A personal story of a young Malaysian exploring her credit score and what influences it.

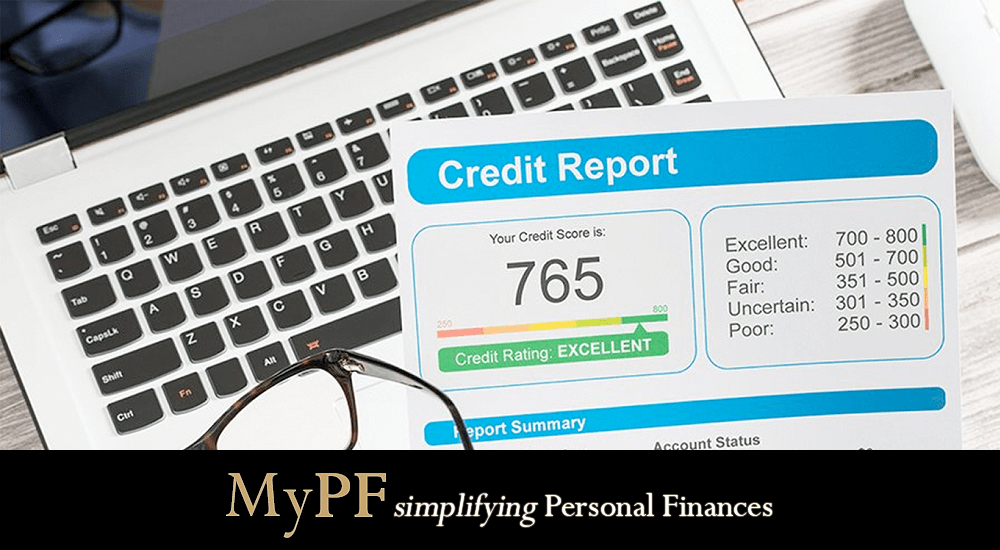

Most of us have probably heard the term “credit score” at some point in our lives. 2 years ago, the only thing I knew about it was that high credit scores are important if you want to buy a car or house. So, what is a credit score and what is it used for?

A credit score represents your creditworthiness.

In other words, your credit score represents how likely you would be able to pay back a loan on time. Lenders (banks) use this credit score to determine whether to grant you a loan or the interest rate associated with the loan.

Contents

My Personal Experience

In an effort to build my credit score, I signed up for a credit card. The goal was to maintain my spending habits and pay my credit card bills on time, sounds simple enough right? How wrong I was.

Last year after a few months of using my card, I decided to check my credit score out of curiosity. I bought my credit score report from CTOS and was surprised that my score was 728 — “very good”.

This year, I wanted to see if my credit score had improved so I checked it again. To my shock, my score dropped to 701 instead of improving.

I was confused at first. I didn’t accumulate any credit card debt, spent within my limit and always paid on time — how did my score deteriorate?

Eager to know where I went wrong, I did some research on credit scores. As it turns out, it goes beyond just making timely payments.

5 Factors Affecting Your Credit Score

There are 5 factors that affect your score, according to CTOS:

- Payment history (45%): The timeliness of payments of your payments and how late you were when you paid. It is best if you settle your loan payments/credit card bills every month. The later you pay off your debts, the more your credit score will be penalised.

- Amounts owed (20%): Your credit utilisation — how much of your credit limit has been used. This is what lowered my credit score. I’ve been using my credit card to top up e-wallets to collect points. Although I paid it off every month, I wasn’t aware that using a higher amount of my credit limit could affect my score. The general rule is to keep your utilisation below 30%.

- Credit mix (14%): A mix of fixed and revolving debt (credit cards) is preferred to prove that you can manage your debt effectively. You don’t need to have a diverse mix because this does not have a high effect on your credit score. Don’t take out a loan just to increase your credit mix!

- New credit (14%): The number of lines of credit you recently took out. According to the report, they look at applications from the last 12 months. The reasoning is that people generally apply for multiple lines of credit when they have cash flow issues. People that take on new debt are a higher credit risk to financial institutions.

- Credit history length (7%): The duration that you have been using credit — the longer, the better. This is why it is advisable that you do not cancel your oldest credit card because you will be wiping away some of your credit history. The impact will be minimal though, as this only accounts for 7% of your score.

My Lessons Learnt

Now here’s where I went wrong:

- I applied for 2 new credit cards within 12 months. Although this doesn’t affect a large portion, my score was definitely affected.

- My average credit utilisation was 32%. I wasn’t overspending but was using my cards to leverage on cashback opportunities. I figured that it wouldn’t cause any harm if I pay it back. I’ve since applied for a credit limit increase to help with that and have been repaying some of the e-wallet top-ups before the statement date.

I’ve since also learnt that getting a credit report yearly is key to monitoring your financial health.

- This is especially true for those of you that borrowed PTPTN. Many friends I know were not aware of when the repayments started.

- You will also be able to know how many lines of credit have been taken out in your name recently.

- If there are more lines of credit that you have applied for, you can detect fraud and identity theft early.

- And in my case, you will know if you have made money mistakes without realising it.

Go Get Your Credit Report

Getting my credit report has been an eye-opening experience and as mentioned before I urge all to get yours yearly as well. There are 4 sources where you can check your credit score using CCRIS, CTOS, RAMCI and Credit Bureau Malaysia. With your credit report and credit score, you can have a better idea of your financial situation and make necessary adjustments for a better future.

To learn more about your credit score, refer to the article links we’ve provided below specially curated for you!

MyPF Story is a series focusing on personal stories by licensed financial planners and Malaysians. If you have a story you would like to share, get in touch with us so we can document it.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment