A simple parable that shows how, given time, the magic of compounding can help you very much financially!

Max and Jane have been blessed with a beautiful, healthy baby girl. They are joyful yet also anxious. Max is in his 3rd year of his career, earning just barely enough to cover their expenses and without much leftover for savings. Jane would be returning to her job once her maternity leave ended for they could not live on Max’s income alone although it is her dream to be a stay-at-home mother. While they are not starving, they are also not financially-secure. In fact, they are financially-fragile.

Let’s look at the journey Max and Jane are taking as they learn about the power of compounding so that they who began with so little can one day end up with so much.

Contents

#1: Start Saving Consistently Early On

Max and Jane knew they had to start saving very early on in their career to take advantage of the power of compounding.

In order to make compounding to work, they needed to accumulate a significant amount of savings early on to establish a strong base from which they can slowly let the forces of compounding work. At that time, they still didn’t know how exactly compounding will work but took the advice of a friend who was a financial advisor to start building that capital base (starting money) now rather than later.

To start, they chose to consider saving 20% of their income, which translates to about RM1,000 of their RM5,000 combined income.

Before they commit to it, they have to plan their budget well and the first step would be to identify their unavoidable, mandatory expenses, which were:

- 1 home mortgage RM1.5k

- 2 car loans RM900

- Groceries & utilities RM1k

These expenses did not include funds for unexpected setbacks/emergencies or for miscellaneous spending. RM1,000 for savings was possible although probably really slim especially with a newborn, who knows what sudden expenses would pop up, but they would try really hard because now they were committed to this.

A savings goal, if it’s easy for you then you are really lucky. The reality is that for many people, a savings goal takes self-discipline. Yes, sometimes Max and Jane would be frustrated because they couldn’t buy nice things, or that they had to eat simple food all the time. But they knew why they were doing this and so they supported each other and focused on making it work.

After some months, Max got a promotion and Jane increased their income streams (Jane would wake up at 4AM daily to make simple kuih which she would sell to her neighborhood nasi lemak stall who in turn would sell the kuih to customers), yet they continued to commit saving 20% of their combined income instead of sticking to just RM1,000. For months where expenses were less, they could even increase their savings threshold to 30%. It was simple but not easy to focus on meeting their needs and ignore feeding their wants.

Little by little that capital base grew. But, inflation was also growing at the same time, creeping upwards year by year. This meant that saving the money at home just isn’t enough. They needed to stay ahead of inflation. It was necessary to find an appropriate place to put their savings where it can have compounded growth. Not knowing what to do, they turned to a professional to advise them.

#2: Choosing the Right Investments

As the licensed financial advisor sat across them in the crowded Chinese kopitiam, Max and Jane sat uneasily together, staring blankly into a piece of paper that contained tens of investment funds and alternatives, strewn with numbers at 3 decimals and description that seemed Greek even to them who were university graduates.

Max and Jane still looked at Mr Chong blankly, wanting to ask some questions but not knowing where to start. Mr Chong smiled kindly and said, “That is why I am here, to help you with your investment and financial goals, and compound your savings in the long-term. Before I start telling you on how it works, we need to be clear on what we are trying to achieve 30 years down the road.” Max looked at her wife, scratched his head slightly, and turned to Mr Chong, “We wish to own a house in 2 to 3 years’ time. We are simple people, so we don’t need a house that is very big or have the most modern furniture. Education and exposure is very important, so we want to give our daughter an overseas education at least for a year or two for their university. That will probably happen about 20 years from now. For ourselves, we would want to be set for retirement by the time we are 60 years old, going on short vacations, traveling around, and spending time on our hobbies.”

A licensed financial advisor seeks first to understand your financial goals for your future, where you are financially now, and advise you on your options to consider between your now and the future state.

Mr Chong considered what Max and Jane were saying. He also considered their age. In a nutshell, he was considering that they have more of a long-term focus and that they are currently young, they can afford to invest in investments that are riskier and have longer-term investment horizons. If they can regularly contribute to the investments every month, then Mr Chong listed several investment choices Max and Jane could consider which are managed by reputable investment firms with an established track record.

Max and Jane’s nervous demeanor slowly turned more relaxed as they began to see that Mr Chong was listening closely to what they were saying and was coming up with useful advice for them to now explore one by one. The questions began to flow more easily and in earnest.

#3: How Compounding Actually Works

Mr Chong now feeling relieved also that Max and Jane are more at ease, told them that this is where the magic happens with compounding. He said, “Compounding is the key ingredient that makes it possible. Einstein once said that compounding is the eighth wonder of the world and I will tell you why shortly after. However, I need to tell you that this works only if you are disciplined in saving up your money and contributing a consistent sum every year, and you don’t take the money out for no reason. Compounding works best if you keep the money in and not out.”

Max and Jane listened with great intent but also with some degree of skepticism. Mr Chong understood their concerns on whether does this really works, and that finance and investment concepts are mainly foreign to most people on the street. He starts by saying, “Compounding is hard work, make no mistake about that. You will not see much results in the beginning as it involves a great amount of patience for the investment to slowly gather steam. I will not complicate things with financial jargon.” He went on and take out a piece of paper and drew one chicken.

Max and Jane looked a bit confused but Mr Chong went on to say, “For example, imagine if you have one chicken that lays only 10 eggs a month. You can choose to eat the eggs now. However, compounding will tell you not to eat the eggs but rather wait for them to hatch in 20 days.

Now imagine if all 10 eggs hatch and you have 10 chicks who are all female. If you wait 16 weeks for them to mature you end up with 11 egg-laying chickens. That’s now 110 eggs in a month. If you repeat the process of letting them hatch and mature, you would have even more chickens to lay more eggs.

Compounding is similar to this in that you put your money into an investment and let it generate returns for you every year. If you take the money out after one year and spend it, that is equivalent to eating the eggs and not letting them hatch and mature. The returns that you generate in one year will go back into the investment and it will then COMPOUND together with your original investment to generate even more returns the next year.”

#4: Project your Investments Through Compounding and Keep Track of It

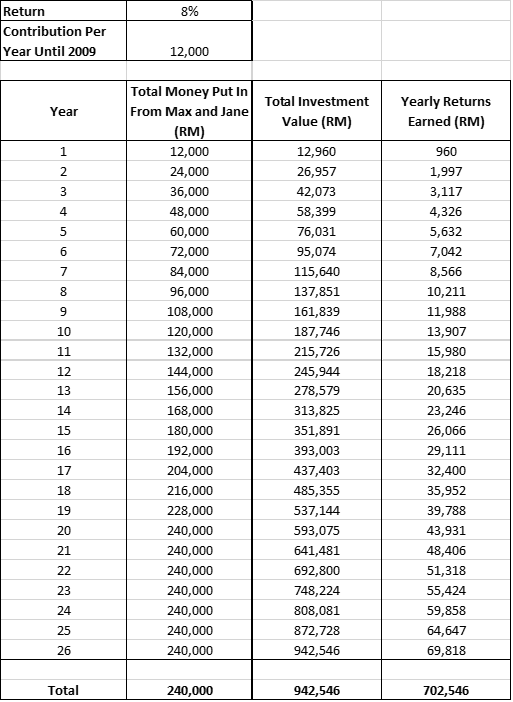

Taking Mr Chong’s advice to their heart, Max and Jane set out to decide on the appropriate savings to have every month, and the type of investments to take on. They decided on contributing RM12,000 per year for the next 20 years for an investment fund that invests in 80% stocks and 20% bonds, and they think could possibly generate about 8% in returns a year, though dependent on market conditions. For the rest of their savings, they would decide on other investment opportunities that could come later.

Jane, being the Excel wizard between the both of them, quickly rolled out a comprehensive spreadsheet, detailing how much money they will be getting down the line. This is the result.

Conclusion

With that money compounded from their investments, Max and Jane were able to put their daughter through a twinning program to go study finance overseas. They were able to buy their house and are already on their way to their retirement with enough saved up from their compounded investments to lead a comfortable life and go on their short vacations. All due to simple compounding and stable market conditions.

In this parable, our characters are super simplified versions of what happens in real life. However, the truth is that life is simple even though it is not easy. Compounding can on its own truly grow your money. Save early, and start allowing your money to grow. If setbacks happen as life throws lemons at us, it’s okay, because you would at least have something started which you can continue once you ride over that wave of bad luck.

If you don’t know where to begin in your journey towards financial independence, start with budgeting, saving, and compounding. The rest will soon quickly follow.

Interested to know more on how did Max and Jane compounded their money? Let us know in the comments below!

You May Also Like

- Calculating investment returns based on ROI, AAR, CAGR, and IRR

- Compounding to One Million Ringgit

- How do I reach 8% (and above!) returns? Contact us to find out!

{kind=link}

{kind=link}

{kind=link}

Leave A Comment