless force that is eroding the value of money and its purchasing power – inflation. In its most basic definition, inflation is simply a general increase in prices. Everything gets more expensive. Consequently, that means that the current value of your money also drops. Take this example. Let’s assume an annual inflation rate of 3%, meaning that prices of goods and services increase by 3% every year. Something that costs RM100 this year will cost RM103 in the next year. To put it in a different way, this means that your RM100 this year will only be worth RM97 next year. Project a 3% inflation rate over the course of several years, and you can see that the value of your money severely weakens.

Going hand in hand with inflation is the cost of living, and it is going up. Cost of living is typically determined by the consumer price index, which measures the prices of a basket of goods and services commonly purchased by Malaysians. From 2015 to 2019, consumer price index growth averaged around 1.9%, However, latest data show that the consumer price index growth for Q2 of 2021 has increased to 4.1%, which is an all-time high since Q1 of 2017!

Considering these two factors above, we can see that there is a need to be able to make your money work harder and grow in value over time. Besides bank accounts and fixed deposits, are there any other alternatives that are equally as easily available and accessible?

CapBridge, a Singapore registered and regulated digital wealth management platform, has recently launched their latest asset class – CapBridge Preferred Access Bonds. With bond yields of up to 9%, now you can make your money work harder and smarter for you. Read on to find out more.

Where Do Malaysians Typically Put Their Savings In?

Generally, most Malaysians store their money in two ways – bank savings or fixed deposits.

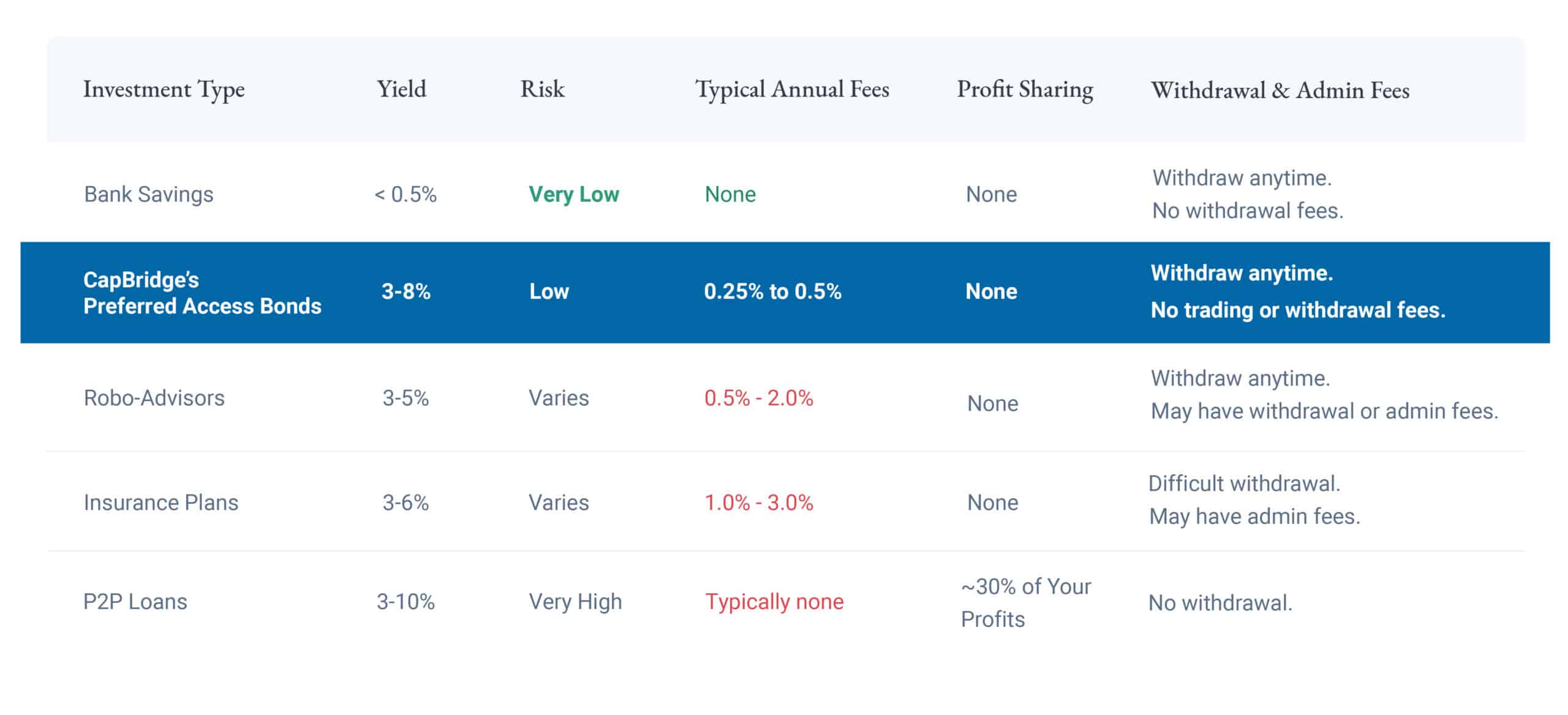

Most people would be familiar with a bank savings account. Yet, with a miserly annual interest rate of between 0% to 2%, this is one of the most ineffective ways of safekeeping your money. In fact, given prevailing inflation rates, simply keeping your money in a bank savings account is a guaranteed way to make your money lose value over time.

Fixed deposits are another popular option for safely growing money. Investors deposit their money with a bank for a fixed period of time, earning a predetermined interest rate. During the term of the fixed deposit, the money is ‘locked up’ and cannot be withdrawn. At the end of the duration, the full sum of money is released, along with the interest generated from the fixed deposit. This sounds stable and fuss-free, but interest rates of fixed deposits vary depending on the duration and the deposit amount. Typically, higher deposits offer higher interest rates but with longer lock-up periods, while smaller deposits will receive less interest returns and a shorter lock-up period.

Lack of Good Alternative Options

What about other alternatives such as robo-advisors or P2P lending platforms? Promising higher interest rates and shorter-term lock-ups, these platforms may seem like good alternatives, but not all that glitters is gold. Let’s take a closer look at these alternatives.

Robo-advisors have been on the rise in recent years. Using computer algorithms to manage your investments, they claim to be able to deliver high returns with low fees. But are the fees really low? No! With annual fees ranging from 0.5% – 2%, not including other fees like withdrawal fees, trading fees and trailer fees, all these fees add up to a significant amount. Furthermore, many robo-advisor platforms offer products that are a mix of different asset classes, increasing your risk-exposure to other asset classes that may not be suitable for investors looking for a flexible investment time-frame. For investors looking for a safe place to store and growing their money consistently, robo-advisors are simply not a good choice.

Peer-to-peer (P2P) financing has been around in Malaysia since 2015 and has raised RM1.14bn for companies since 2017. P2P financing is a sort of short-term investment where investors lend money to small companies at high interest rates. Such companies go to P2P financing platforms to borrow money because they lack the credibility or scale to secure financing through traditional channels like a bank. As a result, they offer high interest rates to entice investors to lend money to them. The interest returns are high, but the risk of default is also very high. Think about it. Would you lend your money to an unknown company which a bank may have rejected? In addition, P2P financing platforms tend to include some form of profit sharing for your investments. This means that a portion of your profits will be shared with the platform, sometimes up to 30%! While P2P financing may offer high interest rates for investors, they are not ideal for investors looking to grow their money stably and consistently.

All these existing options seem lacking, but have you considered bonds?

![]()

Make Your Money Work Harder and Smarter for You

Bonds are a secure type of investment suitable for investors looking to grow their money stable and consistently. In fact at CapBridge, their Preferred Access Bonds lets you make your money work harder and smarter compared to the other options discussed above. With bond yields ranging from 2.5% to 9% for US-dollar bonds and 3% to 5% for Singapore-dollar bonds, CapBridge’s Preferred Access Bonds allow you to enjoy higher risk-adjusted returns compared to traditional bank savings or fixed deposits.

Bond investments typically come with high fees and multiple hidden layers of charges. Not at CapBridge. Enjoy lower fees and more transparent prices compared to traditional brokers and banks. Pay only a single annual fee starting from just 0.25% – no transaction fees, no commission fees and no hidden spreads. Unlike other platforms, there are also no trading or withdrawal fees, which means you can withdraw your funds anytime without having to worry about incurring additional costs. This provides you the assurance that your money is working harder for you, with lower fees and costs.

Through CapBridge’s fully digital platform, you can view all the bond offerings at one glance on a single dashboard. CapBridge offers a curated selection of institutional-grade bonds from publicly listed Fortune 500 companies, including bonds from familiar names like Maybank, HSBC and UOB. You now have the power to choose how you want to diversify your portfolio according to your investing style and risk preferences. Make your money work harder and smarter for you today.

Interested to start? To find out more about CapBridge’s Preferred Access Bonds, visit their website here.

From now till 31 December 2021, investors get to enjoy up to 50% rebate off fees when you invest in bonds through CapBridge. Invest from as low as $1,000.

CapBridge is licensed by the Monetary Authority of Singapore and holds a Capital Markets Services license. Strategic shareholders include the Singapore Exchange, SGInnovate, and Hong Kong government-linked Cyberport Macro Fund.

{kind=link}

{kind=link}

Leave A Comment