News reports say health insurance premiums are increasing by 40% to 70% in 2025 for Malaysians. What’s going on and why? This is Part 1 in our series about Rising Health Insurance Premiums.

As reported in late 2024, Malaysian insurance providers have requested the authorities (in this case, Bank Negara Malaysia) to raise health insurance premiums, with 40%-70% as the estimate being circulated in the news in Malaysia on how much healthcare insurance premiums might increase in 2025.

While BNM is stepping in to ease the burden on Malaysians, many are worried this is just the beginning. After all, things are becoming expensive. Since 2022, the prices of petrol and fuel increased sharply due to the Russia-Ukraine conflict. Inflation has hit Malaysians’ pockets hard.

It comes as no surprise then that this insurance premium increase has been sensationalised in the news and social media, with many bring to the table baseless speculations and misinformation. Hence, this series of articles will aim to provide a deeper but concise understanding on why the premiums are increasing by looking at the various players in the healthcare industry, namely,

- Part 1: Insurance Providers

- Part 2: Private healthcare companies (hospitals and clinics)

- Part 3: The buyer (you).

Hopefully, with these knowledge, you are able to make better decisions when it comes to healthcare and insurance moving forward.

Contents

A Brief History of Private Healthcare Insurance Providers in Malaysia

To understand how private healthcare insurance providers came to be and what their role in Malaysia is, historical context is needed.

Emerging from the 1980s, Malaysia’s public healthcare (government) system has essentially achieved its initial objectives. Basic healthcare was affordable and available to all Malaysians even in rural areas. Mother and infant mortality for both during and post pregnancy statistics went down. And non-communicable diseases like diabetes, heart attacks, strokes were sort of in control. (Source: Savedoff William and Smith Amy, 2011).

But problems emerged. Waiting lines were long. And because of expenses from the cost of healthcare, it put a big financial strain on the government. Hence, the government encouraged the development of the private healthcare industry as an alternative for Malaysians who can afford more expensive and quicker services. Alongside the emergence of private healthcare, the health insurance industry appeared.

The government implemented two main policy changes in the 1990s that proved a boon to private healthcare insurance providers that sent sales for health insurance soaring (Source: Bank Negara Malaysia)

- Introduced personal income tax relief for health insurance policies, and

- Allowed insurance providers to sell standalone health insurance products.

How The Business Model Works

All private businesses sell products or services that solves customers’ problems. Insurance providers sell you a health insurance product, where you pay monthly premiums in return for the provider to cover (fully or partly) your medical cost in the future should something bad happens.

The amount of coverage will depend on many factors. But generally, you pay a higher premium if you want

- Higher coverage amount for more diseases and ailments, or

- Considered ‘risky’ by the insurance companies if you have to use more private healthcare services

You see, an insurance company makes money by getting its customers to pay premiums to them, and they also reinvest those money to gain profits. The better their investments, the more profits they make.

And if policy holders make a claim, the insurance company will assess whether the healthcare treatment or service is covered under the policy. If they are, they will cover the cost using the pool of money that they have. This is beneficial to the policy holder as they only need to pay a monthly premium in exchange for the insurance company bearing the expensive cost of the healthcare in the future (should something happen).

But this depends on how many of them are making claims and how expensive medical services are. Insurance companies make more when there are less claims and cheaper medical services.

Rising Claims and Medical Costs

During the pandemic, medical claims declined as Malaysians couldn’t move around and were also wary about the dangers of travelling to hospitals and clinics. According to data from Bank Negara Malaysia, the number of claims for non-surgical and surgical services declined by 40% and 21% respectively during the pandemic compared to 2019.

However, when Malaysians were able to move around, medical claims rebounded with a vengeance. Medical benefits/claims payout rose by 34.5% to RM7.8 billion in 2022 and subsequently by 28.2% to RM10 billion in 2023.

Healthcare prices also increased as healthcare companies face increasing cost due to higher nurses salaries (higher minimum wages) and prices of equipment and medicine, while Malaysians also demanded for more and better quality products and services.

Furthermore, this could be made worse by ‘buffet syndrome‘ where policy holders maximise their insurance benefits by opting for more and better procedures while hospitals and clinics are more than happy to oblige.

Slowing Profit Growth

So, how is the healthcare insurance industry doing then?

There are various ways to look at this, but two things are clear.

- It is still making profits.

- But profits have slowed or declined in some years.

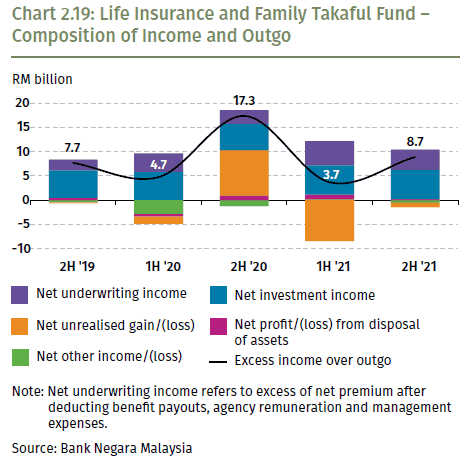

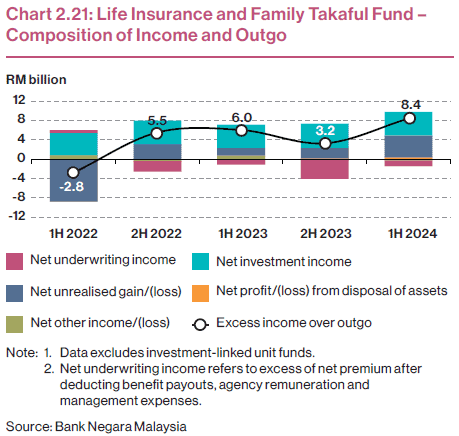

With data from Bank Negara Malaysia, the industry is best represented by life insurance and family takaful’s excess income over outgo. If income exceeds outgo (outflow), then the insurance company makes profit and vice versa.

While they still made profits in most years, insurance companies are finding it harder and harder to grow their profits.

The ‘net underwriting income’ represents how much profit is made from the total premium collected minus claims paid and other expenses. From 2019 to 2022, this number was still positive, meaning there were still enough premiums from buyers to cover claims.

However, that number significantly deteriorated from 2022 onwards when more Malaysians made medical claims after movement control restrictions were lifted. The amount of premiums now could not cover the total claims and expenses, where net underwriting income has consistently been negative.

However, that isn’t the only reason why profits have been weak.

Pay attention to the bars that are ‘net investment income’ and ‘net unrealised gain (loss)’. They signify the performance of their investments. Net investment income mainly comes from dividends and gains from stocks and bonds. This part of the business haven’t really grown that much in the recent years. Meanwhile, net unrealised gains (loss) are gains and losses on investments that the insurance companies are still holding on and have not sold yet. That has been uncertain as the global stock and bond markets were in turmoil from 2022 onwards as inflation got higher and increase everyone’s cost of living.

The insurance industry’s investment profits did not really grow during this period, and there are certain periods (like 1H 2021 and 1H 2022) where its investments performance significantly reduced its profits.

Hence, the slowing profits of the industry should not just be chalked up to higher medical costs, but also to the flat investment profits.

What Choices do Healthcare Insurance Players Have?

There are essentially two main ways for insurance players to prevent themselves from going into a loss.

- Be more aggressive in investing to generate more profits

- Increase insurance premiums

The first way is harder. One, because it involves taking on more risks that could incur bigger losses to the company. And it is easier said than done to make ‘right’ investment decisions as they can’t control what is happening in the markets.

The second way of increasing insurance premiums is more straightforward but potentially more controversial. Raising premiums will allow the insurance company to get more funds to invest and cover the claims and expenses. However, it is not popular as buyers would have to fork out more money and they will be under more pressure from the government.

Conclusion

While it might be tempting to jump to simple conclusions and point fingers at who the media is blaming as responsible for higher insurance premiums, the issue is complex. Hence, this series of covering each side involved in it is crucial for us to understand how things are from their perspectives. Hopefully, by understanding where each side is coming from, we can make more informed financial decisions when it comes to healthcare insurance.

In this article, we’ve explained how things work and how they look from the Insurance Providers. At the end of the day, they need to make a profit in order to continue running. And if we are to continue affording private healthcare, it is to our benefit to still be able to have health insurance.

In parts 2 and 3 we will look at what’s happening from the perspectives of healthcare companies and you, the buyer, and how it all adds up. So, stay tuned!

Let us know in the comments below what you think of the necessity of health insurance.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment