In our lives, we need financing for different reasons. Having a healthy credit score will smoothen the financing process. Your credit score plays an important part in the success or failure of your loan request.

You may have heard the term “credit score” thrown about often enough whenever there is talk about loans and lending. Here we go through 5 common questions about your credit score.

Contents

1. What is a Credit Score?

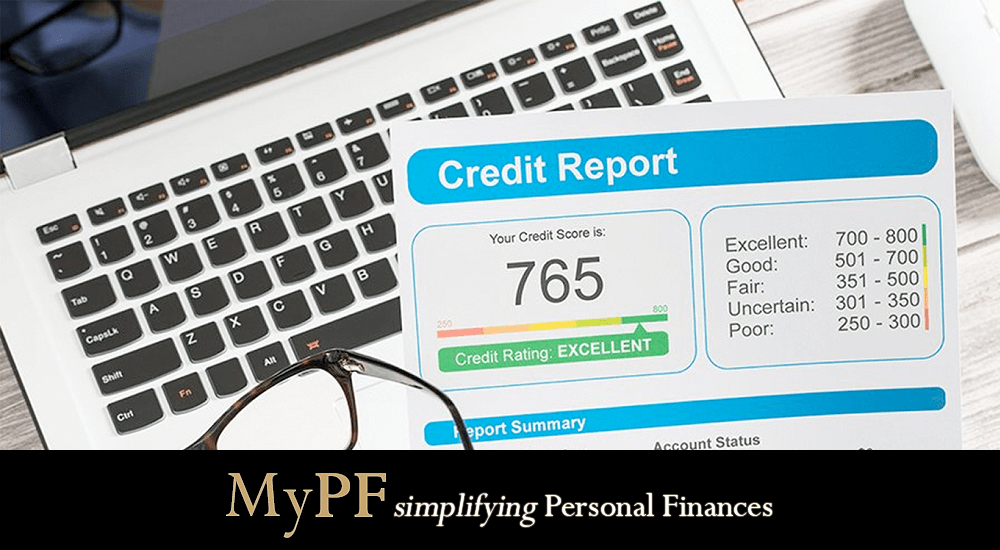

A credit score is a three digit numerical amount representing your creditworthiness.

Lenders use credit scores to assess the likelihood of a borrower (you) paying back their debts. Your credit score may be a primary reason for the approval or decline of a loan or affect the lender’s interest rate offered to you.

The higher the score, the higher the confidence the lenders place on the prospective borrower’s debt repayment capability. Every borrower should aim for a higher score.

Credit reporting agencies collect your financial and personal information (credit history) and document them on your credit report. This data is then used to calculate your credit score.

2. What is a credit reporting agency?

A credit reporting agency gathers and searches information on individuals’ and businesses’ credit. They are provided with reports from lenders and various other sources and then they compile a credit report that includes a credit score.

Lenders (such as banks and financial institutions) buy this information to make loan decisions.

Malaysia has four authorized credit reporting agencies:

- Central Credit Reference Information System (CCRIS)

- CCRIS does not provide a credit score. It only provides information on an individual’s profile.

- It’s a credit information database supervised by our Bank Negara Malaysia. CCRIS tracks the pattern of repayment of your loan.

- When you apply for a bank loan, the bank will check your CCRIS record to access your payment style. If your existing loan payments have been overdue 2 to 3 times in the last 12 months, including any deficiencies or whether a loan is under observation, the bank deems you as a low creditworthy person. Consequently, you may face difficulties getting another loan approved.

- CCRIS does not blacklist; only provides your credit records for bank ratings.

- CTOS Data Systems Sendirian Berhad (CTOS)

- CTOS is a top private-owned credit reporting agency with the most market share. Widely used by lenders.

- CTOS captured credit information from the public such as:

- Failure to settle debts

- Litigations (including bankruptcy status)

- CTOS does not blacklist; only provides your credit records for bank ratings.

- RAM Credit Information Sdn Bhd (RAMCI)

- RAMCI is a credit information office in Malaysia with the support of RAM Holdings Berhad.

- In 2015, in order to cater to individuals, RAMCI established a new division with the launch of three credit reports using i-Score, which is its own credit score system.

- Credit Bureau Malaysia Sdn Bhd (CBM)

- Started on 1 July 2008 to assist SME (Small and Medium Enterprises) to get better financing.

- With the introduction of the Credit Reporting Act 2010, CBM expanded to assist the individual consumer.

- CBM gathers and collates credit information from multiple sources. This information is then distributed to lenders.

3. How is the CTOS’ credit score is determined?

Each credit agency has its own method of determining a credit score. For this article, we used CTOS’ (the leading player) method which is based on the world-famed FICO standard:

CTOS’s credit scoring system considers five major components (with different levels of importance):

- Payment history (45%)

- Refers to whether an individual pays his debts on time. Also look at past litigation, bankruptcies, and delinquencies.

- The credit reports also show the payments forwarded for each credit facility, and whether the payments were received within 30, 60, 90, 120 days or more.

- The current debt level (20%)

- Refers to the amount of money a person owes and their credit utilization rate.

- A lot of debt does not mean low credit scores. Instead, the emphasis is on the money ratio owed to the amount of available credit.

- Types of credit used (14%)

- Types of loans you hold.

- Individuals need a strong mix of accounts to get high credit scores.

- Length of credit history (7%)

- Refers to how long you held a loan facility.

- The longer a person has credit, the better his score.

- New credit accounts (14%)

- Refers to new accounts opened.

- Opening several new accounts within a short time increases the borrower’s risk and hence reduces his score.

4. CTOS credit score ranges and what it meant to the lenders

The credit score of an individual range from 300 to 850. This is further separated into a few ranges.

| 744 – 850 | Excellent | Lenders regard you very favorably as a borrower. You are consistently responsible for managing your borrowings. And a strong candidate to qualify for the lowest interest rates. |

| 718 – 743 | Very Good | You’re considered a top customer generally financially responsible for managing money and credit. You pay most of your loans on time. Compared to their credit account limits, the balance of credit cards is relatively low. |

| 697 – 717 | Good | For new loans, you are above average and commercially viable. It’s possible to get competitive interest rates, but not the best rates of those in the two top categories. You can also find it harder to qualify for certain kinds of loans. |

| 651 – 696 | Fair | For new loans, you are below average and less viable. The credit history has some “bumps,” but there are no major defaults. You will probably still have credit extended by lenders, but not at competitive rates. |

| 529 – 650 | Low | Credit history is damaged due to several loans defaults from several different lenders for different loans. However, a bad score may also result from insolvency. You are not likely to receive new loans. |

| 300 – 528 | Poor | |

| No score | The chances to get a loan is almost zero |

So by now, you can see, the importance of having a high credit score. Lenders used it to decide the approval or rejection of a loan application.

The first thing you need to do is get your credit report from CTOS. Check the information. Inform the credit agency if corrections are needed. And most important, check the credit score. If your score is at the higher ranges (top 3), everything is fine and dandy (you still need to maintain it). If otherwise, plan ahead for some corrective actions to improve your score.

5. Where to get your credit report (whether free or paid)?

You can get your credit report from the four above-mentioned credit reporting agencies. Some are free and some require a fee.

- CCRIS report

- Free.

- Obtain from:

- CCRIS kiosks from the BNMLINK Kuala Lumpur and BNM Offices, and AKPK branches.

- eCCRIS, an online platform to access your credit report.

- Report includes information about:

- your current loans

- repayment records for the last 12 months

- any delinquency

- any lending under observation

- loans that have gone through scheduling and restructuring

- CTOS report

- Obtain from MyCTOS online portal.

- Two different types of CTOS report options:

- MyCTOS Basic report – an overview of your credit health with basic credit information (without credit score).

- Free, no cost

- Personal Information (NRD)

- Directorship & Business Interest (SSM)

- Litigation & Bankruptcy

- Trade Referee Listings (eTR)

- 2 Free MyCTOS Basic Reports a year

- MyCTOS Score report – full credit report with current CTOS Score and CCRIS details.

- RM25 per report

- Everything in MyCTOS Basic Report

- CTOS Score

- CCRIS Records (BNM)

- Dishonoured Cheque (BNM)

- Access to Rewards

- MyCTOS Basic report – an overview of your credit health with basic credit information (without credit score).

- RAMCI report

- Obtain from RAMCI MyCreditInfo portal.

- Three different types of RAMCI report options:

- Personal Credit Report Basic (PCRB)

- Costs RM10, with one complimentary PCRB on your birthday month.

- Personal infomation

- Business interests

- Legal and bankruptcy information

- Past inquiries

- Personal Credit Report Plus (PCRP)

- Costs RM15

- RAMCI i-Score (Credit Score)

- Banking Information (CCRIS)

- Skim Potongan Gaji Angkasa (SPGA),

- PTPTN

- Trade References (Non-Banking Info)

- Litigation History

- JagaMyID Subscription

- RM50.00 (1 year subscription + 2 free PCRP)

- RM90.00 (2 year subscription + 4 free PCRP)

- RM130.00 (3 year subscription + 6 free PCRP)

- 12 x monthly update of CCRIS Information and your i-Score

- 2 x Personal Credit Report PLUS (PCRP)

- Monitor your all your credit facilities utilisation

- tracking of credit applications made under your name

- Monthly payment tracking

- Email alerts on changes in your credit profile

- Personal Credit Report Basic (PCRB)

- CBM report

- Obtain from CBM portal.

- The report is called an Individual Credit Report (ICR)

- Overview of your personal information

- Related business information

- MySCoRE assessment

- Dishonoured cheques

- Past inquiries

- Credit information

- Non-bank credit information.

Conclusion

It is important for maintaining a good credit rating. It doesn’t just look good on paper it’s also essential for many opportunities in life. Those three digits in your credit report affect whether or not you can get a loan for a house or car. It can keep you from getting a job and whether you can be approved for a new credit card.

Do you think you have good credit score? Go and get your credit report now!

{kind=link}

{kind=link}

{kind=link}

Leave A Comment