What you need to know about of bankruptcy processes in Malaysia. Being made a bankrupt is a major hassle and interruption to your life. Educate yourself about it and you will appreciate the importance being on top of your finances at all times.

Generally, the incident of bankruptcy happening to us never crosses our mind. If questioned what bankruptcy means, few things came to mind. A bankrupt is a loser in managing finances. A person who is homeless and someone who’s never ashamed to borrow money.

Being taken for a bankruptcy action can happen to anyone of us if you have debts. A sudden loss of employment or loss of the only source of income will put you in financial distress. As you’re unable to make debt repayment, you will face legal action. A financially literate person will make sure all his/her debts serviced and repaid. They know the inconveniences and hassles of being bankrupt.

This article spells out the bankruptcy processes in Malaysia.

Contents

1. Bankruptcy Defined

Bankruptcy Act 1967 and alongside the Bankruptcy (Amendment) Act 2020 make up the bankruptcy law in Malaysia. A bankrupt is the legal status of a person or organization who is unable to pay the debts owed to creditors. The court of law makes such declaration.

If you are unable to pay your debt, you are insolvent but not a bankrupt yet. It’s best you negotiate a deal with your creditors while insolvent. You may propose an instalment plan to settle the debt.

Only the court of law can declare you a bankrupt in a bankruptcy proceeding. A bankruptcy proceeding can only be taken if the amount owing is at least RM100,000 or if you have committed an act of bankruptcy. This amount was raised from the previous RM50,000 in the Bankruptcy (Amendment) Act 2017.

2. What if You are Declared Bankrupt?

Your spending power will be severely restricted. Your financial position is controlled, assets handed over and limitations of rights and holding of certain positions:

a) Your assets

You need to declare assets own by you. These assets will be under the strict supervision of the Director General of Insolvency (DGI). The DGI will sell them and the income distributed among the creditors. However, certain assets cannot be sold i.e.

- Any property you hold on trust.

- The instruments of your trade, garments, bedding, and other necessities you or your family need where the total value not exceeding RM5,000.

Part of your monthly earnings can be used to pay your debt.

For housing loan, if you default on payment, the bank (a secured creditor) can foreclose the house to be auction off without taking the bankruptcy proceeding.

b) Your rights

- Not allowed to travel overseas with passport surrendered unless with specific approval from DGI.

- Not allowed to hold a management position in any organization.

- Limited legal action (except for personal injury) subject to approval from DGI.

- Can only maintain one bank account.

- One credit card with a limit at RM1,000.

- Every six months submit income and expenditure accounting report.

Its obvious nobody would want to be declared a bankrupt. It will create negative tension for a couple. The additional stress and the stigma of being labelled a bankrupt may just be the final push that causes the collapse of your marital relationship.

Nevertheless, in certain circumstances such as failure in a heavily-invested venture, bankruptcy is the best way to a start afresh and move forward.

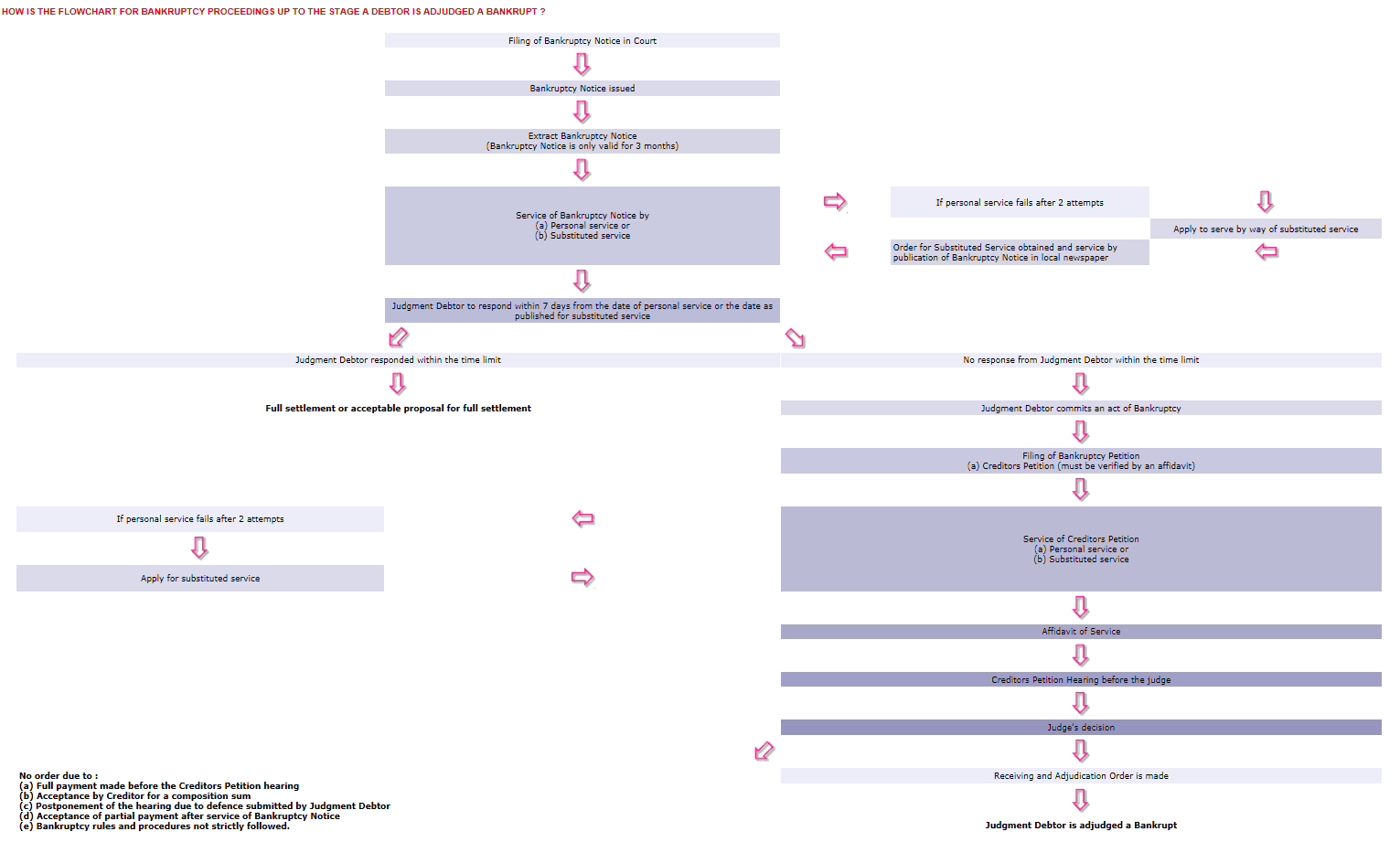

3. Bankruptcy Processes

(Click to enlarge. Flowchart Credit: lawyerment.com)

Bankruptcy action can be brought against you if you have carried out an act of bankruptcy, the common one is a failure to reply to a judgment debt or bankruptcy notice.

When you fail to pay your debt, the creditor will begin legal action and obtained a judgment sum. If you further fail to respond to the judgment obtained, the creditor will start bankruptcy action against you by issuing a bankruptcy notice. Failure to comply with the bankruptcy notice would be deemed to be an act of bankruptcy.

Once you are declared a bankrupt, you need to declare all your assets. Your assets will then be distributed among your creditors. Your creditors need to file proof of debts to the court for a claim of the assets.

A bankruptcy proceeding can also be brought against a minor (below 18 years old) with no maximum age limit.

4. Unknowingly Bankrupt?!

You may not realize you are bankrupt. How is this possible when there are various processes needed to be declared bankrupt?!

It can happen if you move a lot and did not inform your creditors. Bankruptcy notice must be served by hand personally and if you cannot be found by publication in the newspaper (substituted service) or send to last known address.

If you’ve been a guarantor for somebody or you want to discover about your bankruptcy standing, you can use a service like MyEG to verify which costs RM12 per identity per bankruptcy search. You can also request your credit score report from Malaysia’s Credit Bureau or CCRIS.

5. Becoming “Unbankrupt”

You either pay-off your debts or wait 3 years for an automatic discharge from bankruptcy. Once discharged, you will also be released from your unpaid balance debt. However, this excludes debts owed to the government or anything obtained through illegal activity.

There are two different ways of becoming “unbankrupt”

- Annulment: Your bankruptcy records are expunged after paying off your debts in full.

- Discharged: You are no longer bankrupt with negotiation with creditors on repayments. However, your records remain in CCRIS, CTOS, and other credit rating agencies.

You can immediately apply for passport and bank accounts again.

6. Avoiding Bankruptcy

The best way is to start and commit to a household financial budget living within your means and incorporating good personal finance principles including:-

- Expenses < Income

- Delayed gratification

- Invest, invest, invest

- Needs vs wants

- Seek the services of an advisor

Below are other tips to avoid going bankrupt:-

- Do not be a a guarantor in a loan agreement to anybody includes family member if you could not afford the monthly instalment in the event the borrower default.

- Do not take on big ticket item purchase with a bank loan if you could not afford it. Don’t fall to peer pressure or trying to keep up with the Joneses.

- If you currently hold a debt where repayment is doubtful, please seek a loan restructuring arrangement with the bank. Alternatively, you may seek help from The Credit Counselling and Debt Management Agency, or Agensi Kaunseling dan Pengurusan Kredit (AKPK) an agency set up by Bank Negara Malaysia in April 2006.

Malaysia Bankruptcy Law Updates

Malaysia’s bankruptcy laws receive an update in March 2017. Here are the key updates.

- Minimum to be declared bankrupt is raised to RM50,000 (from RM30,000).

- Social guarantors can no longer be declared bankrupt. Social guarantors provide guarantees to loans such as educational loans, hire-purchase loans and housing loans which they are not beneficiaries of.

- Automatic discharge of bankruptcy after three years, subject to good behavior including making payments towards your debt and submitting a full accounting of your monies and properties (previously 5 years and subject to Director General of Insolvency’s approval).

- A debtor may propose a voluntary arrangement to his creditors any time before he is adjudged bankrupt.

- A bankruptcy notice need to be served personally to a debtor.

FAQ

Q: Can a Malaysian overseas be declared bankrupt?

A: Yes. For example a Malaysian acting as a guarantor may be declared bankrupt upon judgment if trying to run away. The person may have issues when trying to renew his/her passport.

{kind=link}

{kind=link}

{kind=link}

Can a bank sue bankruptcy for a hire purchase debt from 2005 added all interest throughout 13 years became RM33,000 (current amount)?

Bank mentioned that even though the minimum amount to be sued bankruptcy is RM50,000, they are still able to sue for amount RM33,000 due to the debt initiated before the Insolvency Act 2017..

Kindly advise..

If I am having a hire purchase loan (car) in bank A, which still have an outstanding amount of 10k (which is also more or less the current market price), now bank B (another bank) has served me a bankruptcy note,

1.how would it affect the car which is still under hire purchase loan of bank A?

2. If I sold the car at market rate which is just sufficient to cover the outstanding amount to bank A, will bank B allow this transaction?

What if bankruptcy found own a car, rent apartment and even been charged by court to not paid rental?

My friend was declared bankrupts for being a social guarantor – hire purchase (Car). It has been more than 5 years now. Recently, about a year ago, he visited the insolvency office to check his status. He was told to open bank account, and start paying a small amount that he is capable of. Since then he has been paying about 100.00 every month.

Now I see there are two new rules which may apply for him:

1. Social Guarantor will not be declared bankruptcy.

2. After 3 years, one will be discharged from bankruptcy.

Can you please advice what he shall do ?

My friend been a bankrupt for 10 years….when we reviewed the records, we found that the creditor issued a receiving order on a property not owned by him, his dad’s property…when the creditor submitted the RO under oath, isn’t it an offence to lie in oath and make like an extortion to collect debts…isn’t it a perjury

Hi. I have a friend that being sued for bankruptcy. There is a company acting on behalf of the bank to collect the debts saying the court has issued a warrant to retrieve items inside the house (the property does not belongs to him nor the wife). The property ownership belongs to the wife brother.

Can the bank actually do so when the property is not belongs to him?

Seek for your professional advice.

Can you tell us in which Paragraph it states in Bankruptcy Act that bank shall not charged interest once the loan borrower adjudged bankrupt.

Dear sir .I already paid settle my depts long time ago many years the amount s around 15k only .now my name still in the system. Maybank have block my account for fer years .I already show them the settlement letter ….they don’t want to reopen my acc .What should.I do ?

Hi,

Both company director got bankruptcy due to director A borrow OD n director B as gurrantor, did director B can seeking partially discharge

From bankruptcy title with portion payment?

I’m looking an solution at this situation.

Regards,

Samuel tong

Hi, I’m currently 4 months unable to make payment to bank credit card and personal loan. The bank inform me would take legal action against me and commence me to bankruptcy. May I ask how long it will take to process me into bankruptcy? And during the time being can the bank issue a warrant from the court to retrieve items inside the house which belong to my wife?

That 3 years apply to all bankruptcy cases or the one starts in 2015 only?

My friend was declared a bankrupt 25 years ago due to credit card loan. Can she be automatically discharge now since she is over 60 years now. Also is she eligible to apply for an international passport. Thanks

Can a bankruptcy of 20 yrs sell off his property?

Once a person is declared bankrupt. Can the DGI/creditor have the power to withdraw the bankrupt EPF money?

Hi Greetings

If 1 of 4 of the company director declared bankruptcy. Does the company allowed to sell the property that belongs under company? Or will be disallowed? Can be the bankruptcy director written off from the company to smooth out the selling process?

Hi Mala, once bankrupt, the person is disqualified from being a director of a company or corporation (and cannot engage in the management of any business or trade run by your spouse, children or relatives). Thus the scenario would no longer be applicable.

Hi. Will be truly grateful if I can get an accurate legal answer for below.

Scenario:

1. A father, currently 76yo, bought a life insurance policy 33 years ago and named his wife and son as beneficiary.

2. 10 years ago the father got scammed and became bankrupt but has never checked his status officially at the Department of Insolvency or any other government departments.

3. 3 years ago, the father brought the son to the insurance company and assigned the policy to him (the son).

Question 1: Is the above life insurance considered an asset in the bankruptcy? i.e., the premiums and claim (upon the death of the father).

Question 2: Will action No.3 cause the son to bear his father’s debts?

Hi. We are not a legal firm so we can merely provide our opinion (and are not liable for any issues arising for information provided)

HI, hope you can help to reply few of my question, when late 2016 DGI had filed me as bankruptcy with MR 64K, when late 2017 and early 2018 bank had auction my properties and the balance i get back is about RM200K+ but all the amount goto DGI account, so i saw the Government had inforce one law like Automatic discharge from bankruptcy , in this case do i qualify for the automatic discharge from new law?? but until today i never meet up with insolvency department and do i still qualify for 3 years with Automatic discharge?? Please advise….

Regards

Wins….

Hope you can help answer this question.

I was declare bankrupt some 20 years ago without my knowledge when I was a citizen of Malaysia. However, I am no longer a Malaysian citizen as I have gain citizenship from another country. I do not carry Malaysian Passport anymore. Can I visit Malaysia without any issues. Thanks.

can a bankcrupt malaysian become an executor of a will

Previously this company was under 2 directors,A&B and recently share from both directors been transferred to C. Now, the company would like to declare bankrupt, may i know what will be happen to director A,B & C and all debts of the company?

First situation is if i hv housing loan not yet finish payment…

What will happen to my house if i being

declared as bankrupt?

Can the bank auction it if my husband can

continue its payment?

2nd situation if the house hv totally settle the loan (finish payment)

What will happen to my house? Can DGI

take my house & sell it off to settle my

other debts? The house is where my family

stay

Lastly, despite all the restriction & limitation, what are the benefit being a bankrupt?

Tqvm for answering!

I have join name for 2 property with my sister for 2 property.( Property A and property B)

Property A housing loan is under both of our name. – I am paying for the house installment

Property B housing loan is under my sister name – My sister is paying for the house installment

If my sister do not pay for the house installment for Property B and the property go lelong and she been declare bankruptcy.

What will happened to the property A since she is a joint owner? But I am still paying for the house installment. Will the property A be lelong also if my sister been declare bankruptcy and the property B which been lelong do not able to clear her debt?

Hi,

Actually joint property is also impacted. My sister has joined property with my mum and my mum is the one paying the monthly installment. My sister been declared bankruptcy, and all account was blocked including the housing loan account, thus my mum is not able to made any payment to that account. When checking wt bank, they said have to liaise wt Insolvency. The solution from Insolvency is to find a buyer for the house with the current house price in the market. That for me is such a ridiculous solution cause whatever that been paid for few years before is just burned. If failed to find a buyer, than the property will go to auction.

Hi.. i am about to make full settlement of my debt to Insolvency. My question, how long will it takes by Insolvency to clear my name and records? Thanks

Hi, can a bankruptcy fly to Sabah, using domestic flight?

Hi, my aunty at 2005 have a car loan with a bank, but she unable to pay the loan after that.

The bank was took back the car at that time and auction it, balance still have to pay 25k.

Yesterday my aunty received a letter from creditor (appointed by the bank) requested her to pay the balance 25k, if not they will take legal action.

Honestly my aunty already 50+ years old and unable to pay back (no income).

What will happen if she just ignore this case? What the legal action she will face?

Thank you for spending your valuable time to read the question.

hi, will bank force sales my property first then only sue me for bankruptcy or sue me for bankruptcy first? if i not able to pay the house loan.

Hi, im raj, mu mom brought a house, but she put my name and my brother name, it was 2004, after few yeara my momnunable to payback the loan, house auction for 90k, she loan for 190k, now on 2009, the outstanding qith intrest250k, me and my brother already declare backrupcy, the amount may now maybe 350k, im not sure, 2020 my mom passway, what i should do? Im joblesa now, any effect on my epf? Thank you

Hi this mr.matt i have personal loan, house loan (house loan joint name) and aeon loan due to my business down now im under program AKPK im paying my monthly instalment to akpk….in this time i was rentel land from land lard but due to my business lost i cant make to payment for 1 year plus but its about rm46,000

Im not pay the rental… now the land lord sue me in court to pay this amount but i have no income to settle this big amount if i can not pay the sum what will happen they make me bankruptcy?

Hi, does bankruptcy affects spouse/children’s bank account?

Hi, I have been trying a bankrupt for more than 10 years now and have been paying my monthly dues to MDI since then.

When I am retired and have no monthly salary coming into my account to pay my dues, can I get a discharge.

Would like to know if the bank able to declare me bankrupt if the amount is just MYR 3500.00 by CC.

As there is some other incident happen in between the negotiation of the installment period.

Thank for the advise in advance.

Hi, just wondering,

the automatic discharged is only applicable for case after 2017, is it for the case before 2017, there will be automatic discharge after 5 years?

there is a person with 100k debt from personal loan with bank:

1. can he do a self declare bankruptcy due to unable to repay?

2. Can he sell his current company to 3rd party before declare bankrupt?

”

Hi, can a bankruptcy still having a normal saving account if he is entitle for BSH from government?

Hi.. If a bankrupt not making any repayment to DGI after 9 years being filled as bankruptcy, what will happen and what he/she need to act now? Will the bankrupt be arrested when he/she surrender? Please advice.

Hi, my sister has been bankrupt for about 2 years for personal loan. She has a car which she was paying promptly. The moment she bankrupt, bank didnt allow her to pay the car instalment and told her to pay to Jabatan Insolvensi. From than nothing has been done and the car is kept dormant. My question is, can i buy the car ?

can i renew my passport in Malaysia even am already been declared bankrupt in Malaysia ?appreciate

and what will happen to me if I come back to Malaysia and pass-thru immigration will I be detained? thanks

I appreciate for the reply. and lastly, the automatic discharge can be done within 3 years or 5 years..

and will bankruptcy affect my application of certificate of good conduct?

HI Eric, does bankruptcy personnel under employed? Especially during MCO.

Hi… I was made bankrupt fr signing a personal guarantee for a shop lease agreement about 10 years ago. Can I apply for automatic discharge.

If a company declare bankruptcy, can the company run away from paying back the employee’s pcb and epf which were deducted monthly from salary but did not pay/credit into the employee’s lhdn and epf account?

http://www.mohr.gov.my

Hiii, i have a saving plan in life insurance company with inside cash value 300 k. If bankruptcy, any issues for that saving plan ? Is it belongs to me or belongs to DGI ?

Hi, could you please give some clear cases analysis to us, for the better understanding of Bankruptcy law in Malaysia? Appreciate a lot.

Hi I’ve got a propery and is a loan joint name. with my husband and the property s under my name.

what happens if my husband sue by bank and declare bankrupt? does the bank allow to take the properties from me under my name?

Hi.

My uncle had Bankruptcy in 2013. I check the her status in the system and it still says Bankrupt. Will the status change. It been more then 5 years?

If a person is declared a bankruptcy is she eligible to be include in a will? What are the consequences if her name is included in her mother’s will?

Even if she’s included in her mother’s will she still have to declare (She’s a Malaysian by the way)? What if she didn’t declare?

Hi, for bankruptcy, can DGI withhold my EPF money?

If i lost my job and unable to service my house loan and personal loans, will they freeze my bank account? For example if i get compensation from previous company due to downsizing, do they need me to declare the sum of money? and what is the process into bankruptcy status for my case?

I need help on my current credit problem and I have been chasing by an agent like mad and been threaten with court due and all. Who shall I talk and get help from to discuss the outcome and next step that I shall take?

I need help on my current credit problem and I have been chasing by an agent like mad and been threaten with court due and all. Who shall I talk and get help from to discuss the outcome and next step that I shall take?

https://mypf.my/2018/03/30/akpk-debt-management-programme/

Once Court has granted the Bankruptcy judgement, how does the current bank accounts (liquid assets) held by the person declared a bankruptcy get suspended/non operational? Do we need to serve the judgement to CRISIS and Bank Negara?

Assuming the person declared a bankruptcy was unaware, and comes to knowledge on the judgement, can she/he attempt to move any funds held under her accounts to say her husband or relative to “hide” from being subject for assessment by DGI towards the debt?

Hi. What happens to the remaining cash in the bank once being declared bankrupt. is it possible to withdraw or transfer the money to a 3rd party prior to being declared bankrupt

I would like to know if a person cant settle private hospital bills amounting MYR 300,000.00. Can they be declare bankruptcy ?

My cousin agreed and only afford to pay monthly MYR 500.00 but hospital demand more due to large outstanding amount.

My concern is will he be declared bankruptcy or insolvent. What will happen to him ? Is he able to work and gain his salary or will it be freeze ?

https://mypf.my/2018/03/30/akpk-debt-management-programme/

Can a foreign national declare bankruptcy in malaysia?

Hi.

I was a guarantor and was declared bankrupt in 2001 because the principal did not make payment. I was paying monthly to Insolvency until the case was discharged recently. How long will it take to get it removed from CCRIS/CTOS? And can I apply for loans again?

Can a bankrupt:

1) withdraw from his epf account 2 for the purpose of studies?

2) can he go abroad for his studies using this funds from epf?

Hi,

can person declared bankrupt receive prize reward in term of money for participating in certain competition?

My friend was a bankrupt.

Recently he divorced and court granted an order that the house registered under his name goes to his wife.

The wife intends to full settle the housing loan and redeem the house. However, she was advised that her ex-husband can’t effect transfer of property /discharge of charge of the house.

So she met insolvency officer for solutions. insolvency officer said the house is now belongs to her so she can get lawyer to transfer the ownership. But insolvency will not execute any documents relating to the discharge.

What can she do to register her name on the charge?

With the court order can the bank still proceed to auction off the house since the ex-husband cannot service the loan?

Can a person who declared bankruptcy buy standalone medical card?

hi, can I sue a person who declared bankrupt in 2003 ie 17 years ago?

Hi..am bankcrapcy 2016.Because I loss sg jobs..now am paying regular insolvency..planning to settle all debts..How many year take time to clear systems..can i apply house loan?

can bank declare a person bankruptcy without a amount owe ? but how ever the bank declare the person bankruptcy without amount owe for 14 years..can any pro & cons explain this situation..tq

Hi there, can a bankrupt person open an FD account ?

Hi,

Can I sell my car to my wife or my sister in law before I declare bankrupt so that my car won’t be taken away for sale to pay creditors? The current car value is RM75k and I want to sell at RM52k because my current car loan balance outstanding is RM52k. Currently I have defaulted in all my bank loan instalments for 2 months. Kindly advise. Thank you very much.

Eric Teo

can joint property effect if my husband declare bankruptcy

I borrow a loan join name with a company A and the company A unable to pay the Loan & ask me to manage it but i cant make the payment

will i become bankruptcy ?

what happen to my property that i have with my spouse ?

please advise .TQVM

Can a bankruptcy person buy standalone medical card for him/herself? And from where i can check the status?

Hi, if we did not renew the travel bond to insolvency because currently working abroad and can’t go back due to current pandemic, what is the effect? Will they terminate the Passport or working visa?

Does the automatic 3 year discharge means that as long pay the minimum and provide due reports of expenditure 6 monthly, any remaining amounts left over after 3 years will automatically be written off? Will the bankruptcy status and ccris ctos be written off as well? Thanks.

hi, my cousin is 80 years old and he was declared a bankrupt a few years ago due to a bank guarantee he signed. His wife (also 80 years old) is a Govt pensioner (retired school teacher). Being a bankrupt, can my cousin claim the wife’s pension when she dies? The wife has named him as the beneficiary.

Hi, what is going to happen if I am unable to pay my housing loan? Can I declare bankrupt?

can creditors lawyer issue through court an RO on a property not owned by me, just cos I am staying there means that is my property.

Hi, what happen to Malaysia if there’s too much people facing bankruptcy? Is the economy affected? or anything affected?

Hi, I plan to declare bankruptcy soon.

1) Currently I own a stall in wet market, can I still do business as a hawker? Will the government take back my stall?

2) If I pay minimum monthly payment required, how many years can I plea to discharge from bankruptcy and written off from the remaining balance?

Hi, may I know if a person is going to declare bankruptcy soon, how to settle the insurance part? Based on my understanding, the policy holder is not able to receive claims and any proceeds derive from the insurance policy. Thus, is absolute deed of assignment application is the only way to settle this issue for the policy holder to receive claims money and the proceeds? Appreciate your response.

Hi. I had been contacted by a Debt Collector Agency for a Rm50k debt. I had immediately paid RM20k. They had then acknowledged and balance now is Rm30k. I asked for an instalment payment schedule for the balance, but they refuse to allow. Instead they instructed me to pay Rm30k lump sum.

My Q- with the balance of Rm30k – can they proceed with a judgment Order for a bankruptcy charges against me, as they claimed now? What are my rights to negotiate for a payment schedule, especially during this global crisis and I am facing challenges with pay cuts, etc.

Thank you.

Can a bankrupt enter into a tenancy agreement?

Hi,

I just heard that the dewan rakyat has pass a bill stating that the bankruptcy has been changed from RM50k to RM100k. I was declared bankrupt a couple of years back for an amount of RM50k will it still declare bankrupt or will I be not be declare a bankrupt?

Hi Good day,

Mr.A been declared bankruptcy due to Hire Purchase deficiency balance in Bank X. Insolvency instructed to block all his saving and loan accounts. Mr. A not able to make House loan repayment in Bank Y. So the account became non servicing account and finally the property listed for auction on 21 sept 2020.

Is there any way to secure the property from being auctioned?

If a person (72 of age) is a guarantor and the principal did not make payment. If he file for bankruptcy? Will it affect his wife’s property/estate/account under her name?

My friend was declared bankrupt sometime in 2005. To date he has not approached the necessary parties to negotiate. Since its been more than10 years, will he be automatically discharge

Can I be sued for bankruptcy if I have total owings of more than RM50,000 from a combination of CCs and PLs but the highest single debt is only about RM30,000?

Hi, if my friend declare bankruptcy, he has a house but joint names with other people under SNP agreement only, but his name is not in the house loan agreement, what would happen to the house? Can DGI force to sell the house?

Hi there,

A debt collecting company wants to sue me for credit card debt that started around 15 years ago. Can they still sue me under the Limitation Act? If they sue me and they win the case, can they hold any of my properties which are joint properties? My properties are all under my name and my wife, since my wife is also the owner of my properties, can the company sell any of my properties given that they will the lawsuit? Thank you for your answer.

May i know how fast banks (creditors) will be informed by Mahkamah of one’s bankruptcy status and account freezing process?

Can Jabatan Insolvensi requests for repayment without having the property being sold to cover the debts? What if the amount is more than enough to cover the debts for sure but pending to be sold?

What is momentary of appearance? If i agreed bankrupt the very first minute a lawyer contacting me, do i need to submit momentary of appearance? Why do i need to file it if i dont have intention to dismiss the so called charge against me? By the way, i did clarify to the lawyer i agreed to bankrupt, why do i still need to have agreement from government lawyers to get the filing of momentary of appearance done? I was charged for the belated filing of momentary of appearance which i thought i only bound to submit if i refuse to proceed for bankruptcy….

Hi, my brother passed away last year and only we found a registration card on bankruptcy in his room. What can we do?

Hi there,

what happen when someone gave-up Malaysian citizenship before being declared a bankrupt by banks? Thanks for answering.

Hi sir ,

My mom had a hire purchase loan taken under her

Name 25 years ago and only today she got a call from debt collectors to pay up the loan amount.she has no assets or not even employeed.what would be the action taken against her?

Please do advise on this situation.

Hi there,

I received a letter from Jabatan Insolvensi asking me to meet them with my asset list. Before this, I didn’t receive any notice from bank or lawyer.

Am I a bankrupt now?

I’m still waiting for the payment options from bank.

My house address and phone number still the same. I thought bank must notify me before they proceed with the bankruptcy process.

Pls advise. Tqvm for your time.

Hi there,

Can a bank sue me for a credit card debt about 16 years ago? My credit card limit according to the bank then was RM8,000.00. But today the amount has escalated to RM875,000.00. All these years there have been no contact with them and I have never receive any form of letters from them. I only come to realized this when I did a CCRIS check. Now they are sueing me bankrupt. I want to know what can I do or what is my next course of action. I tried calling them to negotiate for a more realistic figure but the did not reply.

Hi,my case is ANNULMENT OF ADJUDICATION ORDER on date 15 april 2020,my question is issit my records remain in CCRIS, CTOS, and other credit rating agencies?or automatic clear out??

Hi, i was becoming unbankrupt after i paid my debts in the end of 2018. Currently, my CCRIS report is clear, but CTOS have full record of my bankruptcy information with remark of anulment under status for legal case. This will definitely hinder my loan application in the future. Will this CTOS record appear until a lifetime or it will be deleted in x years? Please help. Is it possible or impossible for an ex-bankruptcy to apply any loan with banks?

May I know what is the effect to a joint bank account is one of the account holders is bankrupt? Can the non-bankrupt holder get back his money from the joint bank account? How much he can get?

I started business last year and unsuccessful. Too many loan from friend, and money to pay back client. I still have a job now.

If I file bankruptcy , How if it affect with these:

1) joint name property with wife, loan amount higher than the market price

2) car that still have 5 years loan.

3) credit card

And how the debtor of these can come to me?

1) company client amount

2) friends loan

3) family loan

4) bank loan

5) 3rd party financial loan

Thanks.

Regards,

Eric Tang

Hi,

Thanks for the reply.

But my main concern is

If I file bankruptcy , How if it affect with these:

1) joint name property with wife, loan amount higher than the market pricE

Thanks.

I filed bankrupt by myself with PoD from bank representative and Bank Negara Credit Report after receiving warning letter from lawyer firm. During the day of PoD submission to court, the bank did not send any representative to file it. The court had approved my bankruptcy without bank representative attended and submit their PoD. Can the bank representative file the PoD with Jabatan Insolvensi a year later?

May i know pay off what debts? Debts reported during bankruptcy filed or after bankruptcy approved by Jabatan Insolvensi? How about creditors who refused to report to court while being called by the court but to jabatan insolvensi 1 year after ny bankrupty? All creditors were invited by court for your information.

My problem is the creditor invited to court for PoD filing was absent. After 1 year of my bankruptcy, i was informed that the creditor must file PoD for debt collection. May i know:-

1) should the creditor report the PoD to court or Jabatan Insolvensi? Creditor absent from court hearing that day, and creditor well awared of it.

2) will creditor allowed to file different amount from the PoD filed with court?

I have applied to purchase a standalone medical card and have been following up with insolvency office for more than 6 months. Each time they will tell me my request is under consideration. What happens if I just proceed with the purchase? Do I need to inform the insurance company my bankrupt status? If i purchase the medical card without approval from DGI, will this invalidate the policy or future claims etc. I have been trying to find out more info on this but there doesn’t seem to be specific written guidelines that I can refer to. Appreciate your advise. Thank you.

Im now in a huge problem because of PoD filing delay by bank representatives….they were all invited to court hearing but absent. Now, we are going to auction off the house to pay off the debts filed during court hearing. Then, to whom should those creditors file PoD? Court or Jabatan Insolvensi?

I filed bankrupt with PoD and Bank Negara Credit Report, the court had approved my bankruptcy according to the documents provided from bank representatives and Bank Negara Credit Report. During the court hearing day, bank representatives were absent and they were well awared of it. After a year of my bankruptcy, those bank representatives are trying to file the PoD to Jabatan Insolvensi skipping the court. Can you tell me is that legal? Can you tell me should the bank representatives refile their PoD to court instead of Jabatan Insolvensi? Or Jabatan Insolvensi has the right to file PoD without court? Thank you

Can bankruptcy work as insurance agent?

My mother passed away at age 55. She been declared bankruptcy. My question is what happen to her epf? Can the nominee withdraw the epf or its straight to DGI.

Hi,if bankruptcy person died, will his debts transfer to his families members?

If not, how his debts will being process?

The time and effort you expended better understanding on bankcuptcy. Kudos to your most commendable advice.

My husband has problem making credit card payments. I’m most concerned our joint-named properties will be auctioned off when he’s bankcrupt. I’m considering a divorce. Please advise:

1..Will the properties still be subject to auction even after his name has beem removed?

Please note all properties have been fully paid–every sen by myself, not a sen from him–right from the beginning!

Your king attention and prompt advice will be greatly appreciated!

Hi there,

My aunt wasn’t able to pay her debts since 2 years ago. Currently, she only has a car as her only asset and she plans to transfer the ownership of the car to her daughter.

Will any actions be taken after she declares bankruptcy?

Hi, How long is the process for high court to declare bankruptcy for someone when the debtor filed the petition? Can bankruptcy apply citizenship from other countries? Any difficulties if the person intend to apply for renunciation of Malaysia citizenship?

Can bankrupts apply for insurance?

So how much protection is it?

My father is 70 years old and has lost his job and recently diagnosed with dementia, so he won’t be able to find a new job due to his age and illness to pay off his debt. However, he is receiving government pension. If my father is declared bankrupt, will this affect his government pension? He has no other source of income besides the government pension. Thanks.

My Brother and Mother declare bankrupt in 10/2017. Still, they have asset property for the business shop; they did sell the shop in 2019 there is remaining money that more than enough that stuck with DGI and supposed to clear the remaining debts, but DGI processing is slow at the same time my brother also passed away in 9/2020, i am handling his current issue how to resolve this every time call they seem to keep on telling us we are calculating all the debts from DGI department. with covid-19 we are cannot travel to a different state, feel like more complicated.

Please advise how to resolve this problem.

http://www.mdi.gov.my/index.php/information-complaint

Hi..thanks for the knowledge sharing and spent your precious time answering all the questions here. I have a question on bankruptcy as well; Do a person who have been declared bankrupt needs to pay income tax? Because I think to settle the debts is more crucial than paying tax. Thanks.

HI

what happens to directors of a SDN BHD once Insolvency petition is filed?

1. Are they declared bankrupt?

2. What happens to foreign director?

3.foreign director is not served any notices to hand

4. Can the foreign director enter Malaysia and Leave Malaysia in future?

Maybank filed a “notice to freeze account – bankruptcy proceedings / adjudicated bankrupt.” This Maybank account belongs to a house.

1. Could his salary account in another bank be freeze as well?

2. He does own a car (no longer on installment). What will happen to his car?

Hi Sir,

I am on AKPK plan and went working overseas since 2015. However due to Covid I had been retrenched and unable to make further payments. I had also gave-up Malaysian citizenship in 2018. Can I still declare bankrupt by banks? Will I be declare bankrupt in the country I became citizen? Thanks

Hi Sir,

Currently, the banker filed bankruptcy proceeding against me. I plan to withdraw my EPF fund and transfer the EPF withdrawal to my son before i declare bankruptcy. Can DGI clawback the EPF withdrawal from my son when i declare bankruptcy. Thank you.

Hi Sir,

I have attended hearing end of Dec20 and judge gave me until 10Feb21 to negotiate and settle with the bank. Unfortunately I am not able to settle, does it mean I will be issued bankruptcy on 10Feb21 and bank account will be frozen immediately? My salary will be in on end of Feb21, what will happen to them? Will the salary be taken to pay to the bank who sued me? Can I still travel overseas after bankruptcy to visit my GF if she can gives a letter to proof that she will be paying for all the fees?

Hi, I have my medical insurance since ages ago (includes 36 critical illnesses) before I was declared bankrupt in 2017. Last week I had an operation to remove my cancer tumour and will submit my medical records to the insurance company for claims on 36 critical illness. My question is, will Insolvency take my insurance payout? This money is to be used for any further medical use and etc. Tq

I have 3 credit cards from 3 different banks. Credit card A, I could not pay since July 2020. It was RM3oK + but now with interest and late charges it has accumulate to RM38k+.

Credit card B, I have not paid since April 2020. At that time it was about RM17k+

Credit card C, Iam still paying when the bank said they want to confiscate my 2 current accounts with them if I dont pay..

My queries 1) Can bank A declare a bankrupt until the debt accumulate to RM50k.

2) Can all the 3 banks add together the debt to declare me a bankrupt.

3)Can the bank seize the money in my current accounts even before a bankrupt.

Please advise. Thank you

Hi my name is ray, due to unable to pay monthly installment of my house, the bank has aution off my house and i still owe them rm80k, i receive a letter for bancrupcy last month, my question is Bank A is suing me for bancrupcy, i still have money in Bank B, will the money in Bank B be frozen too? I mean i still have money in other bank, will it be affected too? thx in advance

HI, I wish to understand the procedure to declare a foreign guarantor a bankrupt under the Malaysia Insolvency Law. The foreign guarantor is a debtor in Malaysia. Do we need to pursue legal proceedings in the guarantor’s country of origin as well? Thank you.

Thank you for your reply,

Hi, if a person is declared bankrupt, will his wife, parents and siblings’ assets also be subjected to bankruptcy proceedings?

Hi, if i owe Rm300k and declare bankruptcy, do i need to pay all rm300k someday only i can be cleared from bankruptcy? Thanks

Good day to you. I jointly own a home (that is still under a joint bank loan financing) with my spouse. In the event that only one of us is declared bankrupt, can the DGI or the bank seize and realise the property via auction/ sale – even if the non-bankrupt person is able to service the joint bank loan alone? Is a jointly-owned home like this considered an asset that must be surrendered to the DGI?

Hi, If a person have joint name in a property but he will transfer his ownership name to other owner before he declare bankrupt. Will it impact to the other property owner?

Hi, I had been declared bankruptcy few years ago. I am still paying the mdi monthly. My father wants to make a will to leave his assets to my children. My question is can I be the guardian of my children stated in the will? Will my bankruptcy have any influence on it?

Hi, my father has declared bankruptcy about 6 years ago, and he has passed away. May i know will his bankruptcy status will discharge automatically? He actually didn’t own any property or any cash in the bank. Appreciate your advice.

Please advise what’s the impact on joint FD account if one of them is declared bankrupt.

Thanks.

Hi. Can someone who has been declared bankrupt involved in local or overseas investment?

If she had gained income from the overseas investment (example: stock market) later, any possibility that the bank (the creditor) or MDI detect and freeze the money?

If the bankrupt has money from another country, can he appoint a proxy (third party) to be the receiver of this money in Malaysia?

I’m a guarantor for a few of my family business loans, even though I’m not involved in the business at all and signed on because a stubbornly trusted my family member when I was young. It seems likely that the business will be heading to bankruptcy with quite a large debt about 1million+. Is there a way for me to appeal out of this?

Hi, my mom has declare bankruptcy since 25years ago, i recently bought a property and already paid in full. Can i transfer this property to my mother’s name?

Hi Sir, i am a bankruptcy since 2013 issued by a bank due to housing loan payment. Since then i was paying promptly the monthly contribution to MDI without fail. Now i would like to make settlement, so i have approach the relevant bank for a discounted settlement before i could submit to MDI. Now the bank management requesting my EPF statement. Kindly advise should i forward them that information or not. Thanks

Hi, if the person bankrupt and passed away so creditors will look for next of kin?

Hi, I have settled my debts and my status is now Not Bankrupt a few days ago … Is that means I can still apply for other loans – car loan/ housing loan/ credit card? Will the bankers know that I was bankrupt before? and will it affect my next loan application?

Hi, I was declared bankrupt in 2015 due to CC debts. I owed 3 banks and one of the banks (bank A) sue me for bankruptcy. If I want to pay off my debt, i need only to pay bank A alone or I also need to pay the other 2 banks. if I do not need to pay the other 2, according to the Limitation Act 1953 can these 2 banks still sue me for bankruptcy Thanks for answering.