Latest Base Rates (BR), Base Lending Rates (BLR), Indicative Effective Lending Rates (Indicative) and upcoming Standardised Base Rates of Financial Institutions.

Updated: Jul 7, 2022

Malaysia’s Historical OPR Rates

| Date | Change in OPR (%) | New OPR Level (%) | New Ceiling (%) | New Floor (%) |

|---|---|---|---|---|

| 2022-07-06 | 0.25 | 2.25 | 2.50 | 2.00 |

| 2022-05-11 | 0.25 | 2.00 | 2.25 | 1.75 |

| 2020-07-07 | -0.25 | 1.75 | 2.00 | 1.50 |

| 2020-05-05 | -0.5 | 2.00 | 2.25 | 1.75 |

| 2020-03-03 | -0.25 | 2.50 | 2.75 | 2.25 |

| 2020-01-22 | -0.25 | 2.75 | 3.00 | 2.50 |

| 2019-05-07 | -0.25 | 3.00 | 3.25 | 2.75 |

| 2018-01-25 | 0.25 | 3.25 | 3.50 | 3.00 |

| 2016-07-13 | -0.25 | 3.00 | 3.25 | 2.75 |

| 2014-07-10 | 0.25 | 3.25 | 3.50 | 3.00 |

| 2011-05-05 | 0.25 | 3.00 | 3.25 | 2.75 |

| 2010-07-08 | 0.25 | 2.75 | 3.00 | 2.50 |

| 2010-05-13 | 0.25 | 2.50 | 2.75 | 2.25 |

| 2010-03-04 | 0.25 | 2.25 | 2.50 | 2.00 |

| 2009-02-24 | -0.50 | 2.00 | 2.25 | 1.75 |

| 2009-01-21 | -0.75 | 2.50 | 2.75 | 2.25 |

| 2008-11-24 | -0.25 | 3.25 | 3.50 | 3.00 |

| 2006-04-26 | 0.25 | 3.50 | 3.75 | 3.25 |

| 2006-02-22 | 0.25 | 3.25 | 3.50 | 3.00 |

| 2005-11-30 | 0.30 | 3.00 | 3.25 | 2.75 |

| 2004-05-26 | 0.00 | 2.70 | 2.95 | 2.45 |

Financial Institutions Rates

| Financial Institution | Base Rate (%) | Base Lending Rate (%) | Indicative Effective Lending Rate(%) |

|---|---|---|---|

| Affin Bank | 2.7 | 5.56 | 3.3 |

| Al Rajhi Bank | 2.85 | 5.75 | 4.2 |

| Alliance Bank | 2.57 | 5.42 | 3.11 |

| AmBank | 2.6 | 5.45 | 3.25 |

| Bangkok Bank | 3.22 | 5.87 | 4.42 |

| Bank Islam | 2.52 | 5.47 | 3.25 |

| Bank Kerjasama Rakyat | 2.6 | 5.58 | 3.4 |

| Bank Muamalat | 2.56 | 5.56 | 3.56 |

| Bank of China | 2.55 | 5.35 | 3.55 |

| BSN | 2.6 | 5.35 | 3.1 |

| CIMB | 2.75 | 5.6 | 3.5 |

| Citibank | 2.4 | 5.55 | 3.2 |

| Hong Leong Bank | 2.63 | 5.64 | 3.5 |

| HSBC | 2.39 | 5.49 | 3.5 |

| ICBC | 2.52 | 5.45 | 3.47 |

| Kuwait Finance House | 2.25 | 6.14 | 3.3 |

| Maybank | 1.75 | 5.4 | 3.25 |

| MBSB | 2.65 | 5.5 | 3.2 |

| OCBC | 2.58 | 5.51 | 3.45 |

| Public Bank | 2.27 | 5.47 | 3.45 |

| RHB | 2.5 | 5.45 | 3.5 |

| SCB | 2.27 | 5.45 | 3.5 |

| UOB | 2.61 | 5.57 | 3.36 |

Note: For reference only based on info from BNM. Subject to changes. Indicative rate based on 30-year housing loan/home financing product with financing amount of RM350k and has no lock-in period. E&OE.

Rates

Effective August 2022, the revised Reference Rate Framework with Standardised Base Rate will replace the Base Rate (BR) as the reference rate for new retail floating rate loans for increased transparency for consumers. The Standardised Base Rate will be

- Linked solely to the Overnight Policy Rate (OPR) and changing only when OPR changes

- Other components of loan pricing (e.g. borrower’s credit risk, liquidity risk premium, operating costs, profit margin) will be reflected in the spread.

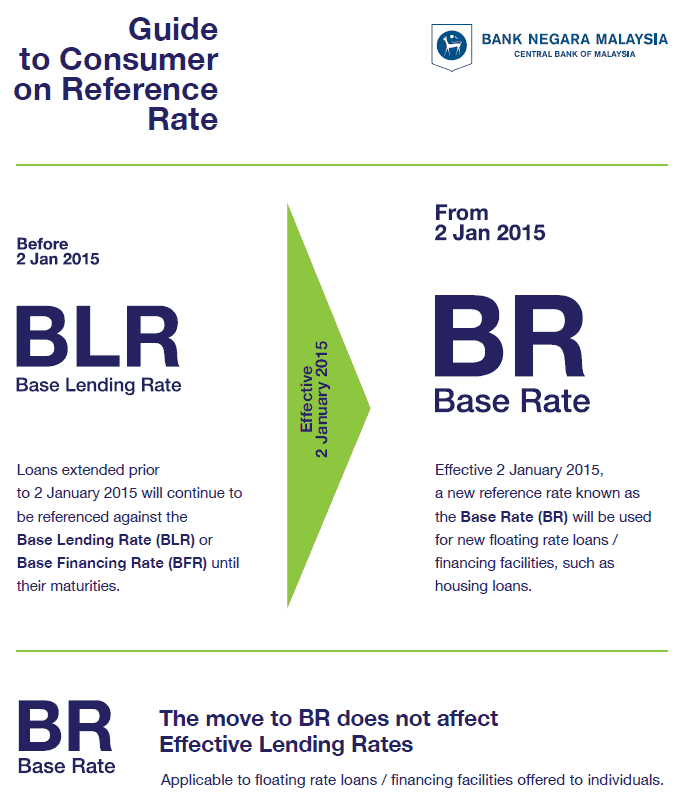

Effective January 2015, Base Rate (BR) replaces Base Lending Rate (BLR) as the main reference rate for new retail floating rate loans. Different financial institutions used different methods to set their respective BR.

(Source: bnm.gov.my)

Advantages

- More transparent reference rate to enable better decision by consumers in making loan choices.

- Better reflect changes in cost arising from monetary policy and market funding conditions.

- Encourages greater discipline and efficiency among financial institutions in pricing retail financing products.

- Spreads will always be positive for financial institutions.

- Stronger link between BR, commercial mortgage rates and Overnight Policy Rate (OPR) facilitating more complete adjustments.

What determines Base Rate

- Financial institutions’ (FI) benchmark cost of funds

- Statutory Reserve Requirement (SRR)

- Borrower credit risk

- Liquidity risk premium

- Operating costs

- Profit margin set by bank

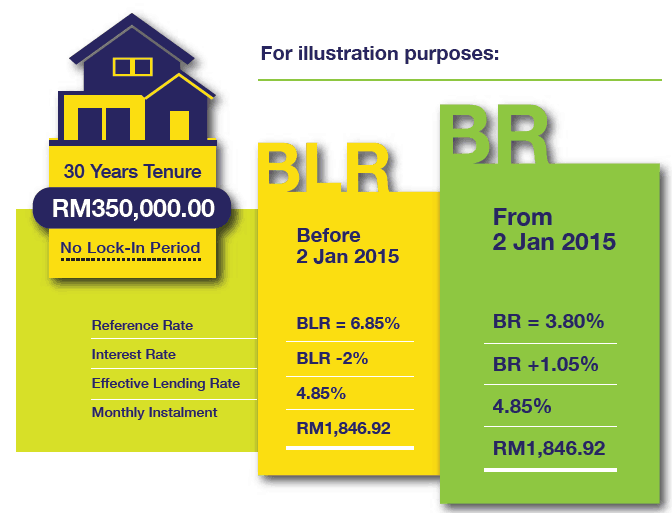

Indicative Effective Lending Rate

This rate refers to the indicative annual effective lending rate required by Bank Negara Malaysia (BNM) from FIs with the following criteria

- Standard 30-year housing loan/home financing product

- Financing amount of RM350k

- No lock-in period

Example of effective lending rate as below:

(Source: bnm.gov.my)

Which Financial Institution to Choose?

BR is applicable to floating rate loans and financing facilities for individuals.

Your monthly repayment amount will increase or decrease when there is a change in BR.

The move to BR does not affect existing effective lending rates loan indicated in terms of BLR.

Steps to take as a borrower

- Compare rates before taking out a new loan. Suggested to compare 3 to 5 different FIs.

- Ask for a Product Disclosure Sheets (PDS) including details of effective lending rate and total repayments for your loan amount.

- Ask the FI on what factors may lead to change on the BR.

- Confirm that your cash flow allows you to afford servicing the loan, especially if the rate goes up.

- Look at other factors that may have a impact especially financially. This may include lock-in period, branch availability, and fees charged.

FAQ

Q: What is the OPR ceiling and floor?

A: The OPR ceiling is the maximum interest rate permitted in a transaction, while the floor is the minimum interest rate permitted in a transaction. The rate from the OPR floor to OPR ceiling would be known as the rate corridor.

Q: Is there any changes to existing loans/financing pegged to BLR/BFR?

A: Np change as existing loans/financing will be based on prevailing BLR/BFR rate until settlement or upon review.

Q: How often are Malaysia’s rates updated?

A: Malaysia’s Monetary Policy Committee (MPC) meets 6 times a year in Jan, Mar, May, Jul and Sep and any changes to Overnight Policy Rates (OPR) which affects rates will be released at 6:00pm on the same day as the MPC meeting.

OCBC