What motorcycle does a financial planner ride? Wealth Vantage Advisory (WVA) is pleased to launch our “Have a Plan: How I Ride” series. Our financial planner for this edition is our Licensed Financial Planner, Muhammad Faris. This is the story of how he rides – both literally and financially.

Hi everyone, I’m Muhammad Faris and this is how I ride, financially and realistically.

Contents

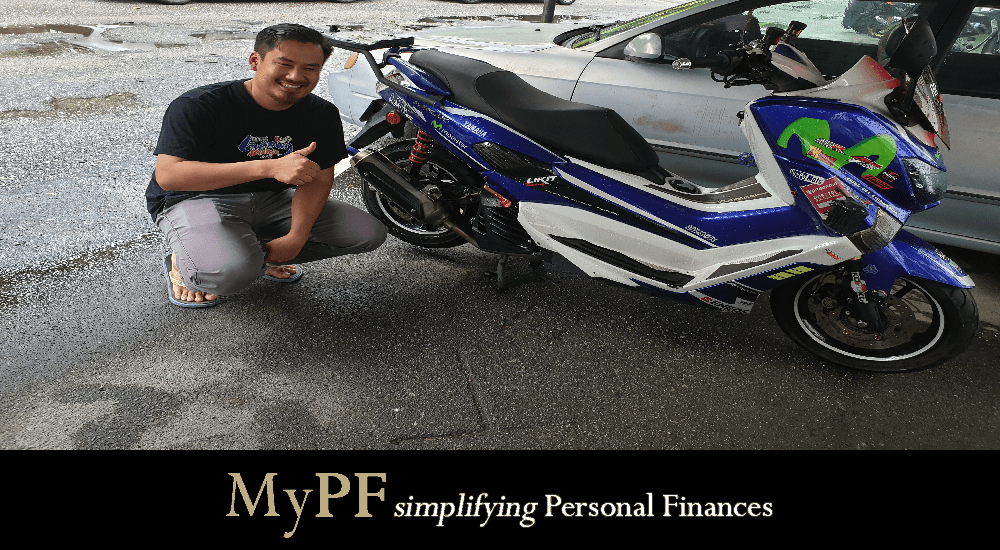

Q1. What Motorcycle Do You Ride?

I ride a secondhand Yamaha Nmax, paid for in cash. This is my first scooter and although it is pre-used, I find that it suits me very well as I’m still single and the maintenance is cheap.

I bought this motorcycle in 2018 when I decided to return to my father his Toyota Vios as I wanted to reduce spending on the maintenance cost of a car. Furthermore, having my own ride was to me a symbol of my independence as a young adult.

Q2: How Do You Plan Your Finances?

It is important to me that I arrange my spending priorities wisely. Things like paying for my house rental and putting the money in investments are high on my list. In this same list, transportation expenses is given a much lower priority.

I take one additional step every month to list down all the expenses and accessories that I have spent for my motorcycle. Knowing the exact amount I spend helps me better monitor my transportation expenses.

Luckily for me, Kuala Lumpur has plenty of transportation facilities that are convenient and comfortable. I consider public transport safe, and it’s a bonus that using it helps me save on toll and petrol costs. I even take the bus once in a month to return to my hometown.

Q3: How Do You Save and Invest?

As a rider, I am aware of the risks I am exposed to so I make sure I’m well protected with medical insurance with sufficient coverage.

This is how I save and invest:

- Every month, I will receive certain amount of income from my hard work. The more I work, the more income I earned.

- My rules in spending are to make sure to set aside an amount of money in my savings first. Only then will the balance be opened for my spending. The question is how do I know what amount of money I’m able to save?

- Human behavior is very flexible and adaptable to changes. For my first experiment, I paid attention on my eating habits in particular, where 49% of my expenses were from food and groceries, which I decided I needed to cut down on.

- At that time, I had reduced my daily expenses to about RM20 or less. It’s a good thing I prefer cooking at home over buying ready made food.

- By reviewing my spending patterns, I would try to squeeze the budget. Eventually, I managed to maximize my budget such that I could save 32% of my income. So, my personal winning formula was allocating close to 30% for emergency fund, 30% is for savings, 30% for investment, and any remainder would be opened for my daily expenses.

- This is where part of the motorcycle maintenance budget was came from, where the maintenance is pretty much only on replacing engine oil and brake pads. Thus, it needs only a small amount of money to keep it running well.

Q4: What is Your Financial Tip for All Malaysians?

“Buy what you need, not what you want. Avoid liabilities and always expect the unexpected.”

As a human being, we have three things that will be always remain in our life in order to maintain its continuity – needs, wants, and comfort. The sequence of the three in terms of priority are arranged according to our income and financial knowledge.

For me, I always highlight my needs over desire and comfort. Because when I managed to optimize my need, automatically I find that I have what I want and I get to enjoy the comfort produced.

For example, we need food to maintain our health and life continuity. But, what kind of food? Some people may say luxurious food, and some of them prefer nutritious food while some of them are preferring a lot of food. I prefer nutritious food rather than luxurious or huge amount of food. Because every penny that you spend should be worth spending. When I think of vegetables, fruits, and nuts, these nutritious foods are well within my affordable reach and provide a lot of vitamins to our body.

Likewise, the purpose of my vehicle is to deliver me from point A to B safe and sound. It is a need to fulfill. If I were to add on wants and comfort, the common considerations society expects would be a flashy brand-name vehicle and make it really large. But for me, fulfilling my needs is enough. Your answer may be different and that’s okay too.

Owning a motorcycle also jives with the later part of my financial tip as expecting the unexpected is less expensive with a motorcycle compared to a luxury car. For example, the cost of changing a motorcycle tire after a puncture is much less than the cost of changing a car tire, especially for larger cars.

For me, my lifestyle choices demonstrate what I mean by “Buy what you need, not what you want. Avoid liabilities and always expect for the unexpected”.

Follow Faris and Facebook and Twitter

Do you have any stories on how you ride? Share with us in the comments section below.

“How I Plan” is a series focusing on personal stories by licensed financial planners and Malaysians. If you have a story you would like to share, get in touch with us so we can document it.

{kind=link}

{kind=link}

{kind=link}

Leave A Comment