Insightful perspectives on this month’s market events. The original version of this article was published on ifastcapital.com.my.

Contents

Insights From the March FOMC Meeting Minutes

Event

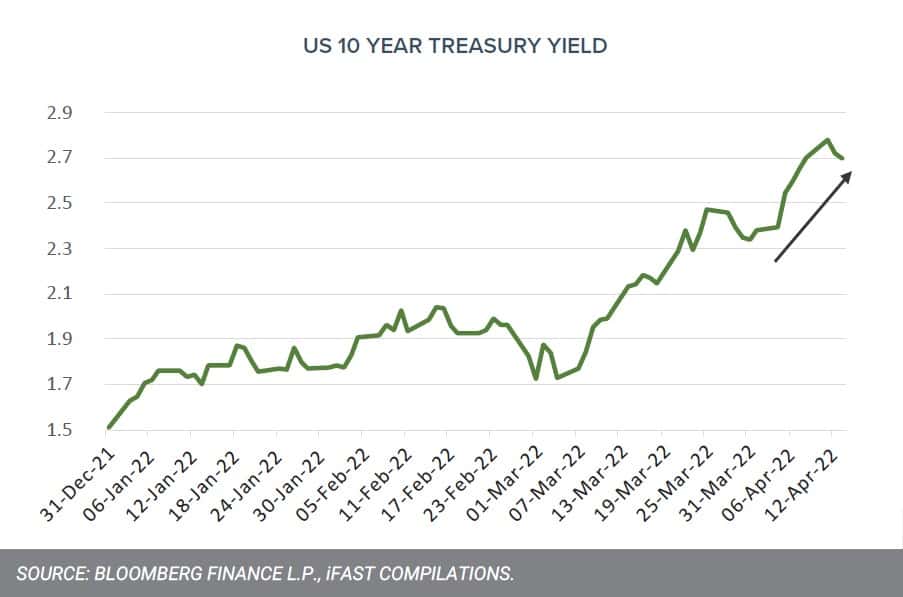

The latest FOMC meeting minutes released on 6th April 2022 was widely regarded as hawkish because it indicates that a 50-basis points rate hike is imminent in the upcoming May FOMC meeting and it also shed light on the US Federal Reserve’s readiness to begin shrinking (i.e. quantitative tightening) its USD 8.9 trillion balance sheet. As stated in the minutes, the reduction will have a monthly cap of USD 95 billion (USD 60 billion Treasuries + USD 35 billion MBS), which is quicker than the previous tightening cycle during 2017-2019 (USD 50 billion monthly cap), and the reduction is widely expected to begin soon after the May FOMC meeting.

Impact

Without hesitation, the market went on to price in a more aggressive series of rate hikes alongside the quantitative tightening roadmap revealed in the FOMC meeting minutes. This sent the US 10-year treasury yield to a three-year high of 2.83% on 12th April.

Opportunities/Risks

Rising rates environment is likely to benefit the financial sector MARKET OVERVIEW and since the sector constitutes a high weighting in ASEAN markets, it is not surprising that Principal ASEAN Dynamic Fund, an ASEAN fund, has significant exposure in the sector that investors can consider for this positioning.

Panic Selling In March Created A Great Buying Opportunity In The Chinese Equities

Event

The Chinese equity market faced multiple headwinds in early March 2022. Firstly, there was a renewed delisting concerns for some Chinese ADRs following US Securities and Exchange Commission’s announcement on 10th March 2022 that Yum China, ACM Research, BeiGene, HutchMed and Zai Lab would face delisting for failing to submit detailed audit documents. Secondly, fears over Covid lockdown especially in key cities like Shenzhen and Shanghai a ected sentiment and to put things into perspective, China’s new Covid cases rose from 355 on 1st March 2022 to 7,042 on 31 March 2022. Thirdly, China’s closer ties to Russia posed another element of uncertainty given that Russia is under various Western sanctions over Russia’s Ukraine invasion.

Impact

The various headwinds in early March 2022 crashed the CSI 300 Index and Hang Seng Index, down -14% and -19% respectively between 1st March – 15th March 2022. What happened next was the various government e orts to calm the market, such as 1) China Vice Premier Liu He said that the government should actively introduce policies that benefit markets, 2) Beijing pledged to ease regulatory crackdown on technology firms, 3) Beijing planning for audit concession to address Chinese ADRs delisting risk, and 4) China will not expand a trial on property taxes in 2022. The much-needed assurance from the Chinese government then prompted the subsequent rebound in Chinese equities with CSI 300 Index and Hang Seng Index up 6% and 19% respectively between 15th March – 31 March 2022.

Opportunities/Risks

Chinese equities still look very attractive from valuation angle or on a long-term fundamental perspective. Investors who find comfort in Chinese government taking more initiatives to calm the market recently can consider Principal Greater China Equity Fund – MYR Hedged for Chinese equity exposure.

Inverted Yield Curve – A Recession Indicator?

Event

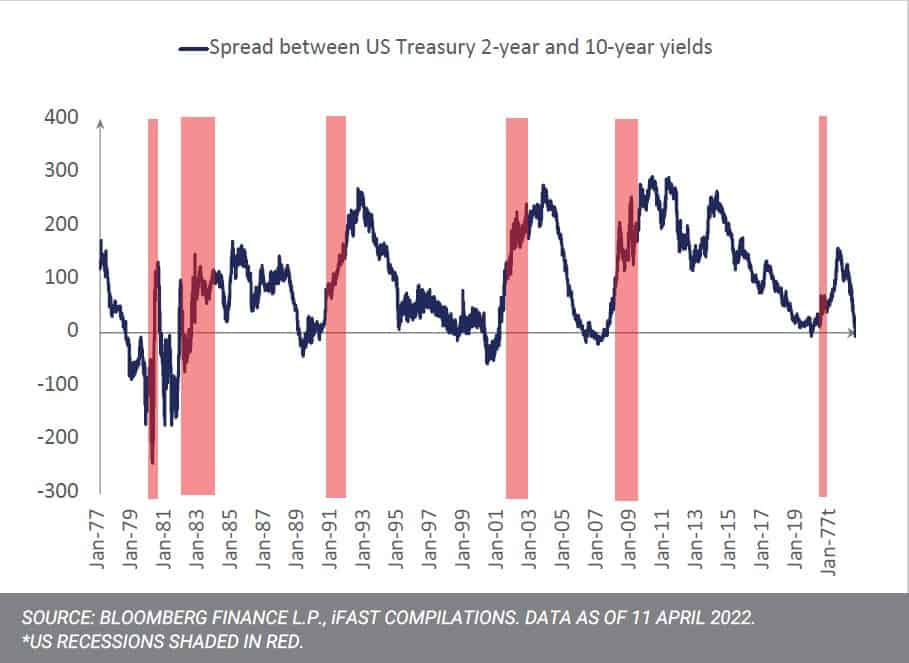

A yield curve is said to be inverted when short-term debt instruments trade at a higher yield than long-term debt instruments of the same credit risk profile. The most widely quoted combination is the 10-year and 2-year US Treasury yields, which yield curve has been flattening (i.e. narrowing spread) since early of March 2022 and the yield curve was subsequently inverted on 1st April 2022.

Impact

The yield curve inversion has sparked fears in the market because, if history is any guide, there is a correlation between inverted yield curves and a recession, albeit with a significant time lag. On average, since 1978, it took the US economy 19 months to get into a recession after the yield curve inverted. What is also worth noting is the market performance after a yield curve inversion, which has shown an average return of +7% in 6 months, +15% in 12 months and +23% in 18 months.

Opportunities/Risks

It is also widely known that the 10-2 Year Treasury Yield Spread is only serving as an indicator of a recession, not a cause-and-effect relationship. Also, given the significant time lag, we do not think that investors should be too defensive at this current juncture. However, investors who remained concerned but would like to stay invested may consider a well-diversified portfolio like iFAST Managed Portfolio to ride through any market volatility.

Malaysia Transitions To Endemic Phase From 1st April 2022

Event

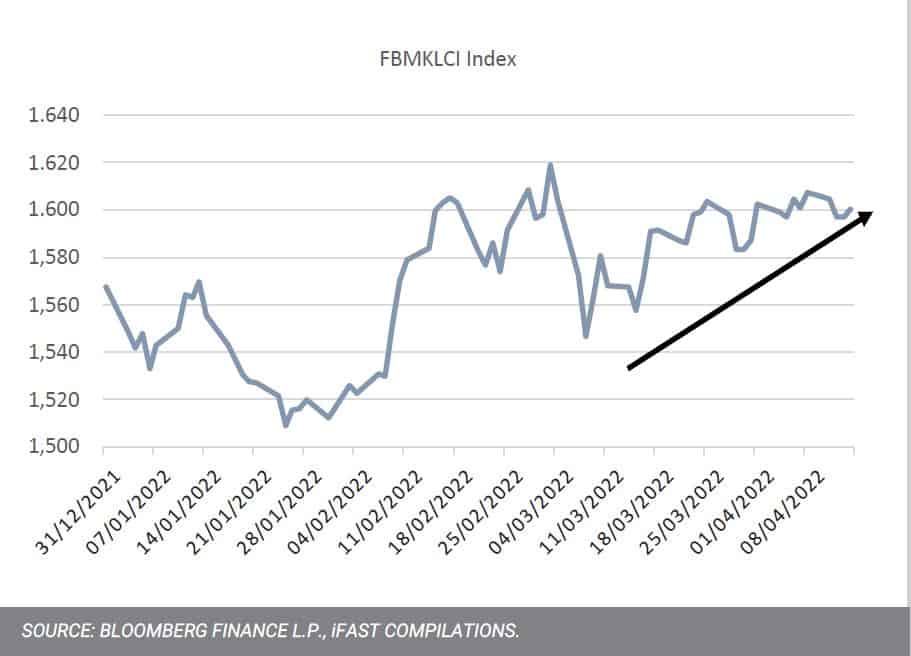

After 2 years of battling Covid-19 and a successful vaccination drive, Malaysian Prime Minister Datuk Seri Ismail Sabri announced on 8th March 2022 that the country will be transitioning to endemic phase from 1st April 2022. The country is more than ready for this with majority of Malaysians were already double vaccinated (79.7% as at 1st April) while the healthcare system has also improved significant with declining ICU bed capacity utilization for Covid-19 patients, at 20.2% as at 11th April 2022.

Impact

The announcement was taken positively by the market with the FBMKLCI Index rallied 3.6% from 8th March to 1,603.30 on 25th March and the index has since been hovering at 1,600. Further upside would likely be dependence on the economic strength thereafter. From the previous episode, when Malaysia came out of a strict lockdown back in 2H2021, the IHS Markit Malaysia Manufacturing PMI improved significantly from 39.9 in June 2021 to 52.2 in October 2021. Fast forward now, the endemic phase is expected to continue to boost the country’s ongoing economic recovery. For example, local businesses will benefit from 1) normal business operating hour as time limit for businesses will be removed and 2) more travellers due to

quarantine-free travel.

Opportunities/Risks

Investors who are feeling positive on the economic development in Malaysia and also the local tourism sector on easing of Covid restrictions can consider KAF Tactical Fund which has decent exposure to tourism related stocks such as Malaysia Airport Holdings and Genting.

Invest in unit trusts, PRS, EPF i-Invest funds & managed portfolios from as low as 0% sales charge with iFAST Capital by talking to your financial planner.

{kind=link}

{kind=link}

Leave A Comment