Learn what is crowdfunding, peer-to-peer (P2P) financing, how social lending works, selecting the best platform, and the benefits for you as an investor in Malaysia while reducing your risk exposure today!

What is Peer-to-peer Lending (P2P)?

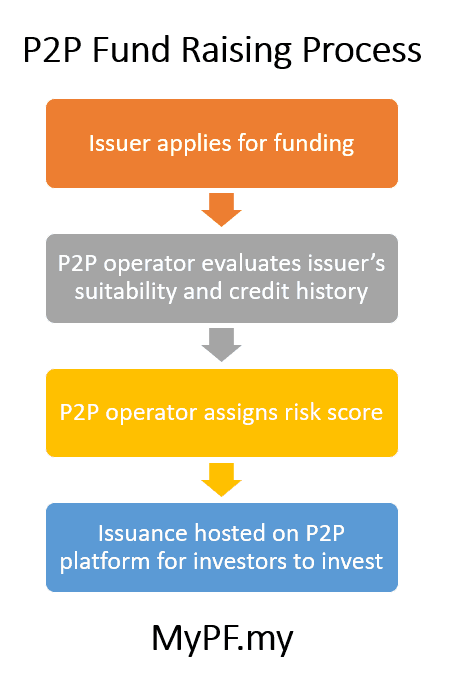

Peer-to-peer Lending (or also known as P2P financing, social lending or marketplace lending) disrupts traditional banking with FinTech. P2P lets small businesses and entrepreneurs obtain capital (borrowings) from a pool of investors via an online platform through an investment note. Malaysia’s Securities Commission (SC) announced the P2P Financing regulatory framework in May 2016 (ASEAN 1st) and there are currently a handful of approved P2P operators.

Investment note: the promissory notes sealed between “issuer” and “investor” to manage the risks involved in funding the “issuer”. It is a short term debt security. This legal document obligates the “issuer” to repay the funding that it has obtained via the investments of multiple “investors” based on specific terms and conditions of repayments.

With P2P Financing, you are a investor-lender and will be repaid your investment-loan with interest at fixed intervals. The P2P lending is to companies NOT individuals (so you cannot give or seek a personal loan). Only locally registered sole proprietorship, partnerships, LLPs, private limited and unlisted public companies are accepted.

Local SMEs industry is estimated to record a financing gap of more than RM80 billion” ~SC chairman

There are no limits to the amount that can be raised but are required to raise at least 80% of the targeted amount as a minimum threshold.

Why do business owners consider P2P Financing?

P2P financing allows a business owner to easily submit a request for funding and receive financing in a short period of time. The business owner often get better rates than banks, easier approval, and often do not need to place any collateral.

Equity Crowdfunding (ECF) vs Peer-to-peer Financing (P2P)

Equity Crowdfunding (ECF) introduced by SC in 2015 has similarities to P2P Financing in that both are options to raise capital.

The key difference is that with ECF, you invest in the company and are given shares becoming a partial owner of the company (instead of a lender). As a shareholder, you are entitled to a share of the profits of the company (if any) and sale of your shares if the company becomes a public listed company. ECF companies are typically Small Medium Enterprises (SMEs) thus often larger and slightly more established compared to a company seeking P2P Financing.

Pros and Cons of P2P Financing

Pros of P2P

- Low starting investment amount from as low as RM50.

- Short-term investment period with fixed monthly returns.

- Potentially higher returns than placed in a fixed deposit.

- Diversification to alternate asset allocations with uncorrelated movement to equity markets (investment diversification).

Cons of P2P

- You often will not know which company you are funding until after (also the company can opt to remain anonymous).

- Risk of the company defaulting on debt and unable to receive your investment returns.

- Risk of the company going bankrupt and losing your original investment.

- Income from P2P is taxed.

- No PIDM protection (compared to FD/savings accounts)

P2P Financing Considerations

P2P Financing is a high risk investment and you need to consider your risk vs potential gains. As an investor, you get to choose how much risk you are willing to take. Lower-grade loans are higher risk but offer higher potential returns. Higher-grade loans are lower risk but offer lower potential returns.

Investors are categorized into 3 classes:

- Business Investor: investing as a business entity with net assets value >RM10m

- Angel/Sophisticated Investor: net assets value >RM3m or income above RM180/250k in last 12 months

- Retail Investor: max investment amount capped at RM50k

Key Numbers:

- Returns/Interest Rates: capped at max 18% p.a.

- Expected returns = Interest rates on investment note less service fee

- First return 1 month after investment note disbursed

- Default rate: ~2% failure

- Investment period: 1 – 24 months

Fees:

- Initial verification fees: none

- Platform management service fees: 1-2% + GST

- Bank transaction/withdrawal processing fees: as charged by bank (i.e. RM0.11)

Account Activation Process:

- Register and fill subscription agreement and upload identification documents.

- Make initial funding deposit.

- Sign investor agreement.

- Application review for approval.

Should you consider being a social lender?

P2P or social lending is growing rapidly and does help address the shortfall of funding for SMEs and breaks downs financial borders. As an investor, social lending can be an way to access higher returns. However, you do need to take time to do your research and understand the risks involved.

Social Lending Tips

- Suggested overall asset allocation into high risk “other bets” (which includes your cryptocurrencies) should be no more than 5% of your overall portfolio.

- Research and compare between all the different P2P Financing Platforms available which have their own pros and cons.

- Consider investing into different companies in different sectors (and possibly even different platforms) to lower your risk.

- Read and understand the fact sheet provided including the risks.

Example fact sheet (click to enlarge)

Comparing P2P Platforms

P2P platform operators are incorporates under the Companies Act 1965 with a minimum paid-up capital of RM5 million and deemed to have fit and transparent IT infrastructure and risk scoring system. A dispute and complaint handling process must also be in place. When choosing a P2P platform, you will want to make sure it is regulated, the investment experience of the team managing the platform, and whether the platform invests in the loans themselves together with you as an investor.

On May 17, 2019 SC announced 3 new licenses for equity crowdfunding and 5 for P2P lending. (fintechnews.my).

| P2P Lender | Company | Market Share | Origins | Website | |

|---|---|---|---|---|---|

| Funding Societies | Modalku | 51% | Indonesia/Singapore | info@fundingsocieties.com.my | fundingsocieties.com.my |

| B2b Finpal | B2B Commerce | 25% | Malaysia | helpdesk@b2bfinpal.com | www.b2bfinpal.com |

| Fundaztic | Peoplender | 13% | Malaysia | support@fundaztic.com | www.fundaztic.com |

| QuicKash | ManagePay Systems | 8% | Malaysia | enquiry@quickash.com | www.quickash.com |

| AlixCo (FundedByMe) | FBMCrowdTech | 2% | Sweden | p2p@alixco.com | www.alixco.com |

| Nusa Kapital (NuKap) | Ethis Kapital | 1% | Singapore | hello@nusakapital.com | www.nusakapital.com |

| Capital Bay | Bay Group Holdings | New | Malaysia | contact@capitalbay.com.my | capitalbay.com.my |

| CapShere Services | CapSphere Services | New | Malaysia | contact@capsphere.com.my | www.capsphere.com.my |

| MicroLEAP | MicroLEAP | New | Malaysia | hello@microLEAPasia.com | www.microleapasia.com |

| Money Save Capital | Money Save Capital | New | Malaysia | hello@moneysave.com.my | moneysave.com.my/ |

| CoFundr | Crowd Sense | New | Malaysia | customerservice@cofundr.com.my | confundr.com.my |

More Info

- Funding Societies account opening RM30 bonus (fundingsocieties.com.my)

- List of Registered Market Operators (sc.com.my)

- UK crowdfunding company Rebus Group really ‘kena rebus’ (ft.com)

- Asian Institute of Finance: Crowdfunding Malaysia’s Sharing Economy (aif.org.my)

- Download P2P Social Lending Journal Template (MyPF Premier)

FAQ

Q: Is P2P lending Shariah-complaint?

A: It can be issued as an investment note or Islamic investment note. Islamic investment notes will be compliant. One of the platforms Nusa Kapital markets itself as a Shariah-compliant P2P crowdfunding platform.

Q: Do I need to pay taxes for P2P lending gains as an investor-lender?

A: Yes it is taxed at personal income tax rates for Malaysia residing citizens. For foreign investors, there is a 15% withholding tax automatically deducted.

Q: What happens if there i early or late repayment?

A: If the borrower makes an early repayment, the investor will receive an early repayment fee on the principal. If the borrower is late on repayment, the borrower will be charged late interest (daily rest) which is shared with the investor.

Q: What happens if a borrower defaults?

The platform operator will try to restructure the loan with the borrower to minimize losses to investors. Else a debt collection agency may be used.

Articles

- The Pros and Cons of Crowdfunding for Investors

- Investing in Stock Markets vs Ethical Investment in Ethis Crowdfunding

- Malaysia’s Equity Crowdfunding: The 4 Players

- Crowdfunding: A New Way to Grow Your Wealth

- Peer-to-Peer Lending vs Crowdfunding – What Are The Differences?

- Platform Patuh Shariah Untuk “Crowdfunding” Di Malaysia

- Islamic Crowdfunding Platforms in Malaysia

- 6 Sebab Kenapa Pelaburan Alternatif Semakin Popular

- 6 Reasons Why Alternative Investments are Increasingly Popular

- How to Setup Funding Societies Auto Investment Bot

- Should I Choose Business Financing or A Personal Loan?

- How does P2P Property Crowdfunding Work?

it seems like another JJPTR or MBI scam, right?