What you need to know about EPF’s latest changes including the Akaun Fleksible (Account 3).

![]()

The Employees Provident Fund (EPF) recently announced upcoming changes including a new Akaun Fleksibel (Flexible Account) commonly being referred to as Account 3. The announcement was met with mixed reactions from EPF members. Some viewed it with positive anticipation as way to access locked-in funds, while on the other side of the fence was worries of a grim future financial outlook with insufficient retirement funds.

The EPF is one of the world’s oldest provident funds established in 1951 with the purpose of providing retirement benefits to members, while continuing to be open to adapt to changes in employment landscape, demographics and members needs. Among several benefits, the EPF invests funds and distributes annual dividends to members. While withdrawals before retirement are allowed under certain circumstances i.e. housing, education, healthcare, insurance, and pilgrimage (from Account 2), the bulk of a person’s savings would remain not accessible until retirement (under what is currently known as Account 1).

Contents

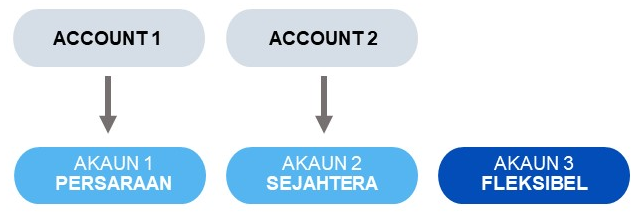

Account Restructuring

(Source: EPF)

In the most recent account restructuring affecting EPF’s 13.2m members below the age of 55, the EPF has announced that members’ existing Account 1 is renamed Akaun Persaraan (Retirement Account), Account 2 is renamed Akaun Sejahtera (Well-being Account), and the introduction of a third account called Akaun Fleksibel (Flexible Account) from which members can withdraw savings online or via the i-Akaun app from a minimum of RM50. After May 11, 2024, new EPF contributions are distributed among the accounts to the ratio of 75:15:10 respectively.

The introduction of Akaun Fleksibel has been welcomed by many as a good move since, as the name implies, it allows members the flexibility for withdrawals while potentially also increasing funds available for retirement. In particular, this would be beneficial to those facing desperate times such as during the Covid-19 pandemic when many of the rakyat faced financial difficulty to which the government responded by rolling out the adhoc EPF withdrawal schemes to help out, i.e. i-Sinar, i-Citra, and i-Lestari. That said, members should bear in mind to limit withdrawals to emergencies as their EPF savings in all accounts are first and foremost meant to be for their own retirement.

Distribution Ratio

Per the announcement, the 75:15:10 distribution ratio across the three accounts is replacing the 70:30 distribution ratio across the previous two accounts.

The 10% allocation for Akaun Fleksibel is a reasonable amount to allow for withdrawals. This allows members to not impede their own savings toward retirement while also allowing them to buy time while finding other sources of funding during difficult times. A 10% allocation each for withdrawals also promises a better controlled situation for the EPF to continue its investment and distribution activities, unlike during the aforementioned government-sanctioned adhoc EPF withdrawals during the Covid-19 pandemic which led to the EPF having to raise cash from 5% to 10% by disposing assets off.

The reduction from 30% to 15% for Akaun Sejahtera would impact future available funds for conditional withdrawals, such as for housing, education, hajj, and healthcare. That said, this should still suffice if combined with the new Akaun Fleksibel. However, if one is not prudent and has already emptied out the Akaun Fleksibel, one risks having insufficient funds to withdraw.

The increase from 70% to 75% in Akaun Persaraan will allow for retirement savings to grow to a larger amount. The median amount of EPF savings as of 2022 is at RM133,000. Compare this to the EPF-recommended minimum of RM240,000 at age 55 to allow for monthly RM1,000 withdrawals for 20 years. A 5% increase in contributions over 30 years working would increase the median to at least 140k (and likely more), reducing the gap and social issues related to retirees having insufficient funds during retirement.

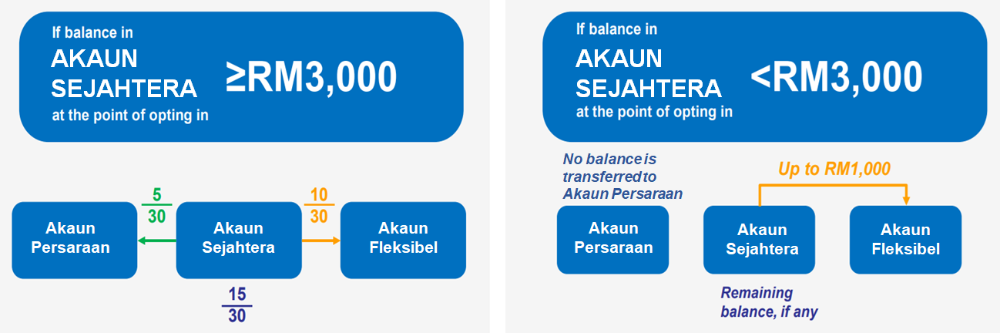

Opting In

(Source: EPF)

Above is the distribution ratio expected to change after 11 May, 2024. The EPF has made some allowances for the transition period. From 12 May, 2024 to 31 Aug, 2024, the EPF is allowing members the choice to opt-in to transfer funds from Akaun Sejahtera to the other accounts.

- If you have below RM1,000 in Akaun Sejahtera, then the full amount will be transferred to Akaun Fleksible.

- If you have between RM1,000 – RM3,000 in Akaun Sejahtera, then RM1,000 will go into Akaun Fleksibel while the balance remains in Akaun Sejahtera.

- If you have above RM3,000 in Akaun Sejahtera, then 1/3 of the sum will go into Akaun Persaraan, 1/6 of the sum will go into Account Fleksibel, and the remainder will remain in Akaun Sejahtera.

This opt-in is a double edged sword with both pros and cons. It does allow for EPF members who really need funds in the short term to access up to 10% of their EPF savings via Akaun Fleksibel immediately. However, moving funds into Akaun Fleksibel also allows for the temptation to make withdrawals. Do note that you only have one opportunity to opt-in which cannot be reversed.

Lower Dividends?

For the immediate launch, the EPF has assured that Akaun Fleksibel will provide the same returns as the other accounts.

The EPF has not ruled out a possible future where Akaun Fleksibel returns may be lower, which would be typical for investments held in liquid cash and cash equivalents. It could be expected that the EPF would need to monitor several factors before making any decisions such as how much funds remain in Akaun Fleksibel across a longer period of time, and how much liquidity is required in cash and cash equivalents.

To Withdraw or Not to Withdraw?

Withdrawing from your Akaun Fleksibel is simple from as low as RM50 either online or via EPF’s i-Akaun app. And, with cash sitting pretty in your Akaun Fleksibel, the temptation may be irresistible to some.

It is important to remember that the money in your Akaun Fleksibel is still very much part of your retirement fund. Withdrawing it for less than desperate reasons will only hurt your future self.

Discipline is the key word for managing your EPF Akaun Fleksibel. Only withdraw if you have an emergency, or a pressing shortage of funds to cover basic needs such as food and shelter.

If you have the discipline, having up to 10% of your EPF in Akaun Fleksibel while enjoying the same returns looks like a great way to have your cake and eat it.

Are you planning to opt-in for the EPF Account 2 redistribution? Let us know your thoughts in the comments.

You May Also Like

- EPF retirement savings guide

- EPF historical returns and performance

- EPF account restructuring (kwsp.gov.my)

- EPF account 3 – podcast (bfm.my)

{kind=link}

{kind=link}

{kind=link}

Leave A Comment