What is the progressive payment schedule for buying a new property under construction in Malaysia?

The Housing Development Act (HDA) 1966 was updated with Housing Development Amendment Act (HDAA) 2012 that came into effect on June 1, 2015.

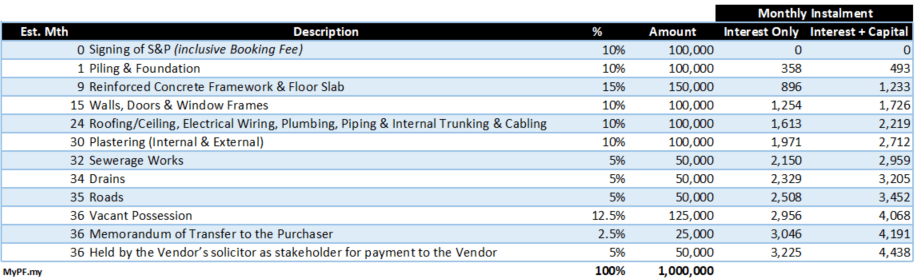

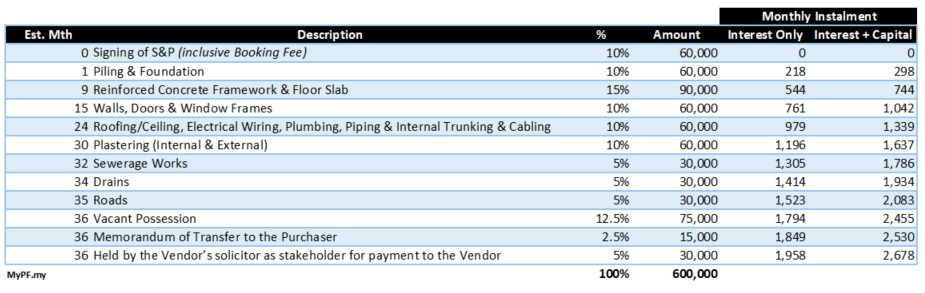

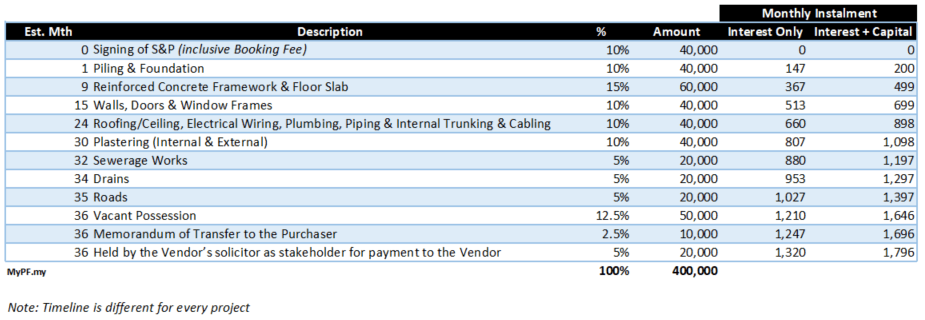

Details of the breakdown for progressive payment for Schedule G & H are as below:-

Schedule G is for landed residential while Schedule H is for strata residential.

There is no schedule for commercial properties thus less protection for buyers.

SCHEDULE OF PAYMENT OF PURCHASE PRICE

| Instalments Payable | % | Amount | |

| 1. | Immediately upon the signing of this Agreement | 10 | RM |

| 2. | Within twenty one (21) working days after receipt by the Purchaser of the Vendor’s written notice of the completion of:- | ||

| (a) the work below ground level including piling and foundation of the said Building comprising the said Parcel | 10 | RM | |

| (b) the reinforced concrete framework and floor slab of the said Parcel | 15 | RM | |

| (c) the walls of the said Parcel with door and window frames placed in position | 10 | RM | |

| (d) the roofing/ceiling,electrical wiring, plumbing (without fittings), gas piping (if any)and internal telephone trunking and cabling to the said Parcel | 10 | RM | |

| (e) the internal and external plastering of the said Parcel | 10 | RM | |

| (f) the sewerage works serving the said Building | 5 | RM | |

| (g) the drains serving the said Building | 5 | RM | |

| (h) the roads serving the said Building | 5 | RM | |

| 3. | On the date the Purchaser takes possession of the said Parcel with water and electricity supply ready for connection to the said Parcel | 12.5 | RM |

| 4. | Within twenty-one (21)working days after receipt by the Purchaser of the written confirmation of the Vendor ‘s submission to and acceptance by the Appropriate Authority of the application for subdivision of the said Building | 2.5 | RM |

| 5. | On the date the Purchaser takes vacant possession of the said Parcel as in item 3 and to be held by the Vendor ‘s solicitor as stakeholder for payment to the Vendor as follows – | 5 | RM |

| (a) two point five per centum (2.5%)at the expiry of six (6)months after the date the Purchaser takes vacant possession of the said Parcel | RM | ||

| (b) two point five per centum (2.5%)at the expiry of eighteen (18)months after the date the Purchaser takes vacant possession of the said Parcel | RM | ||

| TOTAL | 100 | RM |

Monthly Instalment Interest Calculation

RM400,000 at 90% loan rate at 4.40% for first 10% released in month with 30 days

400,000 x 10% x 4.40% x 30 / 365 = 144.65

Examples of Monthly Instalment

1m at 90% loan rate at 4.30%

600k at 90% loan rate at 4.35%

400k at 90% loan rate at 4.40%

LAD Late Delivery Payment to Housebuyers

Liquidated Ascertained Damages payable to housebuyers for lateness is delivering of vacant possession in 24 months (landed) or 36 months (strata) calculated 3 years from date in S&P.

LAD: 10% per annum on purchase price for period of delay

Notes:

- Complaint must be submitted within 12 months from CCC

- Developers for residential properties can apply to extend delivery by another 12 months.

- Caution: Do NOT sign any documents that waive your rights to LAD which have been practiced by certain unscrupulous developers.

If you face difficulties getting your keys, contact the Housing Tribunal (TPPS)

What Developers are No Longer Allowed to Promise Housebuyers

- Developer Interest Bearing Scheme (DIBS)

- Free legal fees

- Projected monetary returns/gains/rentals

- Claim panoramic views

- Travel time to nearby destinations

- Other information developer cannot genuinely lay proper claim

{kind=link}

{kind=link}

{kind=link}

Hi

Just wanna ask..if there is a rebate 13% or 15% . Means 9% when SPA, 2% on stage 2A and 1% on VP. Does it means that i only have to fork out just 1% right?

Hi, referring to your given example eof monthly repayment for “400k at 90% loan rate at 4.3% interest”, can you explain how the “monthly installment amount” being calculated?? Let say during the “Pilling & Foundation” stage, buyer needs to start paying 4.3% interest of the 10% loan (or RM40,000), which should be RM172/month right? May I know the calculation method you use to get RM197?

Hi,

Will the interest paid during the constuction period be deducted from overall interest amount imposed during loan tenure?

Hi, can you elaborate more on the interest part?

So assuming based on loan of RM1,000,000 , 30 years, interest rate 4.3%.

Based on normal amortisation table, the total interest is RM 781,537.

So because loan release based on percentage of completion, and therefore the interest charged during the early stage is lower, but how do the bank make up the remaining interest back to RM 781,537?

Hi,

If the developer failed to deliver the unit on the stated period (36months), what should the buyer do?

How is the 10% per annum on purchase price calculated, if let’s say the unit priced at 400k?

And do the buyer still need to serve the interest? What about the monthly installment?

LAD Late Delivery Payment to Housebuyers

Liquidated Ascertained Damages payable to housebuyers for lateness is delivering of vacant possession in 24 months (landed) or 36 months (strata) calculated 3 years from date in S&P.

LAD: 10% per annum on purchase price for period of delay

I plan to buy a small unit service apartment in Subang. The developer claims that government has extend VC to 48 months. Is this true? If this is false information, is it meaning the developer cheated on us? So we can proceed for LAD claim if they delay after 36months, right?

http://www.freemalaysiatoday.com/category/nation/2017/02/28/delays-are-developerss-responsibility-says-rehda/

hi,

interested how do you calculate the capital. I am got figure out how do you calculate the interest only, but how do you calculate the capital amount. What is the formula?

Thank you

Hi,

Please give me an explanation on the third schedule of payment of purchase price.What is actually foundation,structural framework,internal and external finishes.If I want to check on the above what should I be checking to make sure that they have finished the stages accordingly.

Thank you.

Will the principal amount reduce if I made extra payment while serving monthly payment? (Under construction)

Eg, my total loan was 400k. the first disbursement amount by bank to Developer was 50k. And the monthly payment was at RM250 (serving interest). If I pay 1000, will the extra 750 direct deducted from my principal ? IS the every disbursement amount by bank to developer consider the loan principal ? Will my principal reduced to 350k if I pay a lump sum 50k for the first disbursement ?

Can the buyer or should the buyer choose to start paying 100% of the interest plus capital installment after paying the 10% down payment, instead of paying just the interest based on the mentioned schedule until the key is collected? I assume loan tenure starts after key collection, hence interest paid before that period is extra expenses.

Hi,

In my home loan offer letter, it states that

“The Loan shall be repaid by monthly instalment as stated in the Letter of Offer or such other amount as maybe prescribed by the Bank and shall commence on the first day of the following calendar month after full release of the Loan.”

So, the official start of my monthly instalment repay (principle + interest) should be the next month after the very last 2.5% (two point five per centum (2.5%)at the expiry of eighteen (18)months after the date the Purchaser takes vacant possession of the said Parcel)?

Hi a developer offers me a DIBS when i bought a unut from them . Everything goes well and claimeable for almost three yrs but when it comes to the end of the construction, they said is not claimable anymore. S&P date is on 23 july 2014. Hand over is 36mth from S&P date. And they are late for deliver vacant. The LAD is claimable but the interest they refuse to pay back starting from July 18 to dec 18.

May i know if i have the right to complain for anything i can do? I had emailed alot of times to the GM but she seems like ignore me. Please advice. Thank

hi. if i nevr pay how. will any legal action will taken?

Hi. For home loan that is still under construction, how the amortization table would look like? Should it start with the first disbursement? or the beginning balance start with the total principal?

Hi, would like to clarify two things:

1) If i pay interest + capital during construction, then it is not an extra cost to me? i.e. essentially i start paying my loan amount earlier.

2) How to calculate interest + capital? Can’t seem to get the meaning from the table provided.

3) Refer to 1m at 90% loan rate at 4.30% table, the monthly payment is RM493 then RM1,233 or RM493 then RM1,726 (RM493 + RM1,223)?

Appreciate your clarifications

Hi Heng,

1) Yes technically you pay less as you start paying off the loan. Subject to the max loan disbursed so far.

2-3) Your repayment would typically be for interest only during construction. So your repayment would be RM358/mth until reinforced concrete framework & floor slab where it would increase to RM896/mth.

Hello, I’ve accidentally paid in excess for a progressive claim. Can developer refuse to return the excess sum of money?

Developer said excess payment can only be refunded once construction is completed. How?

Hi , my daughter is getting a unit 300k , deposit only 500 because she is first buyer and now they asking her to start paying interest once the loan is approved

Construction period is 3 year so is it normal to pay interest earlier

This progression payment basically is nonsense but there is nothing we can do..

Bank will release the loan money step by step

And we need to pay base on percentage of completion

Bank is releasing the loan money, but we cannot pay the loan, so we pay “for nothing”

Whatever we paid is extra, the longer its take for the house to complete, the longer we need to pay extra

After we get the key, then we start paying for loan

So it may reach 20-30k for 2 years period for 500k loan

Hi, i don’t really understand about interest. Lets say i’m paying progressive interest about $1.2k every month now. And currently construction is complete, and i will start to pay installment every month? Means installment+$1.2k ?

Hi, as for the progressive payment schedule, let’s say I bought a unit in level 25 and the entire block has 30 floors. How does the completion of reinforced concrete and floor slab completion is considered? Once they completed the work in my particular unit (level 25) or after the work completed for the entire block?

Hello there, i’m still confused after reading through. lets take rm 600k as example, the interest rate is what i have to pay for extra, then how about the “capital”? Is the amount paid for the capital contributed to my housing loan? meaning to say that during the reinforcement concrete stage i will need to pay RM744, RM544 as interest, so the RM 200 from here is treated as the house loan? If what i asked is true, then how does it work? Apply through bank? At which stage?

Another question is that, if i have financial constraint for only 6 months (due to commitment that will ends in 6 months), after 6 months i can afford to pay the monthly repayment then can i pay the progressive interest for 6 months only? E.g. i pay for RM744 during reinforcement concrete stage. until my other commitment is settled, i change to begin paying the house loan, lets say RM2.5k and no longer paying the progressive interest. Will that work? if yes, how to apply?

Thanks in advance! :)

Can we claim LAD based on nett Property Price? Or must based on Property Price as stipulated in Sale and Purchase Agreement.

Hi, May I know how long does it take for the completion of construction from ‘serving road to the said building to owner sign MOT’?

is there a duration?

Hi, the developer ask for stage 2(a) disbursement right after I signed the SPA, and before Power of Attorney and DOA. Is the developer’s prompt action valid. They are now charging me 1.5month late interest.

Hi. I’ve recently bought an undercon condo as of this date and priced at RM288,800 (SPA), 3.6%. My unit is at 25th floor. Currently the project is at 10%.

Questions:

1) The project started back in 2019, and i signed the SPA in 2020. Will i bear the cost of the cumulative interest at 10% stage? As in 12 months from the date of construction.

2) I calculated my interest instalment 10% stage to be roughly RM85. Is this correct?

What a relief! Appreciate your reply.

Also one more thing, what is the rough estimation of duration for each stage from 2 (a) to 2 (h)? Say the condo takes 36 months to be completed.

Hi, is it a must to pay the capital together with the interest? Or I can just pay for the interest first then only pay the capital while I get the VP?

Hi, do we start to serve the actual monthly loan repayment (interest + capital) right after the VP or after the last 5% stage?

Hi, hope you don’t mind clarifying some stuff for me. Let say the scenario as below

loan amount = 700K

interest rate of 3%

period for 35 years.

Total interest after 35 years approximately = 430k

1) progress is at 30%, interest is around RM500. If I continue paying/serving only the interest during the progressive period, I am actually not deducting from the 430k interest at all? Is that what it means?

2) progress is at 30%, I continue paying interest + capital. Hence capital is reduced, so the interest of the next stage will be based on the balance capital? Therefore, total interest at the end of the loan will be lower?

hi, i have simple question. as per the progressive interest, if the loan disburse up to 90%, the progressive int calculation wont be same as 90& of the actual instalment amount, correct ?