Insightful perspectives on this month’s market events. The original version of this article was published on ifastcapital.com.my.

Contents

PROFIT RECESSION – US CORPORATE EARNINGS ARE LESS IMPRESSIVE THAN IT SOUNDS

Event

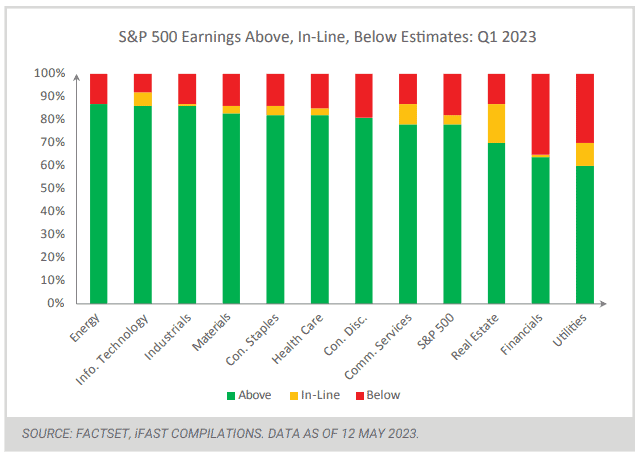

With the 1Q2023 US earnings season coming to a close, the profits of S&P 500 companies are estimated to have dropped -3.7% on average, compared to a year ago. More importantly, it was the second straight quarter of earnings declines for US companies. As per Factset, a majority of the companies, about 78%, have reported actual earnings per share (EPS) above the estimated mean EPS. This percentage is higher than the 10-year average of 73%. Furthermore, this is the highest percentage of S&P 500 companies reporting a positive EPS surprise since Q3 2021, with 82% of companies exceeding estimates.

Impact

In the first quarter, technology companies such as Apple, Meta Platforms, Alphabet, and Amazon outperformed expectations and were a positive aspect of the quarter. These companies are also benefiting from indications that the Federal Reserve has ceased raising interest rates. On the other hand, it is not surprising that the S&P 500 index has not shown any gains since the start of the earnings season in mid-April where sector earnings in the US are expected to decline more than 7% in the second quarter.

Opportunities/Risks

While the overall y/y decline in earnings for 1Q2023 is -2.5%, which is lower than the estimated decline of -6.7% that was predicted, the technology sector has been the bright spot among the sectors that have seen the largest increase in earnings. Artificial intelligence development could prove key, it could power the technology players to rally further over the long

term.

BOJ UEDA DIMMED HOPES OF A POLICY SHIFT WHICH SENT THE JAPANESE YEN LOWER

Event

In its latest policy meeting, the Bank of Japan (BOJ) maintained its ultra-low interest rates but unveiled a plan to examine its previous monetary policy actions where the new governor, Kazuo Ueda, said the bank is to gradually phase out the massive stimulus program. Despite reiterating its commitment to maintaining its accommodative policy, the central bank removed a promise from its guidance that interest rates would remain at “current or lower levels.” This decision provides the bank with more flexibility to make adjustments to its policies in the future.

Impact

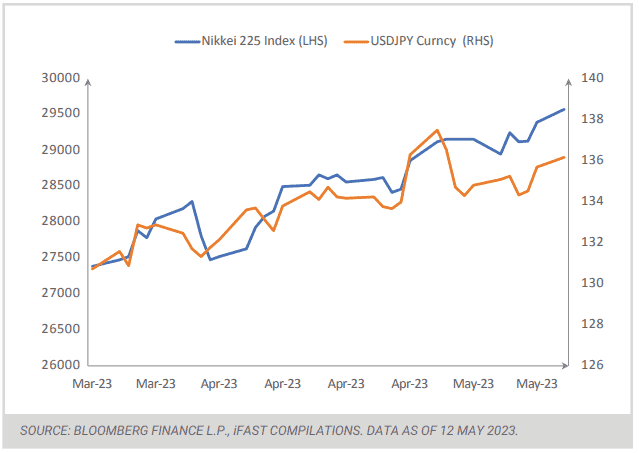

After the announcement, the Japanese Yen fell sharply against the US dollar (about 2.8%) while the Japanese equities, represented by Nikkei 225 index, gained 1.4% on the same day after the central bank’s press conference as the newly minted governor Ueda took a cautious approach and announced a thorough review of the Bank of Japan’s policies. However, he refrained from making any revisions to the bank’s longstanding measures for controlling the yield curve.

Opportunities/Risks

Given the fact that the BOJ left a reference to further easing as needed confirmed its stance to continue monetary easing, it remains uncertain as to when the BOJ may decide to terminate its ultra-easy monetary policies, as it considers the emerging signs of wage growth alongside the persistent challenges stemming from the slowdown in global growth. As BoJ is likely to remain accommodative, our positive stance towards Japanese equities remains unchanged.

CHINA’S FIRST POST-PANDEMIC LABOR DAY HOLIDAY

Event

China had its first normal holiday period after experiencing three years of Covid-19 movement restrictions. The five-day Labor Day holiday started from the weekend on 29th April 2023 until 3rd May 2023. From the Great Wall to Shanghai’s waterfront Bund, China’s most famous tourist destinations are being mobbed by throngs of domestic tourists who are travelling again in huge numbers over the holiday.

Impact

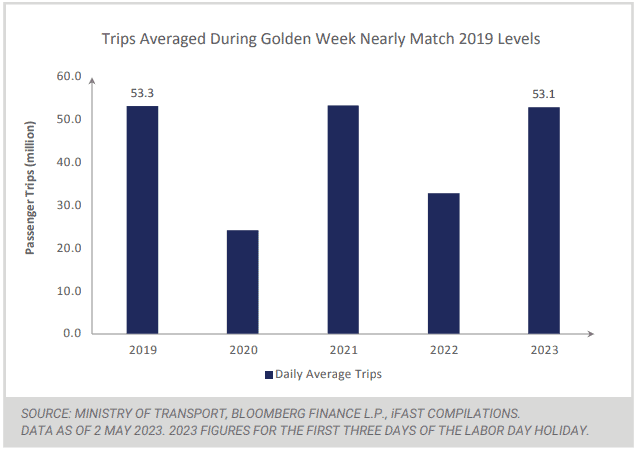

In the first three days of the five-day holiday, more than 159 million trips were made by car, rail, airplane, and waterways, which increased by 162% y/y while the average daily trips nearly matched with 2019 pre-pandemic levels. Domestic tourism revenue surged by 101% of 2019 levels to reach CNY 148 billion. There were around 274 million people travelled over the holiday, reaching 119% of 2019 levels. According to the travel agency Trip.com, compared with 2022 statistics, outbound travel bookings, flight ticket bookings, and hotel bookings increased by 700%, 900%, and 450% respectively.

Opportunities/Risks

Ever since China’s reopening in January 2023, there is a significant improvement in the services sector as reflected in the Caixin services PMI that reached 56.4 in April 2023. The sector continues to be supported by the strong recovery in consumer spending.

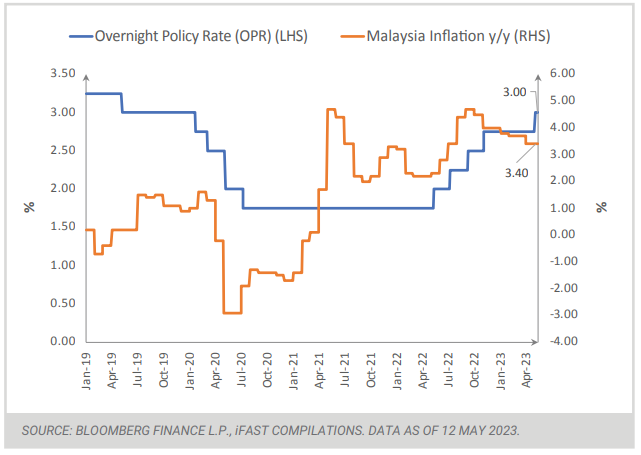

BANK NEGARA MALAYSIA (BNM) DELIVERED ITS FIRST RATE HIKE THIS YEAR

Event

The Monetary Policy Committee (MPC) of Bank Negara Malaysia (BNM) had the meeting on 3rd May 2023 and decided to increase the Overnight Policy Rate (OPR) by 25 basis points (bps) to 3.00%. The ceiling and floor rates of the OPR correspondingly increased to 3.25% and 2.75% respectively. The decision was only predicted by three out of 19 economists in a Bloomberg survey while the rest expected the central bank to hold the rates unchanged. This was also the first rate hike in 2023 after BNM paused for two consecutive meetings since November 2022.

Impact

The local bourse, FBM KLCI index, closed the day marginally higher by gaining 0.4% after the announcement at 3 pm, with the heavyweight banking sector leading the gains. Meanwhile, the bond market showed muted reaction, with the 3-year MGS yield up by 1 bps to 3.32% while 10-year MGS yield declined -4 bps to 3.70%. On the currency front, US Dollar (USD) has depreciated by -0.2% against the Malaysian Ringgit (MYR) from 4.4640 on 2nd May 2023 to 4.4552 on 3rd May 2023.

Opportunities/Risks

BNM is taking a more gradual approach in this monetary tightening cycle as compared to other developed nations such as the US which hiked their interest rate by a cumulative 500 bps vs 125 bps for Malaysia. The inflation pressures in Malaysia remain more moderate at 3.4% y/y in March 2023, which gave room for the central bank to remain its accommodative stance. We maintain our 3.5 Star “Attractive” rating for Malaysia.

Invest in unit trusts, PRS, EPF i-Invest funds & managed portfolios from as low as 0% sales charge with iFAST Capital by talking to your financial planner.

{kind=link}

{kind=link}

Leave A Comment