Insightful perspectives on this month’s market events. The original version of this article was published on ifastcapital.com.my.

Contents

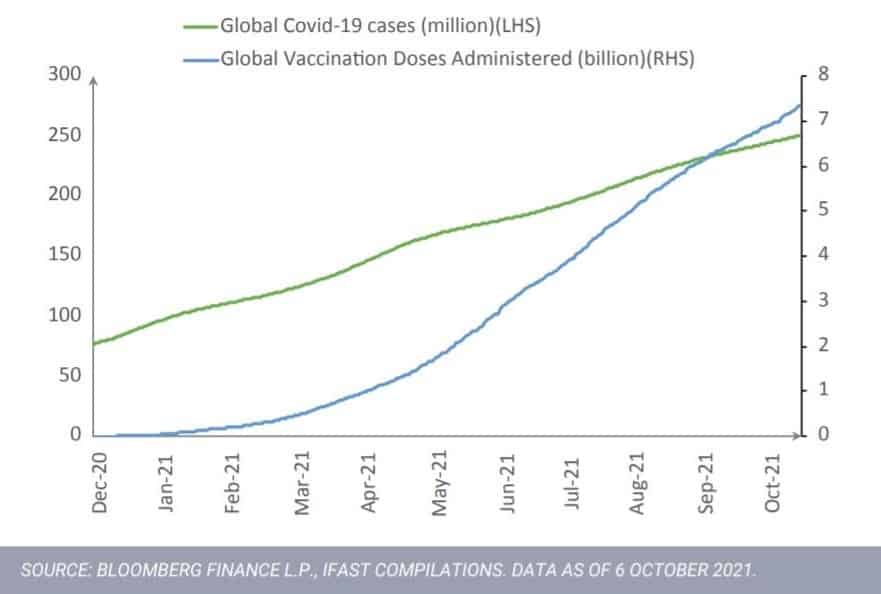

Gradual Lifting of Covid-19 Restrictions Around the Globe, Positive for Travel Recovery

Event

With rising vaccination rates around the globe, inevitably, we are finally witnessing a gradual lifting of lockdown restrictions with a rising number of countries announcing reopening of borders to fully vaccinated travelers. For example, US reopening borders to fully vaccinated tourists starting 8 November 2021, Thailand to allow quarantine free travel from 46 countries starting 1 November 2021, Indonesia cuts quarantine time for fully vaccinated foreigners to 3 days, Singapore opening its borders to fully vaccinated people from 8 countries without quarantining starting 19 October 2021 and Australian outbound international travel ban to be lifted from 1 November 2021.

Impact

The pent-up travel demand is very real with Airbnb reported a substantial increase in gross booking value as compared to 2019 levels and Marriot announced in its 3Q21 results that contract sales were back to 2019 levels while Delta Air Liners witnessed a 450% surge in international point-of-sale bookings as compared to the 6 weeks prior to the US reopening announcement and Ryanair is seeing a very strong recovery across Europe and raised its growth forecast after posting its first quarterly profit since 2019.

Opportunities/Risks

Despite concerns around labour shortages and rising commodity prices, travel recovery seems inevitable due to the strong demand after a dreadful period of lockdown restrictions restraining human mobility. Investors who share the same view on global travel recovery, can consider ETFMG Travel Tech ETF and SonicShares Airlines, Hotels, Cruise Lines ETF.

US Lawmakers Passed a Historic USD1 Trillion Infrastructure Bill

Event

The US House, controlled by the democratic party, finally passed the long-awaited infrastructure bill on 5 November 2021, after months of deadlock as the democrat party leaders were trying to get the progressives and centrists within the party with varied visions to back the bill. Unsurprisingly, the bill was passed after mounting pressure following the democratic party defeat over Virginia’s governorship to the republican party on 2 November 2021 while the US President’s approval ratings dropped to a new low of 38% in October 2021, according to a poll.

Impact

This results in new funding of USD 550 billion under the bipartisan Infrastructure Investment and Jobs Act to spend on roads, bridges, and other projects. The package provides USD 110 billion for roads, bridges, and aging highways, alongside USD 66 billion for passenger and freight rail and USD 39 billion for public transit. Both broadband access and power grid will get funding of USD 65 billion each. The legislation also set aside USD 55 billion for water systems, more than USD 50 billion to deal with cybersecurity, climate change, and extreme weather events, along with USD 7.5 billion spending on electric vehicles and its charging stations, among other things.

Opportunities/Risks

As the bill directs billions into critical infrastructure projects and provides much-needed support for the economy together with more job creation, investors who are keen to participate in this cyclical recovery can position into United Global Durable Equity Fund where it has decent exposure to the industrial sector.

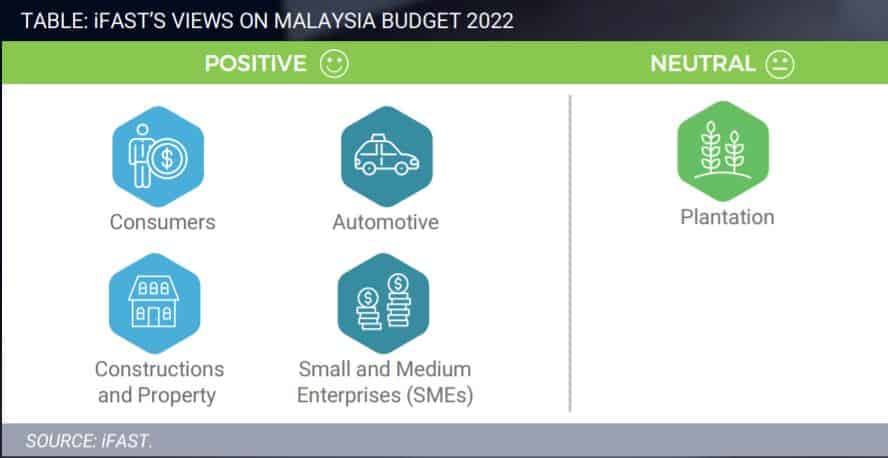

Malaysia Budget 2022, Supportive of Economic Recovery

Event

Budget 2022, which was unveiled on 29 October 2022, was highly anticipated given its significance in assisting the country in this current reopening phase, as the country is still trying to recoup from the severe Covid-19 lockdown that impacted lives and livelihood. The budget covered a lot of grounds, specifically on measures to boost employment with subsidies and programs, targeted assistance to households with less than RM5,000 monthly income, assisting small and medium enterprises (SME)s with more reliefs, funding for Health Ministry to address Covid-19, supports for school re-opening with targeted assistance to students, teachers and schools, and a significant increase (+9.5%) in development expenditure, while also addressing global issues with green initiatives.

Impact

Unfortunately, the budget wasn’t taken well by the market as both FBM KLCI and FBM Small Cap index, declined -2.0% and -0.8% respectively the week following the budget announcement, as investors were concerned on the negatives from the budget such as the one-off prosperity tax on corporates with more than RM 100 million chargeable income, the uncertainty over taxation on foreign sourced income and the removal of stamp duty cap on contract notes for trading of listed shares.

Opportunities/Risks

As the market pricing in the negatives from the budget, FBM KLCI index looks more underappreciated given it has been a laggard thus far in 2021 and the positive measures from the budget which is supportive of this current economic recovery phase bolds well for the Malaysian equity. Investors who are excited about Malaysia’s potential economic recovery can consider Eastspring Investments Equity Income Fund. As for external demand and the continued excitement towards the semiconductor sector, investors can consider Maybank Malaysia SmallCap Fund.

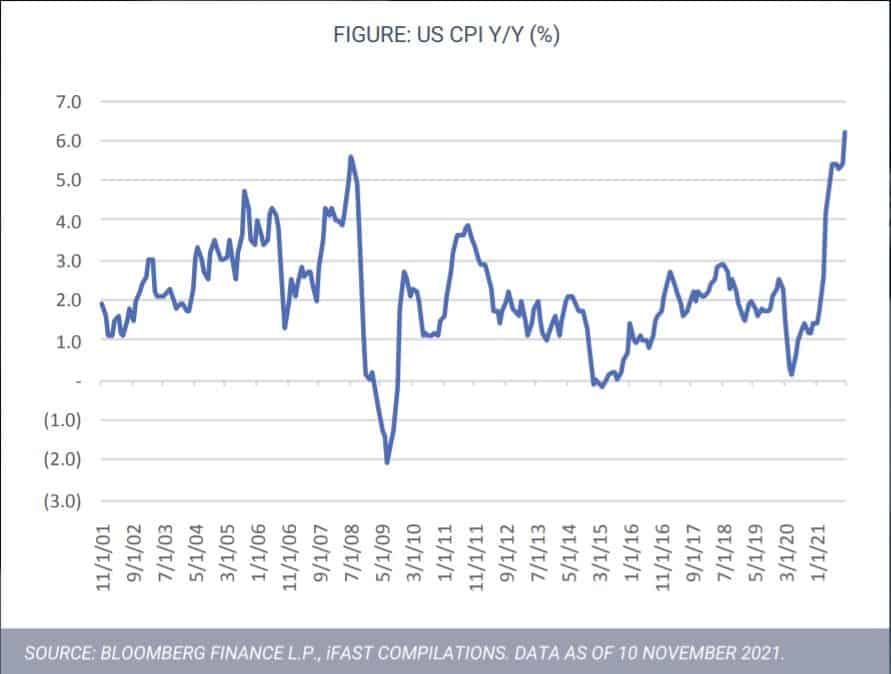

Persistently High US Inflation Remains a Key Market Risk

Event

US inflation hit a three-decade high with the latest reading came in at 6.2% for October 2021. Inflation remains a key market concern and its impacts, thus far, have been very apparent in the bond market as witnessed in the US 10-year treasury yield rising from 0.9132% on 1 Jan 2021 to a peak of 1.7404% in March 2021 on rising inflation fears. The fear was then contained especially with softening of commodity prices and the US Federal Reserve assuring markets that it is just transitory inflation.

Impact

Unsurprisingly, the recent inflation fears were also reflected in the rising US 10-year treasury yield in October 2021. While yields have subsided in early November 2021 following authorities stepping in to address supply chain concerns, we note that the US corporates in the recent results season have stressed their concerns on the current inflationary pressures and to make things worse, they intend to pass the higher costs back to consumers which could add to the upside risk on the inflation numbers.

Opportunities/Risks

As such, we continue to keep inflation risk on our risk radar as a persistent inflation pressure could change the US policymakers’ stance within the US interest rate path moving forward, bringing downside risks towards the financial markets by hiking rates earlier than expected. While generating steady income stream by investing in fixed income space, investors should consider short-duration bond funds like AmIncome Plus to mitigate one’s portfolio fluctuations.

Invest in unit trusts, PRS, EPF i-Invest funds & managed portfolios from as low as 0% sales charge with iFAST Capital by talking to your financial planner.

{kind=link}

{kind=link}

Leave A Comment