Budgeting is essential for managing monthly spending, preparing for life’s unanticipated occurrences, and being able to finance big-ticket items without falling into debt.

A budget is a forecast of revenue and expenses for a specific future period that is usually prepared and updated regularly. Just because you have to budget, doesn’t mean you can’t buy something you want. You don’t have to be a maths genius either.

It simply implies that you’ll have more control over your finances as you’ll know where your money goes. The need for budgeting one’s personal finance in Malaysia is important as the country is slowly coming out of a pandemic and people have been known to go out of control with their money when the economy starts healing.

Although budgeting is an excellent tool for managing your finances, many individuals believe it is not for them.

The following is a collection of budget myths—misguided logic that prevents people from keeping track of their finances and allocating funds wisely. In general, traditional budgeting begins with tracking expenses, debt elimination, and the creation of an emergency fund once the budget is balanced.

Contents

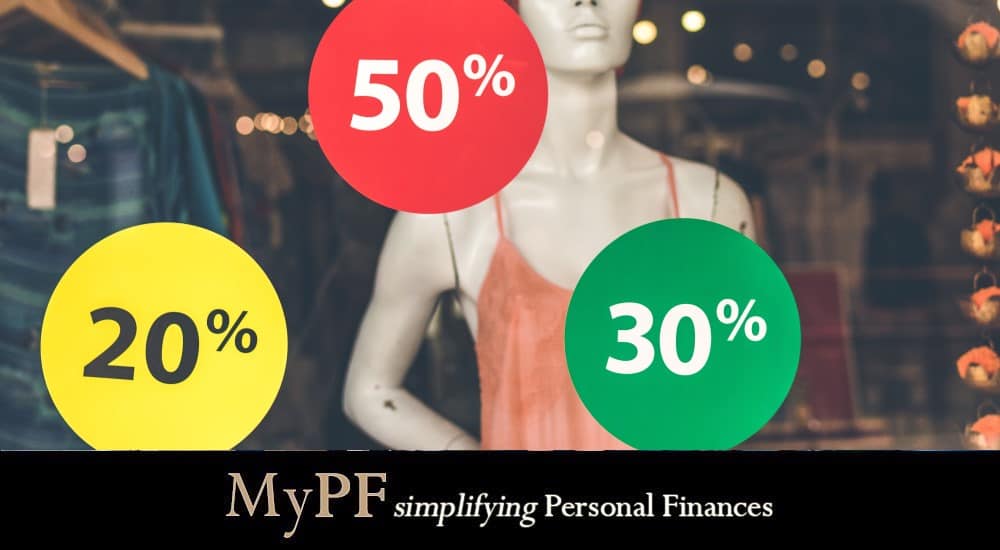

#1. 50/30/20 Budget

The 50/30/20 method is built on a hierarchy of requirements, wants, and savings. Determining which costs are necessities and which are extras can be tricky, but the following recommendations might help you divide your after-tax income:

a) 50% Needs / Non-negotiable Essentials

- Housing (mortgage/rent)

- Groceries

- Utility bills

- Minimum loan payments (credit cards, student loans)

b) 30% Wants/Personal Expenses

- Dining out

- Entertainment/events

- Travel

c) 20% Savings

- Emergency-fund savings

- Retirement savings

- Debt repayment (payments that exceed the minimum required amount)

The 50/30/20 rule strives to provide you with a well-rounded lifestyle with the correct financial balance, including basic bills, unforeseen expenses, and even enjoyable activities, all while saving for your future.

Pros of a 50/30/20 budget:

- Maintaining a balanced lifestyle that includes fun might help you stay on track.

- This strategy covers both current and future expenses, as well as an emergency fund.

- The pie chart format makes it easy to see where your money is going.

Cons of a 50/30/20 budget:

- It can be tough to distinguish some needs/wants because there isn’t always a clear definition.

- Focusing on minimal debt payments will lengthen your debt repayment period and raise the amount of interest you pay.

- Some people may believe that putting more than 20% of their income toward savings and debt reduction is a better use of their money.

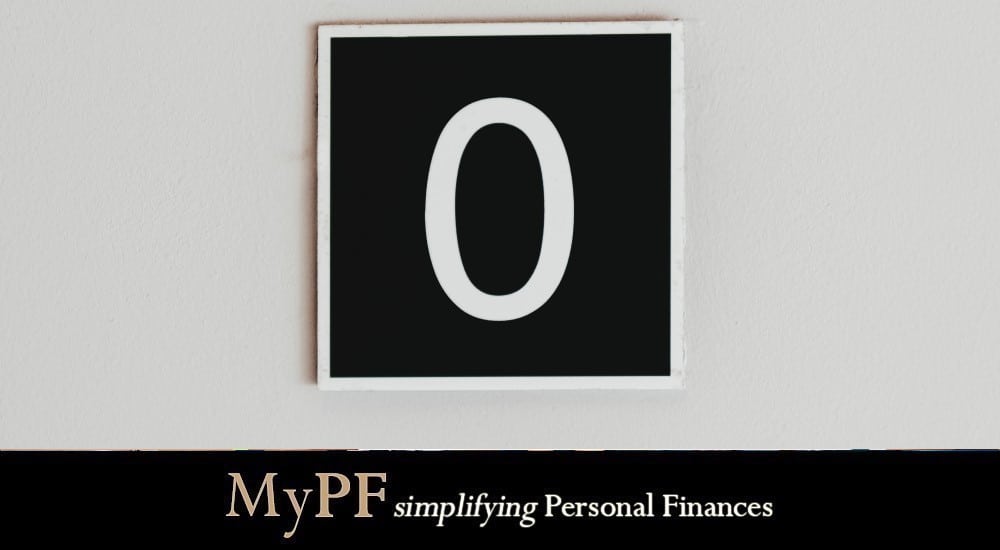

#2. Zero-Based Budget

Although the concept of zero dollars may be frightening, zero-based budgeting (ZBB) isn’t about depleting your bank accounts.

With ZBB, you deduct expenses from your monthly income until you have enough left over to pay whatever is most important that month, bringing you down to zero — in other words, you’re aiming toward a zero-waste situation with no money left over.

You can do this by categorizing your spending. Essentially, there are the major categories like food, housing, utilities, and transportation, and common categories that include additional bills, debt repayment, savings, entertainment, and miscellaneous costs. The money you have leftover is then allocated to the category that requires it the most, such as debt repayment or retirement savings.

Each month, you’ll start with a clean slate and have the opportunity to rethink your strategy, make any necessary adjustments, and consider the various monthly costs you’ll face.

Pros

- Gives you a more complete overview of your money’s whereabouts each month.

- You have more freedom in deciding how to spend any additional money from month to month.

Cons

- Tracking, categorizing, and balancing may take longer than alternative approaches.

- Learning how to get your balance to zero (without going into the red) could take a long time, possibly months.

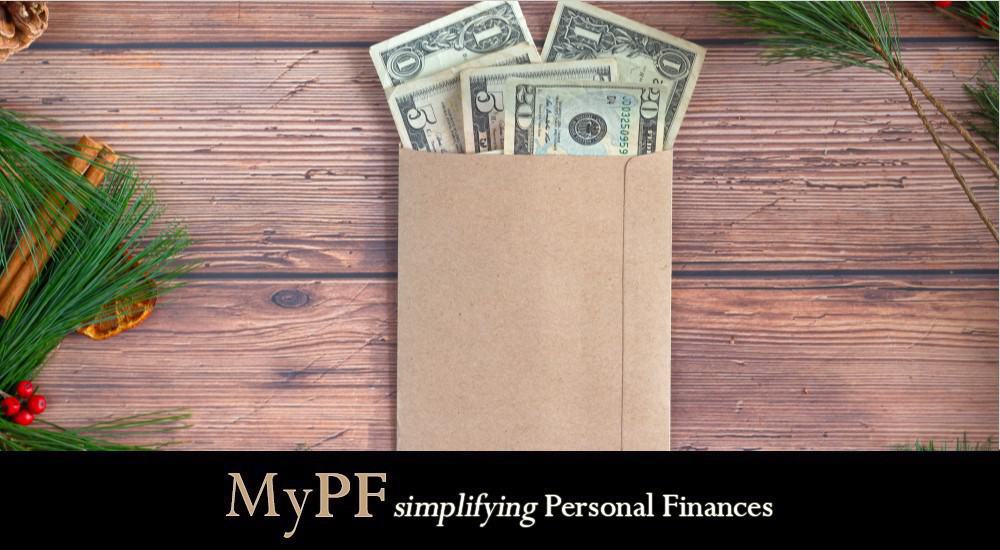

#3. Envelope Budget

This time-honored method involves dividing up actual cash and placing it in separate envelopes labeled for the majority of your monthly costs.

Using debit or credit cards provides an out-of-sight, out-of-mind effect, whereas having cash creates a tangible, hands-on experience every time you spend money. Because the money in each envelope has to last for the full month, you can’t replenish it once it’s gone, this increased awareness can help you stay on track toward your financial goals.

When you use this technique, you’ll pay for your fixed charges, which are those that don’t alter over time, as usual, whether by check, online or with automatic bill pay. Rent or mortgage payments, loan payments, utilities, and insurance are all examples of fixed costs.

The cash envelopes will be used for variable costs that may change throughout the month, such as:

- Groceries

- Utility bills that fluctuate

- Transportation

#4. Discretionary spending

Estimate how much each of these things costs you every month so you know how much money you’ll need to withdraw. Simply place the specified quantity in each labeled packet and dip it into them as needed. If you discover that any envelopes are empty before the end of the month, you may need to make modifications for the following month. This could imply reducing particular areas of spending, such as discretionary spending, or increasing utility bill spending limitations.

Pros

- Reduced overspending – you’re less likely to withdraw extra cash to refill your envelope than you are to swipe your card in a panic.

- You may be more proactive about spending if you have a limited amount of cash on hand.

- It feels good to have money left over at the end of the month.

Cons

- Estimating monthly spending can be difficult and may necessitate changes.

- Having more cash on hand than normal increases the chance of misplacing it.

- For some expenses, cash may not be accepted as a payment alternative.

#5. Values-Based Budget

Would you rather make a difference with your money than feel stressed about your finances? Beliefs-based budgeting entails making a conscious effort to spend any money left over on items or causes that align with your values, in addition to meeting your financial essentials such as food, housing, utility, and transportation costs.

Reviewing your bank statements from the last three months and thinking about your values is one approach to examining how you’re currently spending your money and how you’d like to.

For example, you may discover after reviewing your spending records that you spend the majority of your excess cash on dining out. While having time to go out and sample new places is important to you, you may also enjoy donating to charities and organizations in need, as well as taking care of your health and fitness. Here are some ideas for repurposing your spending:

- Save 40% of your extra cash to go to your favorite restaurants or new places that pop up.

- Donate 30% of your remaining funds to social projects, organizations, and local companies whose missions fit with your values (bonus points if you also offer your time to volunteer).

- Register for a self-improvement course or a well-being workshop with the remaining 30% of your money.

All of your budgeting can include core-values-focused expenditures. Looking to reduce your A/C bill while leaving a smaller carbon footprint? Instead of constantly operating your air conditioning during the warmer months, try opening your windows and employing fans. Want to save money on your water bill while also growing your food? Purchase a rain barrel. With deliberate budgeting, there are many options for lowering your carbon footprint.

Pros

- You’ll feel more connected to your life’s mission, which is beneficial to your overall health.

- Gives you greater clout — you can sometimes get more traction by spending rather than voting.

- Encourages reciprocity and strengthens ties within your community, no matter what shape it takes.

- Donating to charity could result in certain tax advantages.

Cons

- Not great for folks on fixed incomes who can’t afford it.

- Certain values-based alternatives, such as rain barrels and alternative fuel cars, may be difficult to obtain upfront.

- A lot of research is needed to verify organizations and find brands that agree with your values.

#6. Pay Yourself First Budget

The pay-yourself-first budgeting technique sounds like it would break all the rules just by its name, yet it doesn’t. This strategy, on the other hand, just prioritizes your savings. You begin by calculating your monthly net income, as you would with any budget. Instead of identifying monthly expenses or separating your income into categories or percentages, you’ll instead make a list of your monthly savings objectives, each with a monetary amount. After that, remove your entire savings from your monthly net income. Whatever money is left over might be used to pay bills and other costs.

Pros

- There’s less prep work and greater flexibility for monthly expenses that fluctuate.

- Your financial objectives will always be met.

Cons

- It might be difficult to keep track of expenditures if there is no organization.

- This guideline is unlikely to meet your financial demands if your monthly costs exceed your income or if you have high-interest debt.

Conclusion

Planning for a budget can be a simple and stress-free process if you allow it to be. Plan around your wants and needs, and remember to always factor in for emergencies. If you find it hard to continue on a plan, switch it up. Best of all, a financial planner can help you decide and plan on the best strategy for you and your loved ones.

Which budget plan do you think will suit your needs? Let us know in the comments down below.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment