What is Critical Illness (CI)? Isn’t it already covered with my medical insurance plan? What are my risks? Why do I need CI insurance? How much CI insurance do I need? Can I afford it (or afford not to have it)?

Updated: July 20, 2017

If you have friends (or frenemies) who are insurance agents, they have probably asked you before on whether do you have insurance. And we answer (whether truthfully or not-quite-truthfully) that yes we have ‘many’ insurance policies. Well, most of us do have some basics covered with medical insurance (medical costs are pretty damn high & ever inflating!), some death (or if you want to call it life), total and permanent disability (TPD) & maybe some critical illness coverage (if we purchased our policy in the last decade).

When asked what insurance do you think the average Malaysian needs but does not have, most of us actually answer Medical insurance. Maybe this perception comes from seeing the long queues & packed wards in government hospitals. However, the truth is that the risk area whereby more than 90% of Malaysians are lacking is in Critical Illness coverage!!

However, the truth is that the risk area whereby more than 90% of Malaysians are lacking is in Critical Illness coverage!!

What is Critical Illness (CI) insurance?

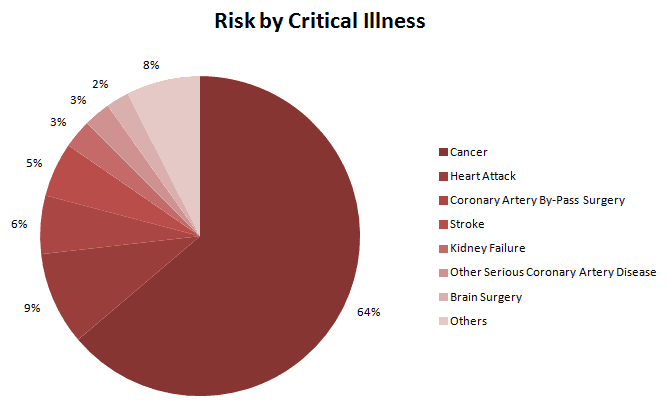

As a simplified explanation, you receive payment (in part or full depending on severity) when you are diagnosed with any of these 36 Critical Illnesses:

- Cancer (63.8%)

- Heart Attack (9.4%)

- Coronary Artery By-Pass Surgery (5.9%)

- Stroke (5.5%)

- Kidney Failure (2.9%)

- Other Serious Coronary Artery Disease (2.7%)

- Brain Surgery (2.3%)

- Fulminant Viral Hepatitis

- Major Organ / Bone Marrow Transplant

- Paralysis / Paraplegia

- Multiple Sclerosis

- Primary Pulmonary Arterial Hypertension

- Blindness

- Heart Valve Replacement

- Loss of Hearing / Deafness

- Surgery to Aorta

- Loss of Speech

- Alzheimer’s Disease / Irreversible Organic Degenerative Brain Disorders

- Major Burns

- Coma

- Severe Cardiomyopathy

- Motor Neuron Disease

- HIV Due to Blood Transfusion

- Parkinson’s Disease

- End Stage Liver Failure (Chronic Liver Disease)

- End Stage Lung Disease (Chronic Lung Disease)

- Major Head Trauma

- Chronic Aplastic Anemia

- Muscular Dystrophy

- Benign Brain Tumor

- Encephalitis

- Anglioplasty and Other Invasive Treatments for Major Coronary Artery Disease

- Bacterial Meningitis

- Loss of Independent Existence

- Systematic Lupus Erythematosus (SLE) With Lupus Nephritis

- Full Blown AIDS

Why do I need Critical Illness coverage?

A common objection is that one already has medical insurance (from my company plan and/or personally purchased)

History lesson: Knowledge on Critical Illness coverage is still somewhat lacking in Malaysia. Critical Illness (CI) insurance (or originally known as Dread Diseases) was 1st launched 1983 in Africa. In Malaysia, 36DD (no, not cup size but 36 Dread Diseases) started in the 90s. Back then, every insurance provider had their own definition of what was ‘Critical’. But as we entered the (then) new millennium in 2000, LIAM was formed at BNM‘s request & the list of 36 CI was largely standardized. This has been further streamlined in 2016 by LIAM.

One big misconception is that we have medical insurance so we do not need CI coverage. In actual fact, medical insurance coverage (which is definitely a must have!) is used to cover your hospitalization, doctor’s fees, surgery & medication costs. In other words, it all goes to the hospital & doctor.

However, CI insurance is payable to YOU. This means that you get much needed funds when you need it most during & recovering from CI (hopefully never though..).

When a CI hits a person, the now recovering individual will be out of work for quite a while. If you are employed, by Malaysian labor law you are given hospitalization leave of up to 60 days only (slightly more than 2 months). But a full recovery from a Critical Illness takes on average 3 to 5 years before you are up & running again! And it may take even longer to find employment again. At the same time most of your living expenses & bills are still running (food, home loan, car loan, utilities, child/parent support, etc)

Thus your money from CI is important as

- Income replacement for the full recovery time period (aka Lifestyle maintenance/Loan cancellation)

- Funds available to opt for alternate/additional treatment possibly outside Malaysia

How much CI coverage is required?

Too little? Too much? Too late?

It is recommended to cover 5 years of your annual income for CI coverage. At the very least, you should be covering 2.5 years of your annual income.

- Median Malaysian salary: RM5,000 (Source)

- Annual income: RM60,000

- Recommended: 5 years annual income equivalent: RM300,000

- Minimum: 2.5 years annual income equivalent: RM150,000

But how much CI coverage do we have as Malaysians?

- Above 90% of Malaysians have less then RM100,000 CI coverage

(And most actually below RM50,000)

The Cost of Critical Illness Coverage

I am enlightened & know that CI coverage is important & good for me. However I am concerned about costs, I have my expenses & I need to think of saving up for my future as well!

Congratulations to you that you are saving up for your retirement nest egg! You are already ahead of the pack if you are keeping expenses below 60% of your take home pay & saving at least 10% of your income (the more then better of course). Insurance costs should be at no more then 10% of your income (but probably more than 5% otherwise chances are you are under-insured which means you are actually at risk).

CI coverage is actually affordable especially if purchased relatively young (40s & below) when you have not been afflicted by any CI yet. Monthly costs estimate for RM150,000 CI coverage (by default comes with RM150,000 Life & Total and Permanent Disability coverage together):

- Age 20: 100 per mth

- Age 30: 100 per mth

- Age 40: 200 per mth

- Age 45: 200 per mth (for RM100,000 coverage only)

- Age 50: 300 per mth (for RM100,000 coverage only)

How long before I can make a CI claim?

The waiting period is normally 60 days from the date of the policy coverage for critical illness.

The severity of early/intermediate/advanced stage of critical illness also affects when you can claim depending on your insurance policy.

Leave A Comment